Insured depository institutions with total assets above $500 million are required to obtain an audit of their financial statements by an independent auditor to comply with the Federal Deposit Insurance Corporation (FDIC) regulation Part 363 – Annual Independent Audits and Reporting Requirements.

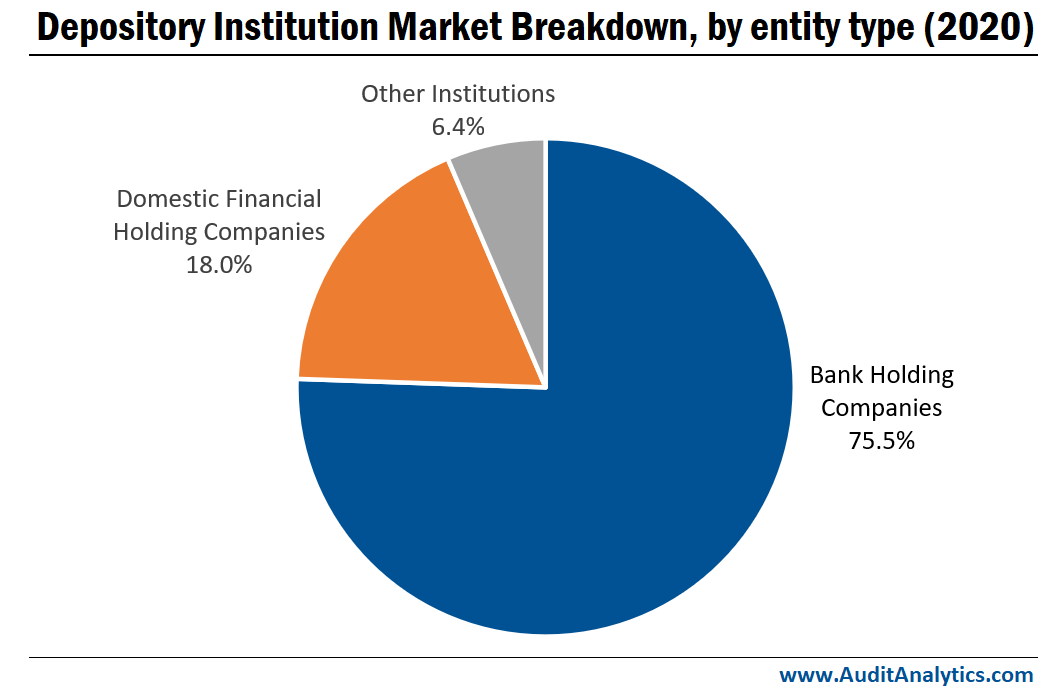

Most institutions fall into two groups: Bank Holding Companies (BHCs), comprising 75.5% of the market, and Domestic Financial Holding Companies (FHDs), comprising 18.0% of the market. However, the remaining 6.4% of the market consists of other smaller groups, including Other Domestic Entities, Savings & Loan Holding Companies, and Intermediate Holding Companies.

