Thousands of NT (“non-timely”) filings are disclosed every year, but only a small percentage seems to trigger a significant market reaction. A non-timely filing is a notice that a company needs additional time to file periodic financial statements. (See here and here for more information about NT filings.) Reasons for a delay range from requiring a few additional days to complete an audit, to dealing with an unexpected material government investigation.

In our recent post about Hertz (NYSE: HTZ), we provided an analysis of red flags that could have provided investors with advanced warning of impending accounting problems. Among those red flags, we identified a non-timely filing that indicated potential accounting issues as one of the most powerful warning signals. This flag was largely overlooked by the market, and only a subsequent 8-K Item 4.02 filing (Non-Reliance disclosure) triggered a massive sell-off. In that post, we also noted that in most cases, by the time news of a restatement hits the market, it is already too late for most investors.

In this post we will try to identify more scenarios where a non-timely filing could have provided an early indication of upcoming troubles.

Our objective was to identify filings that contained new significant information (such as accounting issues or a pending investigation) that was not known to the market and at the time of the filing was not yet incorporated into the stock price. To limit the analysis to such cases, we used a somewhat crude but effective method: namely, the proximity of the NT filing to the highest closing in the preceding 52 weeks. If an NT filing was close to a 52-week high (both time- and percentage-wise), then the subsequent troubles were unlikely to have already been priced-in.

For the purpose of this analysis we considered only companies traded on NYSE or NASDAQ, and that had a 52-week high over $5. We wanted to limit ourselves to the companies that are easy to borrow and may be of interest to institutional investors. For the same reason, we excluded thinly-traded stocks with average daily volume below 100,000 shares.

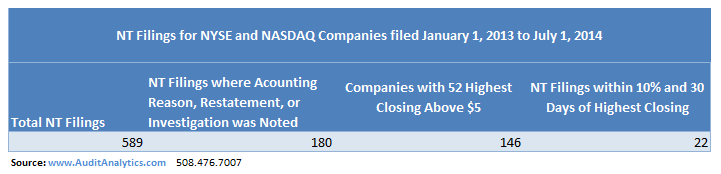

Looking at Table 1 above, NYSE and NASDAQ companies filed 589 NT forms over the last 18 months. Only 180, or about 30%, identified an accounting issue or an investigation as a reason for the company’s inability to file timely financial statements. Out of those 180, only 22 cases (5% of the total) were filed within 30 days of the company’s stock reaching a 52-week high. This is consistent with our previous statement: by the time negative news hits the market, the stock is normally well on its way south.

For illustrative purposes, let’s take a look at a specific company, IXIA (NASDAQ: XXIA).

Over the last two years, IXIA has given investors plenty of reasons to worry. Restatements, a CEO dismissal (following a “misstatement” of his academic credentials and employment history), deficient internal controls, and a CFO resignation are just a few of the red flags that were tracked by Audit Analytics. Since our present analysis focuses on NT filings, let’s take a look at two NTs: the first filed on March 19, 2013, and the second on March 4, 2014.

Both filings were early indicators of subsequent revenue recognition restatements. After market close on March 19, 2013 (indicated by a white arrow on the chart), IXIA filed an NT that disclosed issues with the company’s revenue recognition policy. Then, on April 4, 2013, the company announced that previously-filed financial statements could no longer be relied upon. In this case, the March 2013 NT was indeed near a 52-week high, and was a very good early indicator. As with Hertz, this filing was largely overlooked by the market. The subsequent sell off (further fueled by the additional negative events mentioned above) saw the company lose nearly 50% of its market cap in just 12 months. Wise were those who cut their losses early, or managed to profit from short positions.

The pattern here repeated again the following year. IXIA filed an NT 10-K on March 4, 2014, noting that the company was unable to file timely financial statements due to a number of worrying problems. “The Former CEO had misstated his academic credentials, age, and early employment history… The investigation found… an aggressive tone at the top set by the Former CEO and a lack of leadership at the top with respect to the recently resigned Chief Financial Officer…” The NT went on to indicate that accounting adjustments were expected related to the company’s revenue recognition. As in 2013, the NT did not trigger an immediate sell-off. The stock recovered some of the lost ground (on what looks like a short covering), before sliding back to the support line. A couple weeks later, IXIA had another revenue recognition restatement that affected the first two quarters of 2013 and decreased net income by a cumulative $1,031,000. The stock price continued its downward slide, but on lower volume than in 2013 and at a somewhat slower pace. Not that at the time of the second restatement, the stock was already almost 50% off its 52-week high.

IXIA is not the only case where an NT could have been used as an early indicator of a subsequent significant decline in stock price. As indicated in Table 1 at the top, we identified 22 other companies that made non-timely filings near 52-week highs. Referring back to our analysis parameters laid out at the beginning of this article, three companies were excluded from the start due to low average daily volume. Of the remaining, eight were eliminated due to the presence of an earlier announcement of trouble, and five were eliminated due to an accurate explanation of the magnitude of the trouble. We are looking for the first notification of material negative events. In our experience, an inability to estimate the magnitude of the error or liability increases the chances that the event is indeed significant. Using this filter, we eliminated additional five companies. We have also excluded one company because the adjustment to financial statements was expected to increase net income.

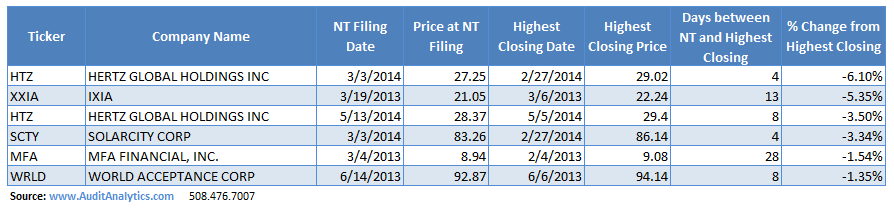

We were left with six cases (five companies – Hertz (NYSE:HTZ) shows up twice) where the NT was the first notification of trouble, no estimated magnitude was provided, and the stock price was near a 52-week high. As mentioned, we set these parameters to identify only those NTs that had a very high probability of being an early indicator of a subsequent significant price drop.

The cases listed above are the instances we identified for which an NT filing could have been used as an early screening filter. Three out of five companies – Hertz, Ixia, and Solarcity (NASDAQ:SCTY) – had a subsequent restatement. World Acceptance (NASDAQ:WRLD) identified a material weakness in its internal controls, but didn’t have to restate financial statements. MFA Financial (NYSE:MFA) was the only company that did not identify any subsequent accounting and control issues and was also the only company that did not experience a very significant correction after filing an NT form.

We continue to believe that NT filings are an under-appreciated red flag, perhaps because the different kinds of NTs are unfamiliar to most investors.

Note: It should be mentioned that NT filings are seasonal – for quarterly reports, the due date of the financial statements is 40 days after the end of the fiscal quarter. Companies with June 30 quarter end should file financial statements by August 10th. Audit Analytics monitors NT filings for all SEC registrants and can identify filings that meet the criteria listed above.

Disclaimer: Audit Analytics is not an investment adviser and is neither giving nor attempting to give any investment or trading advice.