The data found in SEC Comment Letters can offer insight into some overlooked areas of a company’s business. In the past year, we have discussed a continuous decline in the number of letters and major areas of concern raised by the SEC.

Previous posts, while providing

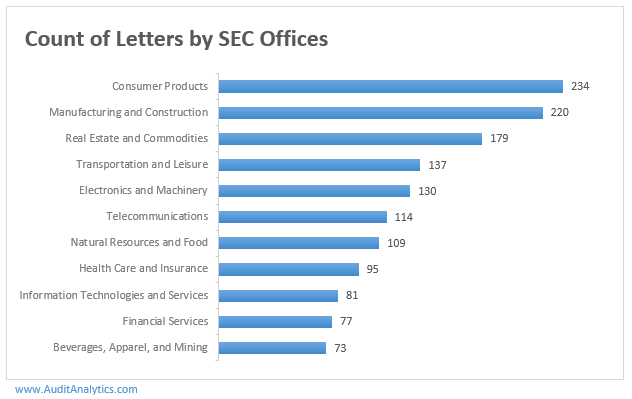

Let’s start with a high-level overview of the number of UPLOAD letters issued by each of the 11 offices of the SEC Division of Corporation Finance during 2016. (The UPLOAD form is for a letter from the SEC to a company. CORRESP forms are responses to the SEC from a company.) The Office of Consumer Products was at the top of the list with 234 letters written to 174 companies, followed by the Office of Manufacturing and Construction with 220 letters to 151 companies.

So much for the offices producing the most letters. In the following table, we thought it would be interesting to see who at SEC signed the most letters in 2016.

Not surprisingly, almost 60% of the letters were signed by the CFO, with an additional 14%

Interestingly, external counsel – indicated by “Law Firm” in the table to the right – signed 11% of all letters responding to the SEC.

Let’s take a further look at the role that third parties, such as law firms and accounting firms, play in the comment letters process.

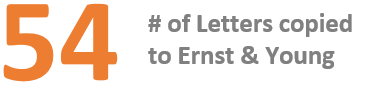

Between the years of 2010-2014, companies copied their auditor on

Law firms were copied by the companies they represent more than three times as frequently as auditors. In 2016, 692 (or 36%) of CORRESP letters copied their outside counsel. The top five firms named in comment letters are listed in the table below:

Vinson & Elkins topped the list with 38 letters, followed by Wilson Sonsini Goodrich & Rosati with 35 letters, Latham & Watkins with 30, Baker Botts with 25, and Goodwin with 19 letters. Overall, 160 different law firms were referenced in comment letters from the year 2016.

In some cases, law firms write and sign the CORRESP directly, instead of just being copied on correspondence from a company. For example, Valeant, the controversial pharmaceutical company, had at least two separate sets of Corp Fin reviews in 2016.1 In both cases, the responses came directly from their outside legal counsel, Skadden Arps Slate Meagher & Flom LLP. In total, 212 (or 11%) of the CORRESP letters were signed by the outside law firm.

We were curious to see how frequently comment letters are the subject of such attention. Another company that we discussed recently, MDC Partners,2 had a comment letter with an even larger crowd involved – 12 people in total.

The number of people alone can hardly be used as the only indicator to determine the significance of a particular comment letter. Yet, it seems reasonable that in some especially sensitive cases, companies would prefer to include additional parties in their outgoing correspondence.

Note: Our analysis is based on 1,506 UPLOAD and 1,908 CORRESP (3,404 total) letters dated between January and December of 2016. Only letters referencing 10-K, 10-Q, or 8-K filings were included.

1. Valeant’s CORRESP letters signed by outside counsel from August and October. ↑

2. MDC Partner’s CORRESP letter. ↑