The SEC recently announced settled charges with Under Armour [NYSE: UAA] related to certain disclosure failures and making misleading statements to investors. The charges were notable, as the SEC enforcement action alleged that Under Armour engaged in manipulative revenue practices to conceal falling sales and struggling operations, but the company was not charged with accounting fraud. The charges against Under Armour were squarely focused on the lack of appropriate disclosure surrounding the revenue practices.

As addressed in the wake of Under Armour’s settlement, fraud charges by the SEC are serious enforcement actions and can stem from a litany of circumstances. A common culprit for accounting fraud is improper revenue recognition.

In general, regulators frown on types of accounting that massage revenue numbers specifically to conceal poor performance or meet earnings targets. There are a variety of revenue recognition practices that are permissible under GAAP and federal securities laws, provided the policies are disclosed to stakeholders. Without appropriate disclosure, certain accounting practices can mislead investors about a company’s profitability and growth.

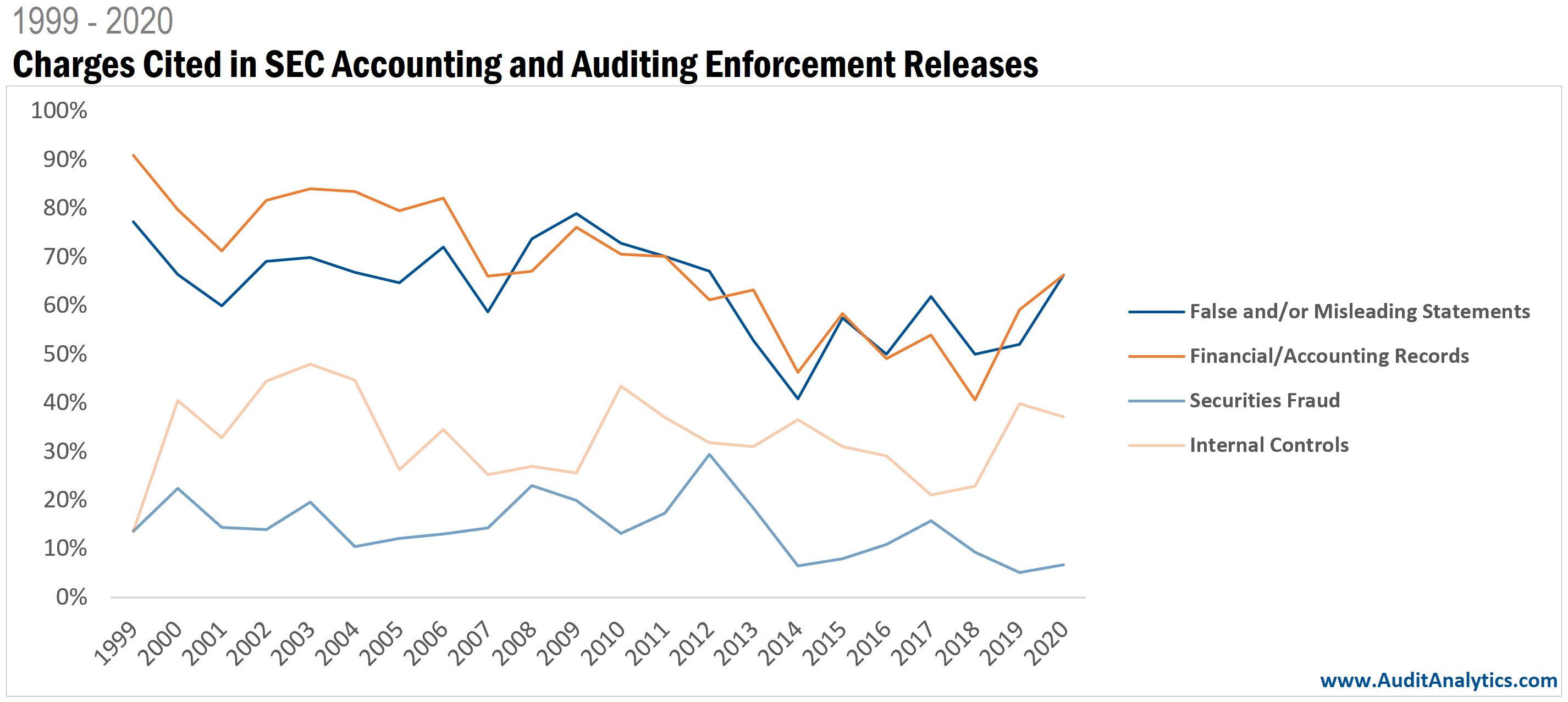

The SEC monitors financial reporting and accounting and issues Accounting and Auditing Enforcement Releases (AAERs) when a company commits a violation, including fraudulent activity and issuing misleading statements. There has been an evolution in these charges over time, as priorities and agendas change.

Overall, since 1999, 70% of AAERs issued cited charges related to financial and/or accounting records and 64% cite false and/or misleading statements. After the implementation of SOX, the charges related to those aspects began to diminish around 2006, but there were upticks in the number of AAERs citing false and/or misleading statements and financial/accounting record issues in both 2019 and 2020.

Securities fraud charges in AAERs are issued when evidence of illegal activity involving securities is uncovered, which may include lying on SEC filings, the intentional manipulation of stock prices, or accounting fraud. These charges are uncommon; only 15% of total AAERs since 1999 included a fraud charge. In the wake of the 2008 economic recession, there was an increase in fraudulent activity, but the amount of fraud charges in AAERs on an annual basis has been dropping from the high point seen in 2012. Notably, the AAERs issued in 2019 contained the fewest fraud charges in the last 20 years.

