Each year, Audit Analytics looks at the big picture of comment letter activity to see what important issues the SEC is focusing on, and how they compare to prior years. In the first half of 2016, 2,491 comment letters 1 (1,452 UPLOADs and 1,039 CORRESPs) were filed by 808 registrants, a notable decline in comparison to the 3,166 and 4,348 in the first six months of 2015 and 2014, respectively.

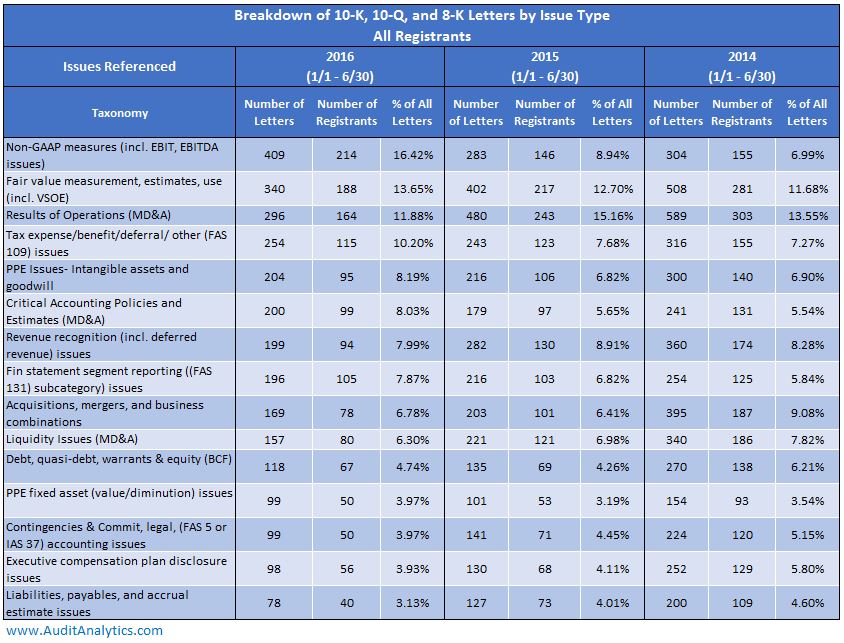

The table below focuses on just a few of the major issues discussed in comment letters over the past 3 years.

Although the overall trend of comment letters hasn’t changed, non-GAAP measures are the new top area of concern. In the first 6 months of 2016, 16.4% of all letters and about one quarter (25.7%) of the conversations included at least one non-GAAP comment, in comparison to 8.9% in the first 6 months of 2015. This number should come as no surprise: several recent SEC speeches provided a clear indication that the SEC is paying close attention to the excessive or misleading use of the custom metrics. In at least 14 cases, the companies were required to make substantial changes to their non-GAAP presentation.

Back in July, Audit Analytics, together with Accounting Observer, released a blog that discussed the types of measurements that companies were required to modify following SEC comments.

Another interesting trend that emerged in 2016 is the large number of conversations that involved SEC review of earnings transcripts, presentation materials, or corporate websites. In the past, SEC reviews mostly focused on SEC filings. For example, in the first 6 months of 2016, 47 distinct companies received comments related to their earnings calls.

Management’s Discussion and Analysis of Financial Condition and Results of Operations, page 42

1. Please tell us what consideration you gave to including disclosure and quantification, to the extent possible, of currently known trends, events, and uncertainties specifically related to your business that are reasonably expected to have a material impact on your liquidity, capital resources, and/or results of operations. Your discussion of trends and uncertainties should provide insight into the extent to which reported financial information is indicative of future results. In this regard, we note your earnings calls indicate that you have recently begun to enter into more long-term contracts with larger customers. As an example, you discuss in your earnings call that greater than two-thirds of net new Office bookings were potential customers opting for annual or multi-year agreements. However, your disclosure only states that there has been growth in your business with larger customers and does not discuss your growth in longer term contracts. Refer to Item 303(a)(3)(ii) of Regulation S-K and Sections III.A and III.B.3 of SEC Release 33-8350.

Additionally, a relatively large number of letters in 2016 focused on 8-K filings.

Although the increase in non-GAAP comments provides a clear indication of the SEC’s focus, non-GAAP issues were not the only popular topic under review.

Questions related to fair value measurement were also at the top of the list, totaling 14% of all letters. Similar to last year, many of the fair value comment letters released in 2016 questioned valuation techniques, specifically Level 2 and 3 securities, which included requests to disclose valuation techniques and inputs, as well as discussion of the acceptable valuation methods.

Note 7. Assets and Liabilities with Recurring Fair Value Measurements, page 128

9. We note your disclosure of the valuation techniques and significant unobservable inputs used in your Level 3 fair value measurements on page 131. Please tell us where you have disclosed the valuation techniques and inputs used to develop your Level 2 fair value measurements. Refer to ASC 820-10-50-1a and 50-2bbb. If your narrative disclosure on page 129 is intended to satisfy this requirement, please note that obtaining prices from market sources such as the Intercontinental Exchange and Bloomberg is not a valuation technique or input.

