The COVID-19 pandemic has had wide-ranging impacts on public company disclosures over the last year. In particular, the pervasive and ongoing uncertainty affecting the global economy contributes to increased subjectivity underlying assumptions and increased challenges in determining estimates for certain metrics in financial statements. If those metrics are related to material accounts, and involved particularly challenging, subjective, or complex auditor judgment, it could result in the matter being identified as a critical audit matter (CAM) during an audit.

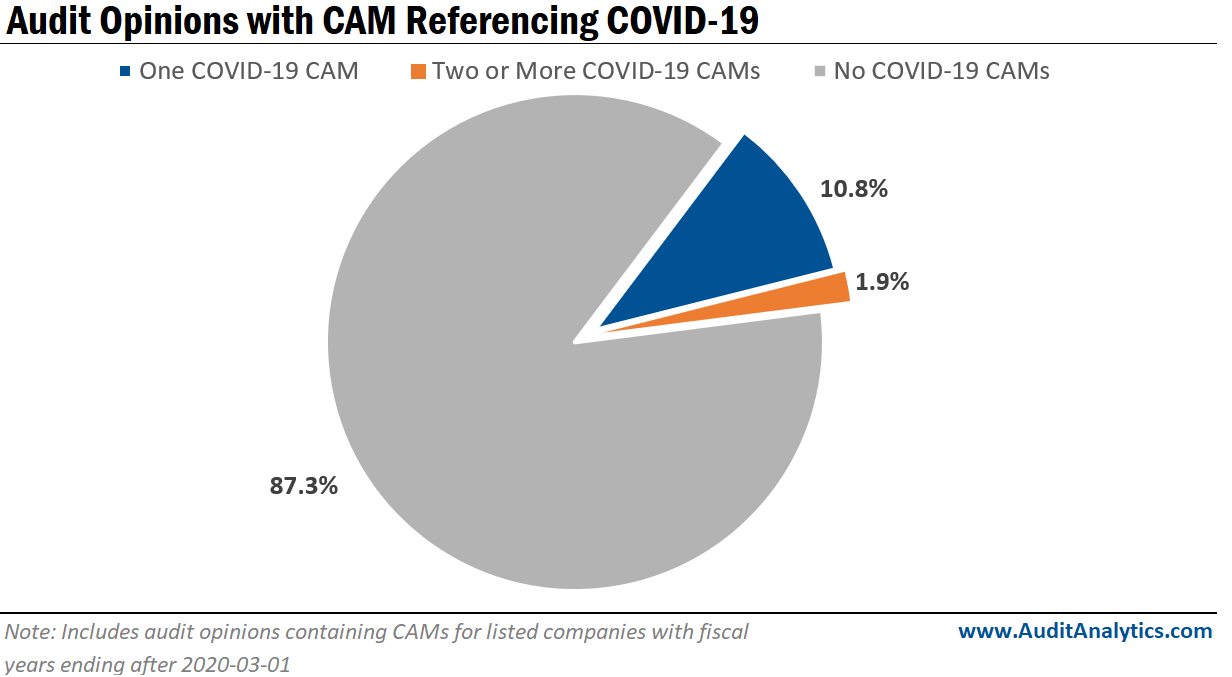

Of roughly 2,700 audit opinions containing CAMs for listed companies with fiscal years ending after March 1, 2020, 12.7% include at least one CAM referencing the COVID-19 pandemic.

For opinions with two or more CAMs referencing the pandemic, more than half were for companies in the Consumer Cyclical industry.

While no industry was immune to the events of the last year, certain industries, due to the nature of their operations, were more likely to have a CAM communicated that referenced the pandemic.

Over half of all CAMs referencing COVID-19 (58%) are for companies in the Financial Services, Industrial, and Consumer Cyclical industries.

For those industries, the pandemic had direct, adverse impacts on revenue, operations, and cash flows. Consequently, financial statements for those industries have added complexity and subsequently necessitate more subjectivity and estimation.

The general economic downturn during the pandemic contributed to adverse impacts on the financial condition and operations for many Financial Services companies. Additionally, Financial Services companies were adopting ASC 326 over the last year, requiring more estimation of credit losses, compounding the complexity of the audit and resulting in additional COVID-19 related CAMs for the industry.

The overall increased volatility significantly impacted companies in the Industrial sector, which depend closely on conditions in the markets they serve and general forecasted economic conditions. Whereas the Consumer Cyclical industry, including hospitality, travel, and entertainment companies, experienced direct financial impacts by pandemic guidelines that shuttered operations and restricted travel.

The sectors with the fewest observed COVID-19 related CAMs – Utilities, Basic Materials, Consumer Defensive, and Healthcare – are the industries most likely to be insulated from significant adverse impacts from the pandemic due to the ubiquitous nature of their operations.

