We continue our review of financial reporting quality this week by looking at trends in financial restatements in Canada. The number of financial restatements in Canada has been relatively consistent over the past five years. There were 144 restatements in 2020, just one more than in 2019. This is down 60% from the high of 347 in 2007.

The 144 restatements in 2020 represented just 3.8% of companies that issued an annual report in Canada during 2020. This is down from 8% in 2007. In contrast, the US saw 4.9% of companies issue a restatement during 2020.

The number of issues cited in each restatement was near its highest in 2020. Restatements cited nearly 1.9 issues on average. Slightly behind the high of 1.95 in 2015 and significantly higher than the 1.4 to 1.55 over the past four years.

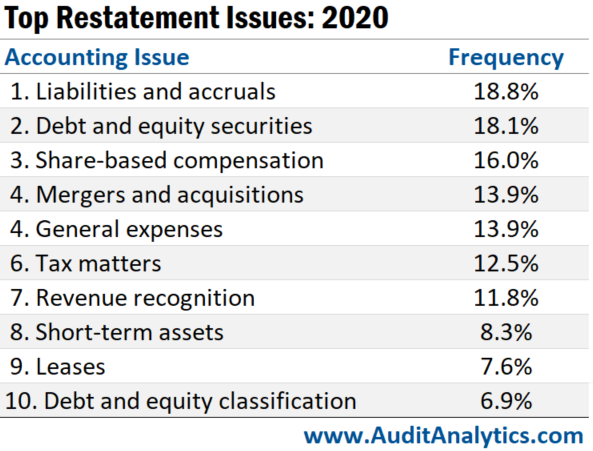

The most common issue cited was liabilities and accruals. Liabilities and accruals were cited in nearly 20% of restatements. While liabilities and accruals are usually a common issue, this was the first time they were cited as the top issue. They were the fifth most common issue.

There was some overlap between issues cited in Canada and the US. Liabilities and accruals were the third most cited topic in the US. Debt and equity securities were second in both the US and Canada. And general expenses were the fifth most common in the US and tied for fourth in Canada.

One surprise was that revenue recognition was outside of the top five in Canada. Revenue recognition has been the most common issue in the US for the past three years. Tax matters were also among the top five in the US but missed out on the top five in Canada. Tax matters were fourth in the US and sixth in Canada.

Another notable issue that was outside the top five was leases. Leases were rarely cited as a reason for restating prior to 2019. The adoption of the new lease standard (IFRS 16) in 2019 caused a significant rise in the citation of leases for accounting restatements. No restatements cited leases between 2016 and 2018. Roughly 5% and 7.5% of restatements cited leases in 2019 and 2020, respectively.

Financial reporting has generally improved in Canada based on the declining frequency of financial restatements over the past decade and a half. This progress has stagnated in recent years, though. We expect the number of restatements in 2021 to be in line with previous years based on recent trends and the fact that the multiple rounds of SPAC restatements did not impact Canada as they did the US.

Interested in our content? Be sure to subscribe to receive our email notifications.