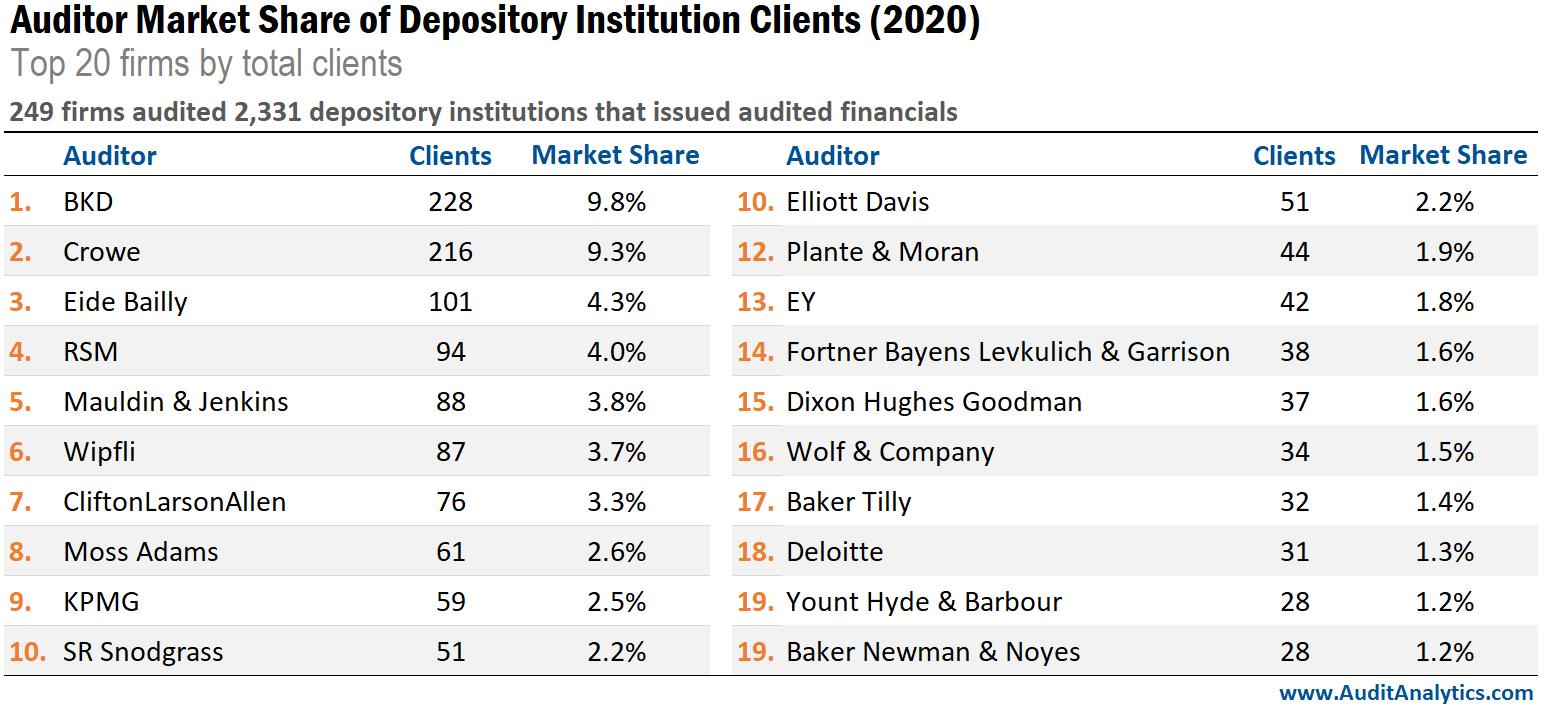

In contrast to the public company market, the Big 4 accounting firms do not audit the majority of insured depository institutions. As a result, the auditor market share of depository institutions is quite diverse. In 2020, 249 different firms audited 2,331 depository institutions that issued audited financial statements.

In the total insured depository institution audit market, national firm BKD leads with 9.8% of the market. Other non-Big 4 firms round out the top 5 auditors: Crowe, Eide Bailly, RSM, and Mauldin & Jenkins. Despite the diversity in audit firms, there is a concentration at the top in this market. The top 20 audit firms audit 61.2% of insured depository institutions. 229 audit firms share the remaining 38.8% of the market.

Bank Holding Companies vs. Domestic Financial Holding Companies

A bank holding company owns and/or controls one or more U.S. banks or has a controlling interest in one. Comparatively, domestic financial holding companies engage in a broad range of banking-related activities. This includes insurance underwriting, securities dealing, and investment advisory services. Because of diverse operations, financial holding companies have a greater amount of assets, necessitating a more complicated audit.

The auditor market share of BHCs and FHDs reflects the differences in the entities’ operations. The top 10 firms in the BHC market consist entirely of national and regional firms, with BKD in the lead. In contrast, the Big 4 firms have a bigger slice of the FHD market, collectively auditing 19.5% in 2020.

This analysis uses 2020 data from the OIA Financial Services – Bank Holding Company database, powered by Audit Analytics, and is based on auditor data pulled in December 2021.

Interested in our content? Be sure to subscribe to receive our email notifications.