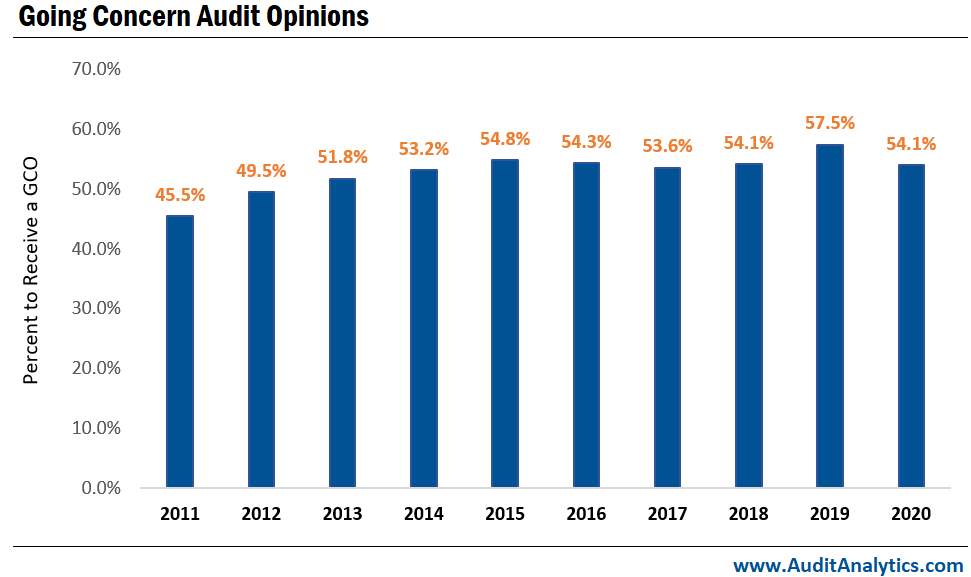

More than half of Canadian companies received a going concern opinion (GCO) in 2020.

Canada’s CAS 570, which requires the auditor to assess and report on management’s use of the going concern assumption, became effective for periods ending on or after December 14, 2010.

The percent of companies that received a GCO has topped 50% annually since fiscal year (FY) 2013. Excluding the COVID-related 3.5% jump in FY2019, the percent of GCOs has been steady since FY2014.

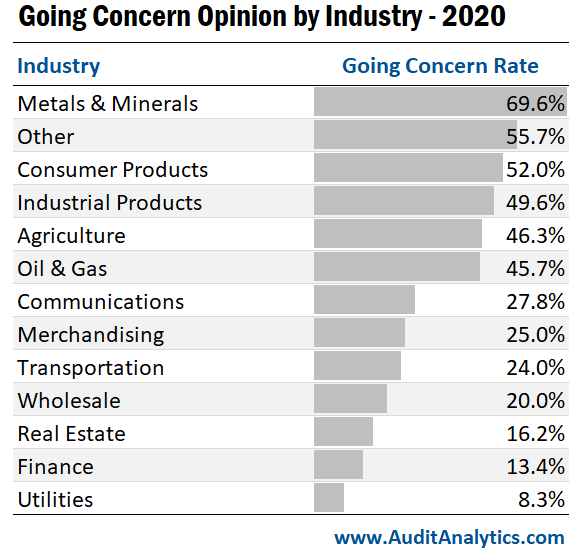

The largest industries in Canada account for the high rate of GCOs. Metals & Minerals companies made up one-third of all Canadian companies during FY2020. And over 80% had no revenue in FY2020.

Companies that identified in the Other industry made up nearly 30% of all Canadian companies during FY2020. Over half had no revenue during FY2020.

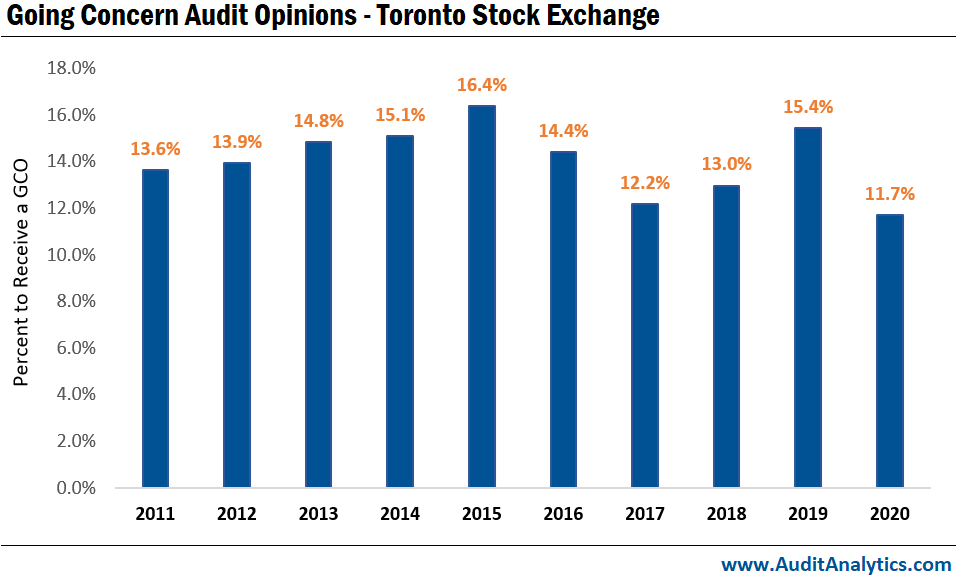

Whether a company was listed on the Toronto Stock Exchange (TSX), the TSX Venture Exchange (TSXV), some other exchange, or not listed at all also had a big impact on GCO rates.

For example, the TSX lists many of the largest companies in Canada. Consequently, only 12% of companies listed on the TSX received a GCO during FY2020.

Meanwhile, two-thirds of companies listed on the TSXV received a GCO. The TSXV lists many of Canada’s emerging companies – including many pre-revenue Metals & Minerals companies.

When we focus on the TSX, we see a slightly different trend. The percentage of GCOs received by TSX companies fell to a new low during FY2020. And a general decline in GCOs can be seen since FY2015.

The data used in this analysis comes from the Audit Analytics Canada Audit Opinions database. The Canada Audit Opinions database tracks all auditor reports on financial statement on Canadian public companies disclosed since 2005.

For more information about Canada Audit Opinions, contact us at info@auditanalytics.com.

Interested in our content? Be sure to subscribe to receive our email notifications.