Numbers are used for just about everything in the financial world. Companies report their results using numbers, investors trade in terms of numbers, and most everything is evaluated by numbers. On the face of financial reports, most of these numbers are representative of some type of currency such as the US dollar, which are then evaluated based on more numbers in the form of ratios.

Numbers may be used for more than just determining the strength of a company’s financial statements, though. They can also be used for evaluating the quality of financial statements. One method is the application of Benford’s Law, which states that many kinds of number sets should follow a logarithmic distribution known as Benford’s distribution.

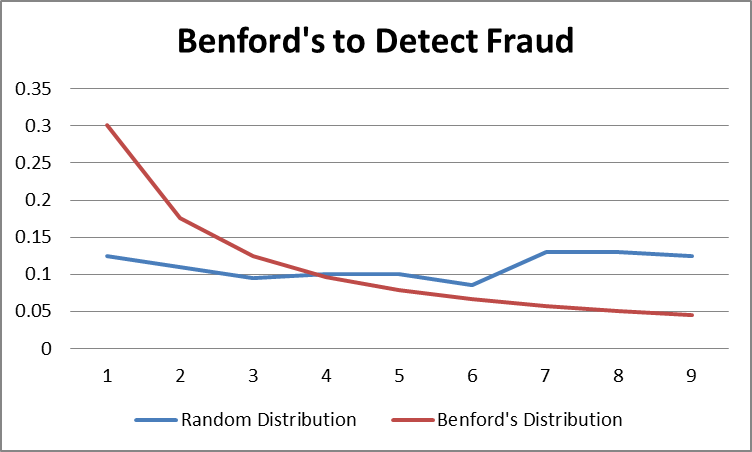

Frank Benford, a physicist at General Electric back in the 1930s, first hypothesized the distribution that now carries his name after noticing that the first pages of the logarithm books were significantly more worn than the later pages. (This was before the time of electronic calculators, of course.) Inspired, he investigated over 20,000 numbers culled from various sources, and defined the distribution in a research paper published in 1938. In the paper, he found that about 30% of the numbers investigated began with the digit 1, 18% began with 2, and so on, with about 5% beginning with 9.

Many explanations for this phenomenon have been proposed. One, based on an intuition, is as follows. Consider the absolute difference between two numbers. Most people can easily understand that the incremental rise from 1 to 2 or from 8 to 9 is the same, namely 1. On the face of it, these seem like equal increase. If, however, we think in terms of percentage growth – like investors do – we see that the “distance” between 1 and 2 (100%) is much larger than that between 8 and 9 (12.5%). This is a characteristic of logarithmic scales.

A lot of research suggests that Benford’s Law can be used to detect anomalies in data, whether from clerical errors, random chance, or outright manipulation. When a set of numbers expected to conform to the distribution do not do so, this can be a sign that there is something wrong with the data.

Benford’s Law has been used to detect fraud in accounting for some time, thanks in large part to the work of Professor Mark Nigrini. The distribution is most often used on an individual account basis, such as accounts payable, to detect the over or under use of certain digits. But recent research has led to an increased use of the law in analyzing financial statements themselves.

While the process of using Benford’s Law to detect fraud on an account basis has been around for some time, a recent paper entitled Financial Statement Irregularities: Evidence from the Distributional Properties of Financial Statement Numbers by Dan Amiram, Zahn Bozanic and Ethan Rouen explores the use of Benford’s distribution on the face of financial statements. In an overview, the authors found that 1) financial statements, as a whole, conform to the distribution and 2) individual divergences from the distribution “may reflect the informational quality of financial disclosures.” This means that the numbers on the face of financial statements should conform to Benford’s distribution and those financial statements that do not may be of poor quality.

The authors used two metrics in measuring a financial statements’ adherence to Benford’s distribution. The first is the Kolmogorov-Smirnoff (KS) statistic, which compares the largest single deviation to a critical value. This allows for a definitive pass or fail answer. The second is the Mean Absolute Deviation (MAD) statistic, which finds the average deviation of the actual distribution to the ideal Benford distribution.

Source: http://www.AuditAnalytics.com

The authors showed that deviations from the Benford distribution are correlated with restatements and Accounting and Auditing Enforcement Releases (AAER). In the remainder of this post, we investigate whether deviation from Benford’s distribution may be predictive of other issues such as adverse 302 and 404 opinions, and non-timely financial reports.

By using XBRL data from 2010-2012 we apply a crude version (meaning we do not control for variables) of the KS statistic on a population of 18,086 financial statements. Roughly 7% of these financial statements failed the KS statistic at a 20% confidence interval. The results are as follows:

Source: http://www.AuditAnalytics.com

Companies that failed the KS statistic were 30% more likely to have an adverse 302 opinion, 45% more likely to have an adverse 404 opinion and 50% more likely to file a non-timely filing in the following two years. This means companies with financial statements that do not conform to Benford’s distribution have a greater chance of having poor internal and disclosure controls. And having poor internal and disclosure controls can lead to low quality financials either due to intentional or unintentional means. This type of environment will often lead to unfavorable outcomes such as non-timely filings and restatements.

While Benford’s Law should not be used as a decision making tool by itself, it may prove to be a useful screening tool to indicate that a set of financial statements deserves a deeper analysis.