Critical audit matters (CAMs), as required by AS 3101, took effect for audits of large accelerated filers with fiscal years ending on or after June 30, 2019. The majority of large accelerated filers have fiscal years ending on December 31, meaning they were required to file their annual reports by March 2, 2020.

Now that we have passed some of the most major filing deadlines of the year, including the April 30th deadline for foreign private issuers, we figured it is a good time to reexamine CAMs.

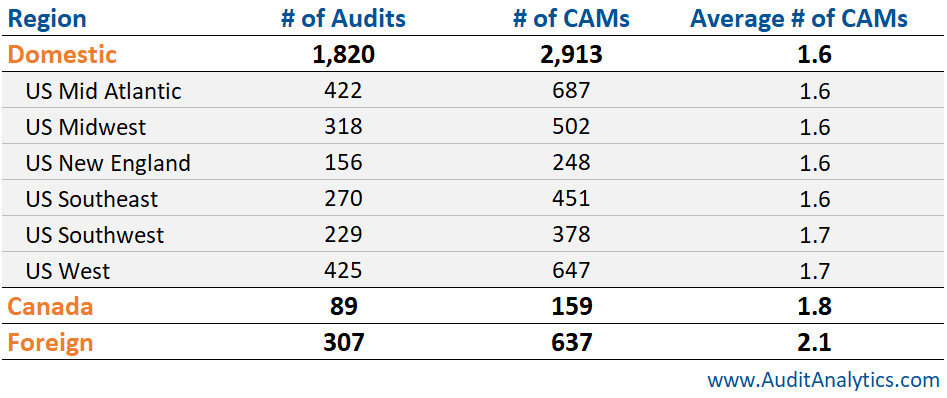

One of the most interesting trends we’ve began to notice is the difference in CAM count between domestic and foreign auditors. Looking at CAM counts across auditor locations, we see that firms located in the U.S. are reporting an average of 1.6 CAMs per opinion, while firms located in Canada are averaging 1.8 CAMs per opinion, and auditors outside of these regions are reporting an average of 2.1 CAMs per opinion.

To look at it from a different lens, the table below shows the breakdown of CAMs by form type. Again, we see that domestic forms (10-K, 10-K/A and 10-KT) average a significantly less number of CAMs per report than foreign forms.

Taking a step back, let’s look at the breakdown of CAMs by auditor. As shown, the Big Four collectively average around 1.7 CAMs per report. However, looking at the numbers across the individual firms, we see that EY averages the highest number of CAMs (1.8) and Deloitte averages the lowest (1.5). All other audit firms combined average 1.6 CAMs per audit opinion.

As a reminder, a CAM is any matter that the auditor communicated or was required to communicate to the company’s audit committee, and is related to items that are material to the company’s financial statements, as well as items that involved challenging, subjective, or complex judgment.

The most occurring CAMs to date reference intangible assets, revenue, and structure events. Together, these three topics account for almost 50% of all CAMs.

Goodwill and Intangible Assets

In order to assess goodwill and intangible assets, management must compare the fair value to its carrying value, a process that requires significant estimates for items such as cash flow forecasts, revenue growth rates, and discount rates. These significant estimates made by management in turn lead to a high degree of auditor judgment when evaluating goodwill and intangible assets.

Revenue

Determining the amount of revenue to be recognized is a complex process, especially when considering companies can have multiple sources of revenue. To evaluate revenue, it is necessary to determine a variety of factors including performance obligations, selling prices, and when to actually recognize the revenue. If company management must exercise significant judgment or rely heavily on estimates when determining revenue, the related audit effort may be extensive and require a high degree of auditor judgement.

Structure Events

Assigning value during an acquisition is not an exact science – it requires significant assumptions, including fair value estimates, forecasted revenue growth & operating expenses, and the valuation of intangibles such as customer relationships. Therefore, auditing a company’s valuation of acquired assets may be considered a CAM, as it may present a difficult task for the auditor to assess the significant judgments that are required by management in these types of transactions. On occasion, the valuation of assets may even require the audit firm to consult with subject-matter experts.

It is important to note that while these topics always necessitate estimation by management, they may not always be material to a company’s financial statements, in which case the auditor would not identify the topic as rising to the level of a CAM.

Additionally, auditors have been advised that CAMs are specific to the circumstances for each audit. Although certain topics may always require estimation, the CAM disclosure should address events specific to the audit for an individual company; if the same CAM language can be used for the same topic across multiple companies, it could indicate that the CAM disclosure isn’t specific to the circumstances.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.