Many times, people overlook out of period adjustments. Adjustments are a method of correcting errors in which prior periods are not revised or restated, and the error is corrected in the current period.

However, one is only allowed to use the out of period adjustment method for correcting errors that are immaterial to the period in which they occurred and immaterial to the period in which they are corrected. As a result, management must believe that investors will not care about the error.

Out of period adjustments can also be difficult for financial statement users to discover. In fact, many times, one has to search through the footnotes of the financial statements or management discussion and analysis (MD&A) to find the disclosure. And even then, one will often only find a single sentence with little detail.

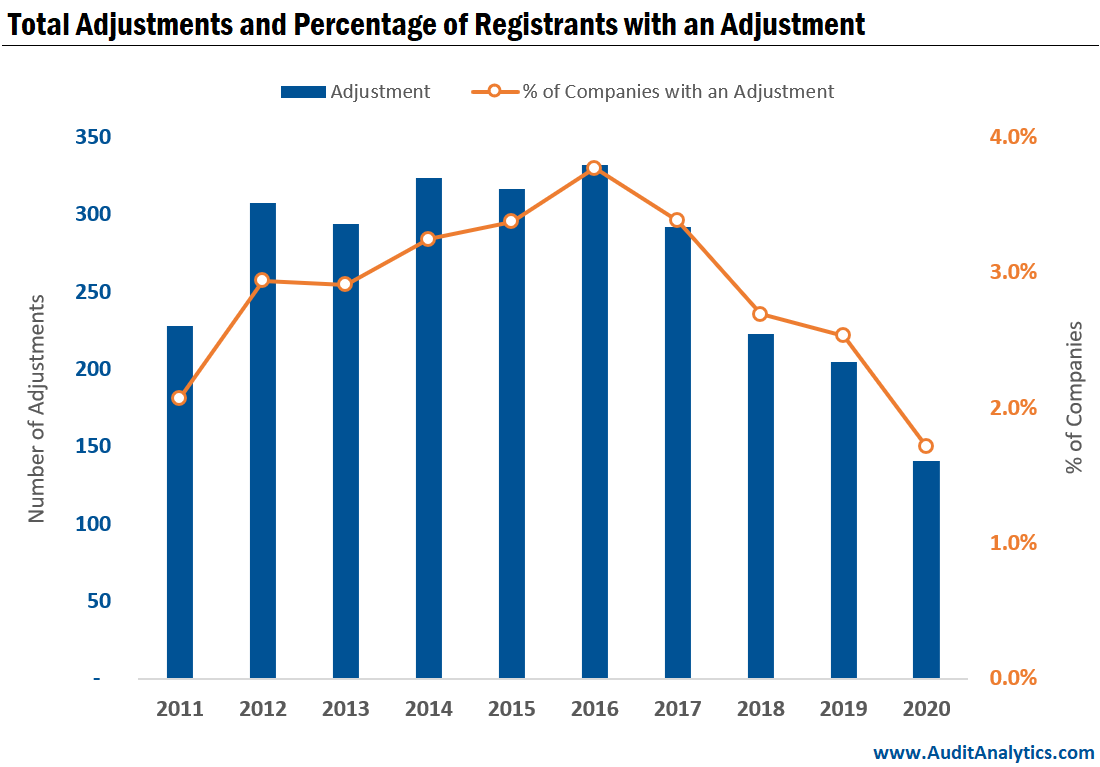

In the past few years, the number of out of period adjustments has been declining, similar to financial restatements. Adjustments were down 31% between 2019 and 2020. This represents just 1.8% of companies that issued a 10-K, 20-F, or 40-F in 2020, compared to a high of 3.8% in 2016.

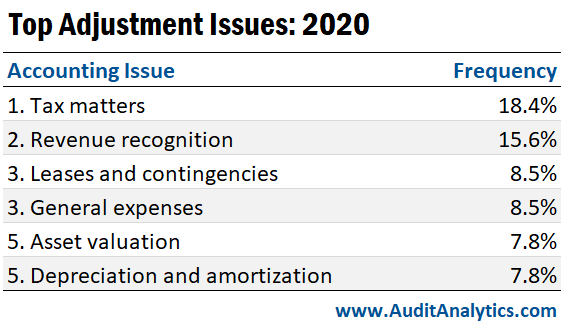

Overall, the most common out of period adjustment accounting issues are tax matters. In 2020, 18% of out of period adjustments referenced tax issues. Additionally, tax matters are the fourth most common issues cited in financial restatements. The recurrence of tax matters as the most common adjustment issue is a sign that taxes are a complex area of accounting but may not be a material account for investors. Also, the rise of non-GAAP reporting – which often excludes the impacts of taxes – could be evidence of the immateriality of taxes.

The second most common accounting issues are revenue recognition matters. For the past three years, financial restatements have cited revenue recognition matters as the most common accounting issues.

In 2020, leases and contingencies, general expenses, asset valuations, and depreciation and amortization round out the top five accounting issues. General expenses were the fifth most commonly cited accounting issues in financial restatements in 2020. The other three topics were outside of the top five financial restatement issues.

In conclusion, financial statement users should take note of out of period adjustments. While not as material as revision or reissuance restatements, adjustments are corrections of errors. Control deficiencies that result in adjustments may result in more severe restatements in the future. And companies that use the adjustment method repeatedly for correcting errors may have more severe issues with control systems and financial reporting.

Interested in our content? Be sure to subscribe to receive our email notifications.