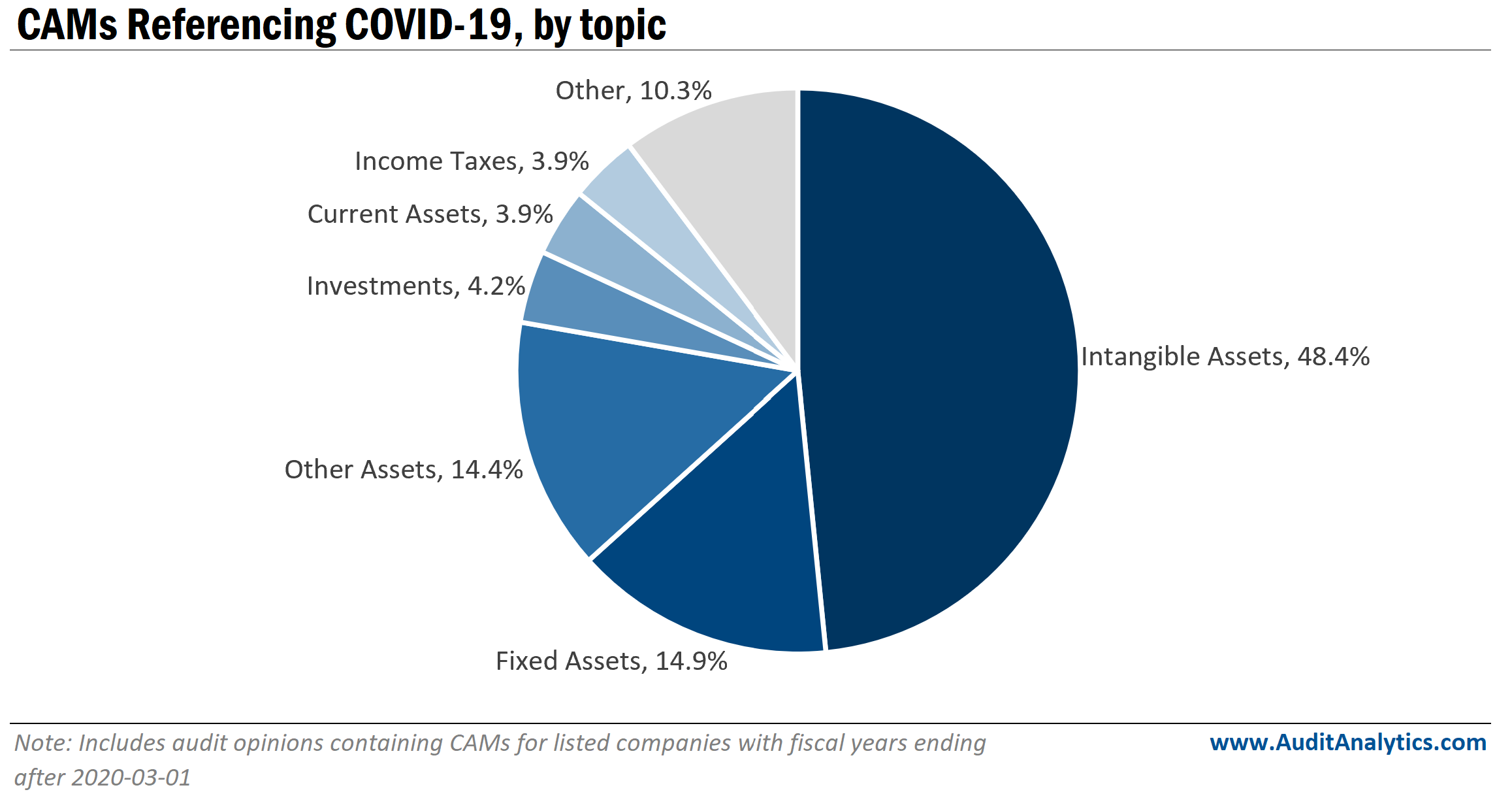

While trends in COVID-19 related CAMs observed across sectors are closely tied to operational differences, trends in audit matter topics referencing the pandemic are closely tied with the similarities in accounting procedures.

Nearly half of all CAMs referencing the pandemic (48.4%) related to intangible assets, including goodwill. It is unsurprising that intangible assets is the most common CAM topic referencing the pandemic; before the pandemic, intangible assets appeared as an audit matter in roughly one-quarter of US audit reports.

Considering assessing and evaluating intangibles and goodwill always necessitates a degree of estimation and subjectivity, intangible assets will frequently be a common audit matter topic, if material to a company’s financial statements. The severe and persistent negative effects that COVID-19 injected into global economies, and the impact of added uncertainty on long-term assumptions for cash flows and operations, only exacerbates pre-existing challenges with assessing goodwill and intangibles for both management and auditors.

While the impact of the pandemic on certain areas of company financials is evident, the impact of the pandemic on audit procedures utilized when addressing a CAM during an audit is less pronounced.

For example, the majority of CAMs addressing intangibles with a reference to COVID-19 in the Industrial and Consumer Cyclical sectors reference the pandemic in the CAM description, the portion of the disclosure that explains why the matter rose to the level of a CAM. Less than one-third of those CAMs explicitly reference the pandemic’s impact on audit procedures in the auditor response portion of the CAM. This suggests that the threshold for an intangible asset audit matter to be considered critical may have been lowered by pandemic-related conditions, but procedures used to evaluate intangibles on the balance sheet during an audit were generally unaffected.

Conversely, some procedures typically employed to evaluate other audit matter topics, such as inventory and fixed assets, experienced disruption by COVID-19 restrictions and operational impacts. As an example, the pandemic triggered a change in how Target [NYSE: TGT] accounted for inventory, subsequently having a direct impact on the procedures used to evaluate inventory during the audit.

Since the adoption of the CAMs requirement, Target received two inventory-related CAMs, one in last year’s annual report, before the pandemic, and one in this year’s annual report. The audit procedures to assess Target’s inventory outlined by EY in both auditor response sections were similar, but 2020 required additional steps to reflect the temporary suspension of Target’s physical inventory counts during the pandemic.

The additional steps taken during the audit included evaluating the effectiveness of controls over the modified store inventory count process, as well as “testing the existence of inventories by observing physical inventory counts for a sample of stores and distributions centers.” Evaluating Target’s inventory was already a complex audit process and the added complexity resulting from the pandemic prompted procedural changes in order to address the audit matter.

Certain trends in audit matters during the pandemic are expected, such as the industries most impacted and the most frequent topics, but taking note of COVID-19 references in CAMs is useful to gain insight and gauge areas of auditing difficulty during a period of uncertainty and disruption.

This analysis uses data from the Critical Audit Matters database, powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.