Similar to the trends we’ve seen among SEC registrants, the number of SEDAR issuers has been declining over the years. In 2019, only 2,350 Canadian issuers reported audit fees – a substantial 34.5% decrease from the 2,963 issuers in 2018.

This decline in issuers is primarily due to the COVID-19 pandemic, which has contributed to mass disruption to periodic filings on a global scale. Many issuers in Canada opted to take advantage of blanket relief extensions on periodic filings offered by securities regulatory authorities.

Blanket relief orders were established for issuers in Canada, allowing for a 45-day extension for filings due before June 1, 2020. This was later expanded to cover filings through September 30, 2020. Therefore, it is likely the total number of issuers for 2019 will increase as late filers issue their annual reports.

For Canadian companies, the compensation of the external auditor is disclosed pursuant to the Multilateral Instrument 52-110 on Audit Committees, which describes in Item 9 the following categories of fees that are to be disclosed:

- Audit Fees;

- Audit Related Fees;

- Tax Fees, and

- All Other Fees.

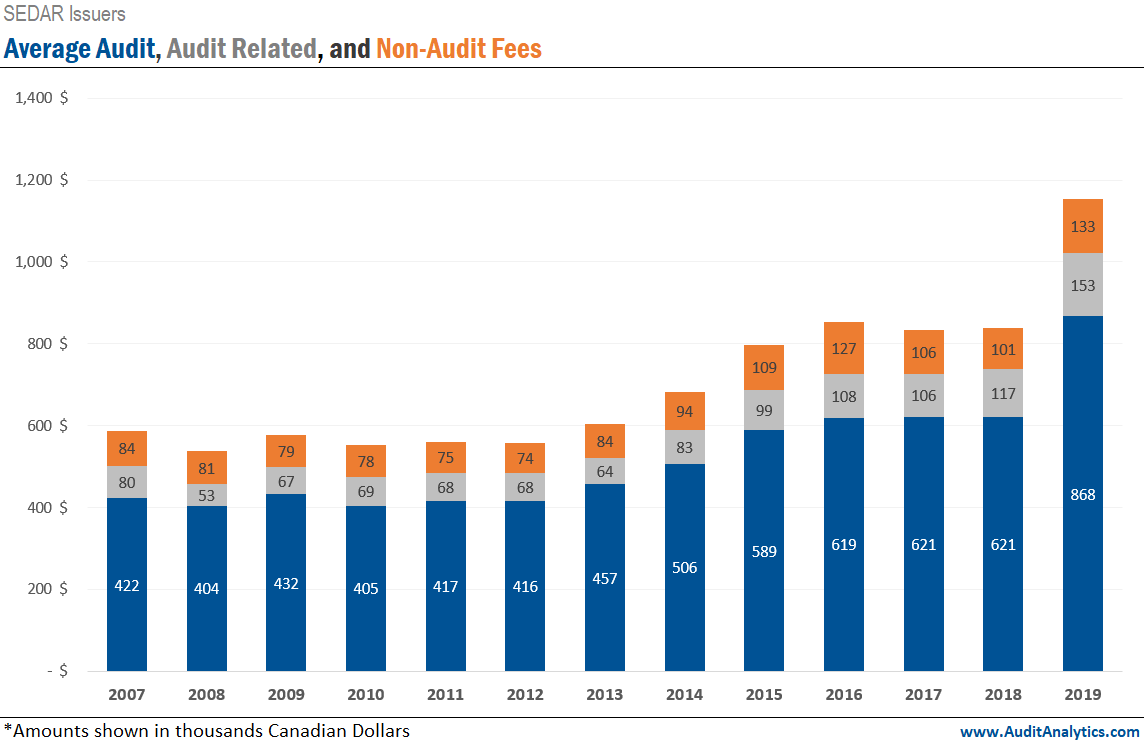

Since 2007, the average amount of audit fees per Canadian company has continued to increase each year, with the largest increase coming in 2019, when all fee categories saw significant increases in totals.

Audit fees increased from an average of $621,000 in 2018 to $868,000 in 2019, a 28.5% increase. Audit related fees jumped 23.5%, rising from an average of $117,000 in 2018 to $153,000 in 2019. Similarly, non-audit fees increased 24.1% from an average of $101,000 to $133,000 in 2018 and 2019, respectively.

A review of non-audit fees as compared to audit fees is of interest, as high non-audit fees could indicate an auditor independence concern. At times, analysts prefer to view audit fees as its own category, while others prefer to see audit fees and audit related fees collectively. For these reasons, this analysis provides both approaches.

The graph below displays audit fees (including audit related) and non-audit fees as a percentage of total fees. Audit and audit related fees have remained relatively consistent over the years, comprising 88.5% of total fees in 2019.

Audit fees (excluding audit related) comprised 75.3% of total fees in 2019, an increase from 74.3% in 2018. The proportion of non-audit fees (including audit related) have remained relatively stable since the high of 28% in 2007, dropping to 24.7% in 2019.

The chart below provides the breakdown of audit, audit related, and non-audit fees as a percentage of total fees.

As shown, audit fees have increased since 2018 and both audit related and non-audit fees have decreased in 2019. Non-audit fees have declined to 11.5% of total fees – a new low in the 13 years of data.

Note: All amounts stated are in Canadian Dollars.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.