Wrapping up our series on mutual funds, here we examine the market share for audit and non-audit fees by audit firm. The Audit Analytics’ Funds + Securities Audit Fee database tracks audit and non-audit fees paid by mutual funds to their independent audit firm at the series level.

Because fees are recorded at the series level, this analysis will exclude exchange-traded funds (ETFs) and variable insurance annuities. Audit fees for ETFs are usually disclosed at the registrant level. The registrant level will group the audit fees of several funds together. Variable insurance annuities are not required to issue form N-CSR; the form in which mutual funds disclose their audit fees.

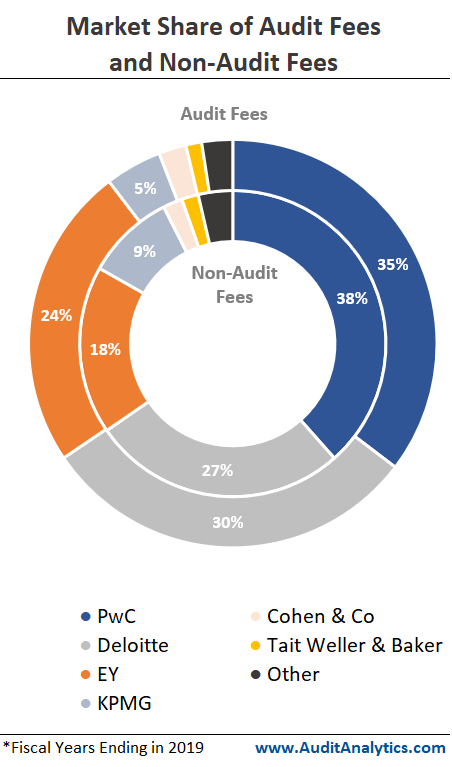

The Big Four audit firms earn 93% of audit fees and 94% of non-audit fees from fund clients. PricewaterhouseCoopers (PwC) holds the greatest market share with 35% of audit fees and 38% of non-audit fees.

Though regional firms audit a significant number of mutual funds, they earn a much smaller share of total fees. The regional firm with the largest share, Cohen & Co, earned 2% of audit fees and 2% of non-audit fees. This shows that clients of regional firms are likely smaller than those of Big Four firms.

When looking at fees by fund type, we see that just three firms – PwC, Deloitte, and EY – earn nearly all audit fees from money market and open-ended funds. PwC, alone, earns nearly half of all audit fees from money market funds and over 40% of fees from open-ended funds.

The market share for close-ended funds is much more competitive. Not only do each of the Big Four earn a more comparable amount of audit fees from close-ended fund clients, five regional and national firms each earn between 1% and 3% of close-ended fund fees.

The reasons for this may be twofold. First, close-ended funds pay much higher average fees per total investment. Meanwhile, money market funds pay much lower fees. And secondly, close-ended funds are smaller than money market and open-ended funds based on average total investments. The average total investment for close-ended funds was just $600 million, compared to $3.4 billion for open-ended funds and $11.7 billion for money market funds.

This analysis uses data from the Mutual Fund Audit Fees database, part of the new Funds + Securities module, powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.