Audit Analytics offers a suite of data products covering public companies listed on European exchanges across 31 countries in the EEA and Switzerland, which includes comprehensive databases of Audit Fees, Audit Opinions, Auditor Changes, Auditor Engagements, Key Audit Matters, and Transparency Reports. We currently track over 8,000 companies and more than 1,000 auditors.

We are excited to announce the addition of historical data back to 2010 for European Audit Fees and Audit Opinions. To kickoff 2020, we will be publishing a blog series, Decade of Data, highlighting this historical data in the following weeks.

In this post, we provide a closer look at the different Audit Analytics Europe databases and what they offer.

Audit Fees – Powered by a decade of data

Audit fees are an important component when tracking the audit market. This disclosure allows financial statement users to easily identify who audits who, in addition to the amount firms were compensated for their services.

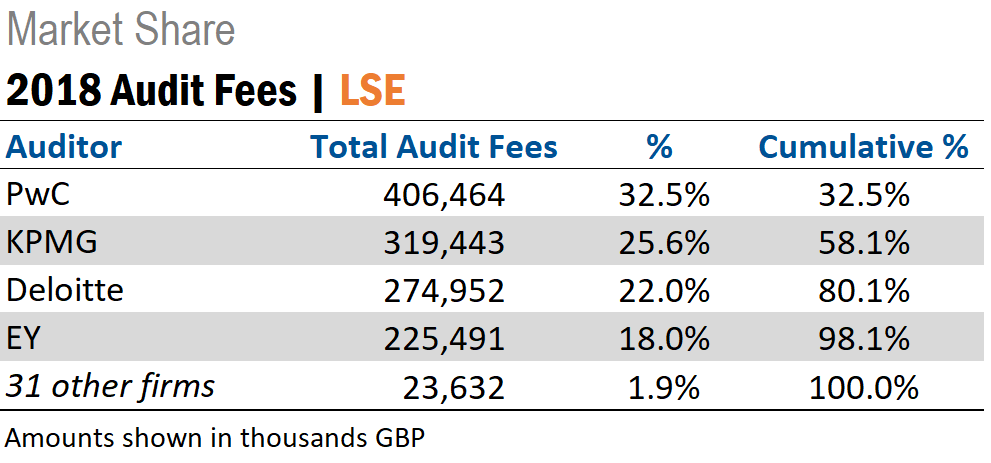

An analysis of audit fee disclosures can also provide unique insight into auditor market share. For example, looking at audit fees paid by LSE-listed companies in 2018, the Big Four firms accounted for over 98% of the cumulative audit fees, while the remaining 1.9% of fees was shared among 31 other firms – illustrating the heavy market concentration of the Big Four for LSE-listed companies.

The Audit Analytics Europe Audit Fees database contains audit, audit related, tax, and other fees paid to the independent auditor, and currently has over 73,000 audit fee records from more than 8,000 companies, dating back to 2010.

We will be featuring various analyses powered by this database in a couple of Decade of Data posts.

Audit Opinions – Powered by a decade of data

An audit opinion, also referred to as an auditor’s report, is a formal statement made by the auditor concerning a company’s financial statements, where an opinion is issued in regard to the quality or integrity of the reported financial information. The audit opinion serves as one of the primary sources for determining who audits who.

The Audit Analytics Europe Audit Opinion database tracks the audit firm and its location, the engagement partner, and any going concern modifications. This database contains over 64,000 audit opinion records from over 8,000 companies, encompassing 2010-present. With the majority of companies having a fiscal year end in December, these numbers will quickly increase over the next few months.

Auditor Changes

The choice of an audit firm is an important decision for a company. Typically, if a company changes its auditor, it’s for mundane reasons, such as mandatory auditor rotation, but there are myriad other reasons for which a company may change auditors.

The Audit Analytics Europe Auditor Changes database tracks auditor changes as disclosed in annual reports, annual general meetings, and press releases. Key data points include departing and engaged auditors, date of announcement, and the fiscal year to be audited by the newly engaged audit firm. A recent addition to this database includes whether the previous auditor resigned or was replaced due to regulation, and includes more information regarding the resignation, if provided, such as a disagreement between the auditor and the company.

Looking at auditor changes in specific markets can provide unique insight into underlying trends. For example, if a company changed from a Big Four firm to a smaller firm, or vice versa, it could be an indication that the company is looking to reduce fees or is looking for an auditor that can provide different services. It’s also important to note who initiated the change: the auditor or the company.

To date, we have over 4,000 auditor change records from more than 3,200 companies. Stay tuned for an upcoming blog showcasing this unique database.

Auditor Engagements

Knowing who audits who is critical for market intelligence, allowing users to gain valuable audit market insight and monitor auditor market share.

The Audit Analytics Europe Auditor Engagement database tracks current auditor(s) of record. This database helps interested observers identify the year in which an audit firm began auditing a particular company. For example, the graph below shows the auditor tenure frequency for companies listed on the Bolsa de Madrid.

From this, we can see that the majority of companies have auditor tenures of 0-5 years – which could mean the companies are newly formed or a change of auditor has recently taken place.

Key Audit Matters

Key Audit Matters (KAMs) are required under ISA 701 for fiscal years ending on or after December 15, 2016. Therefore, fiscal 2017 is the first full year of KAM disclosures.

The Audit Analytics Europe KAMs database tracks individual KAMs, normalizes the topic of the KAM, collects the text of the title, as well as the description, and the auditor’s response. To date, the database contains over 32,000 KAM records from the audit opinions of more than 4,000 companies.

We are noticing significant trends arising in the data, with larger companies (by market cap) reporting more KAMs, on average, per audit report. We are also noticing the number of KAMs decreasing year over year, but expect that number to level out as the new standard is normalized.

As mentioned in a recent post, the Big Four firms have remained relatively consistent with one another as far as the number of KAMs per audit report goes, ranging from 2.5 to 2.7 in 2018 opinions.

Transparency Reports

According to Article 13 of the Audit Regulation of 2014 (Regulation EU 537/2014), a statutory auditor of a public interest entity (PIE) must publish an annual transparency report on the firm’s website, at the latest four months after the end of each financial year. Among other disclosures, the transparency report must include a list of PIEs for which the statutory auditor or the audit firm carried out statutory audits during the preceding financial year.

Audit Analytics Europe tracks Transparency Reports published annually by EEA and Switzerland-located audit firms and the normalized names of all entities disclosed on each audit firm’s report. To date, we have collected over 3,000 transparency reports dating back to 2007.

The chart below shows the number of Transparency Reports published per country in 2018.

Our ever-growing European databases offer specialized information for academics and all users of financial statements.

We are thrilled to have access to historical data back to 2010 for our European Audit Fees and Audit Opinions databases. Be sure to check back for our Decade of Data series, highlighting these two data sets.

The analyses in this post were powered by the Audit Analytics European databases.

For more information on any of these European databases, or to request a demo, please contact us.