Many enforcement actions cite multiple charges due to the interconnected nature of financial reporting standards. For example, violations of internal control provisions are typically accompanied by issuing false/misleading statements, because the assessment on the effectiveness of internal controls must be signed off by management.

As with Under Armour, companies can also be charged with both financial record violations and issuing misleading statements to investors. In their case, though they were charged with disclosure violations related to revenue manipulation, they were not charged with fraud. The SEC previously charged another company, Nortel Network Communications, for similarly employing manipulative revenue practices, but additional circumstances, in that case, did result in a fraud charge.

Under Armour SEC Enforcement Action

On May 3, 2021, the SEC announced charges against Under Armour in regards to the company misleading investors about its revenue growth and failing to disclose known uncertainties concerning its future revenue. Under Armour agreed to pay a civil monetary penalty of $9 million to settle the matter.

The charges stem from actions taken by Under Armour beginning in 2015. At that point, Under Armour had an illustrious reputation, with more than 20 consecutive quarters of impressive year-over-year revenue growth. However, sales began to slow; warm winter temperatures were partly blamed for a decline in sales of high-priced cold-weather gear. In the third quarter of 2015, Under Armour’s internal revenue and growth forecasts fell short of analyst estimates; missing analysts’ revenue estimates could have had significant negative consequences for the company.

According to the SEC order, to avoid these consequences and continue to provide the appearance of revenue growth amidst slowing sales, Under Armour began pulling forward sales. Under Armour executed sales practices that incentivized their customers to agree to take product before the shipment had been requested. This allowed Under Armour to record revenue for orders that would have been placed in the future in the current quarter.

The revenue from the pull forward sales made it seem as though Under Armour was meeting or beating consensus estimates for the current quarter. To explain where the revenue was coming from, Under Armour falsely attributed it to increased sales; while the revenue did come from sales, it did not actually reflect an increase in sales. Employing this practice over six quarters in 2015 and 2016, Under Armour accelerated a total of $408 million in revenue.

The use of sales manipulations to accelerate revenue is acceptable under US generally accepted accounting principles (GAAP) and the SEC order “does not make any findings that revenue from [Under Armour’s pull forward] sales was not recorded in accordance with GAAP.”

However, Under Armour failed to appropriately disclose this information about its use of pull forwards and the significant impact on revenue. The sales pulled from future quarters to boost revenue could not be repeated in future quarters. Omitting this information misleads stakeholders about the nature of the revenue growth and whether the company could meet its revenue guidance in future quarters.

Under Armour settled the SEC charges related to disclosure failures that resulted in false and/or misleading statements; the company was not charged with fraudulent activity or misstating its financial results. While the material omission of certain disclosures is a violation of antifraud provisions in the federal securities laws and may warrant an enforcement action, it is not accounting fraud.

Nortel Network Corporation SEC Enforcement Action

There are instances of companies using revenue practices similar to Under Armour that did result in fraud charges from the SEC. In 2007, the SEC filed charges against Canadian telecommunications manufacturer Nortel Network Corporation related to two fraudulent accounting schemes, one specifically involving pulling revenue.

Similar to Under Armour, Nortel was suffering from slowing sales in 2000 when it became evident the company would not be able to meet its revenue guidance. As with other tech companies at the time, Nortel’s anticipated revenues failed to materialize in the wake of the dot-com bubble burst and the accompanying economic downturn.

In order to meet targets and their previously issued guidance, Nortel changed its accounting policies in a way that would allow them to accelerate the recognition of certain revenue. Company executives used this policy to inflate revenue in 2000 by accelerating $1 billion in revenue from bill-and-hold transactions. These transactions, which bill an account for undelivered inventory, are permissible per GAAP only if they meet certain criteria. Nortel’s transactions were not in conformity with GAAP criteria and the company was found to be improperly accelerating and recognizing the revenue.

This is where the circumstances for Under Armour and Nortel significantly diverge. The second accounting scheme Nortel employed involved the manipulation of reserves to meet targets and pay out executive bonuses, another GAAP violation. Nortel’s accounting schemes unraveled in 2003 and the situation became substantially more complicated; a restatement of $948 million was disclosed that was subsequently deemed to be a cover-up, and several executives were fired for cause.

The SEC brought civil fraud charges against several Nortel executives, including the former CEO and CFO, for their roles in the accounting fraud schemes. Eventually, the entirety of Nortel’s actions culminated in SEC enforcement, including charges related to violations of the antifraud, reporting, books and records, and internal control provisions of federal securities laws; the charges were settled for $35 million.

Nortel’s additional issues related to reserves and a materially false restatement to deliberately conceal misconduct understandably contributed to more serious charges and a more substantial monetary penalty.

Fewer than 10% of securities fraud charges result in monetary penalties. However, the amount of the average penalty imposed in SEC AAERs for securities fraud charges is nearly triple the average penalty for financial and accounting record violations.

One in four AAERs with charges related to financial and accounting record violations result in monetary penalties, but these charges are associated with a lower average penalty amount.

A high average penalty speaks to the serious nature of securities fraud charges. Worth noting, three of the top ten highest monetary penalties imposed by SEC AAERs cite securities fraud charges, including WorldCom’s massive $2.25 billion penalty in 2003 and American International Group’s $800 million penalty in 2006.

Though fraud charges are currently on a downward trend in SEC AAERs, the recent increase in the amount of enforcement actions citing false and/or misleading statements and financial/accounting record issues indicates the ongoing importance of those financial reporting aspects for SEC registrants.

Data in this analysis provided by Audit Analytics SEC Accounting and Auditing Enforcement Release Exploratory Research. Contact us for details.

Interested in our content? Be sure to subscribe to receive our email notifications.