Other comment letters focused on the valuation of long-lived assets and goodwill, including the impact of lower commodity prices on liquidity. Given the nature of these letters, not all comments were easy to resolve, with many resulting in further push-back from the SEC.

Impairment of Long-Lived Assets, page 84

3. We have read your response to comment 7. We reissue the portion of the previous comment related to your consideration of defining a “prolonged period” of lower commodity prices in your critical accounting policy on impairment of long-lived assets. Lower commodity prices appear to be a critical assumption and you have asserted to us in your response to comment 9 that certain asset groups within your Natural Gas Services segment showed trending (higher) years to recovery over the last few reporting periods and the trend was primarily due to decreased commodity prices resulting in lower-than-expected EBITDA for these asset groups. Please advise us.”

As in previous years, tax-related topics received their fair share of interest, with many of the comments targeting indefinitely reinvested foreign earnings and the implications of repatriation of the cash held overseas.

As mentioned in a previous blog, in 2015, Costco (COST) repatriated a substantial portion of its indefinitely reinvested earnings and changed its position regarding additional portions of its cash held overseas. A recent SEC comment letter questioned whether the remaining overseas cash is still indefinitely reinvested and whether a tax liability ought to be recorded.

Note 8 – Income Taxes, page 59

3. We note you changed your position in the fourth quarters of 2014 and 2015 regarding the undistributed earnings of your Canadian operations such that a portion of the earnings were no longer considered permanently reinvested. Please tell us in significantly more detail the facts and circumstances which led to the changes in your position and the underlying reasons for repatriating these earnings. Further, tell us in detail how you evaluated the criteria for the exception to recognition of a deferred tax liability in accordance with ASC 740-30-25-17 and 18 for the remaining Canadian undistributed earnings that are intended to be indefinitely reinvested. In this regard, describe the type of evidence that sufficiently demonstrates that remittance of the remaining Canadian earnings will be postponed indefinitely. As part of your response, please quantify the amount of cumulative undistributed earnings from your Canadian operations for which you have not provided for U.S. deferred taxes and quantify the amount of cash and cash equivalents and short-term investments held by your Canadian operations.

Other tax-related letters focused on the release of the valuation allowance and request to justify assumptions that the results will improve and permit to utilize the allowance.

Income Taxes, page 74

We note the evidence you considered for the release of the majority of your valuation allowance against your U.S. federal and state deferred tax assets in the fourth quarter of 2015. Based on your historical operating results, it appears that the realization of your deferred tax assets is dependent on material improvement over present levels of pre-tax income, including the impact of acquired entities. Given the significant portion of U.S. operating loss carryforwards expiring between 2023 and 2027, tell us in detail the material assumptions underlying your determination of the expected U.S. pre-tax income amount needed to realize your deferred tax assets. Tell us how you weighted all of the positive and negative evidence, including to the extent to which it can be objectively verified, in reaching your conclusion to reverse the valuation allowance. Please refer to ASC 740-10-30-21 through 30-23.

And of course, revenue recognition comments are still a top area of concern, with many of the comments focusing on milestone payments. 13% of registrants having comment letters in this topic belong to the pharmaceutical industry (SIC: 2834) alone.

2. Please provide us the amount of each milestone and a description of its triggering event included in the $525 million milestone payments that you will be eligible to receive for each Amgen program. Also provide us your accounting policy for recognizing revenue related to these milestones. Refer to ASC 605-28-50.

Response:

Under the Research Collaboration and License Agreement between the Company and Amgen, Inc. (“Amgen”), dated December 31, 2014 (the “Amgen Agreement”), Amgen is required to pay the Company, among other things, future potential payments upon reaching certain development, regulatory and commercial milestones. To date, the Company has not received any milestone payments from Amgen. These milestones are highly speculative and contingent in nature and disclosing the details of all such milestones in the Company’s periodic reports or otherwise may lead investors to mistakenly place an unrealistic value on the payment stream from future milestone payments. Moreover, the Company would like to draw to the Staff’s attention that because of the highly confidential nature of the specific milestones and related amounts under the Amgen Agreement, and the likelihood of considerable competitive harm to the Company should such terms be specifically disclosed, the Company requested confidential treatment of these terms, and the Commission granted that request pursuant to an Order Granting Confidential Treatment under the Securities Exchange Act of 1934 issued on July 21, 2015. An unredacted version of the Amgen Agreement including the details of the milestones was previously provided to the Staff on March 26, 2015 in connection with such request for confidential treatment. The Company will further disclose whether any payments subject to milestones have been recognized, or not, in its future periodic filings.

Stay tuned for our follow-up comment letters blog.

For more information about comment letters, please contact us at info@auditanalytics.com.

1. [Comment letters reviewed through 10-K, 10-Q, and 8-K. One important thing to remember is that comment letters are normally released only 20 days after the resolution of all the comments, so the numbers of letters and number of registrants may change for the mentioned periods. Based on historical experience, for about 10% of the comments dissemination days is more than 90 days after the filing date of the letter]↩