The effects of climate change, and the accompanying disclosures, have risen to the forefront of the conversation for public companies. For example, in the US, the SEC has begun issuing climate-change-related comment letters.

There are a variety of impacts that climate change can have on a company’s accounting and financial reporting. These impacts largely depend on the specific circumstances of individual companies. As a result, the climate change issue is a prime candidate to appear in a critical or key audit matter (CAM/KAM) in a company’s audit report.

Audit matters require the auditor to provide more information about complex audit procedures relating to material or high-risk accounts, on an entity-specific basis. This includes areas of the audit that necessitated significant subjectivity or judgment.

Because climate change is an emerging issue with evolving impacts on companies and their accounts, the topic is inevitably making its way into audit matters. A text-search performed in the US CAM database, the Europe KAM database, and the Canada KAM database for select search terms related to climate change already reveals a variety of disclosures.[1]

Who Is Receiving Audit Matters Referencing Climate Change?

Location

Climate change is a global issue. As such, companies listed in the US, Europe, and Canada have received audit matters referencing climate change as a consideration.

In the US, SEC filings containing audit matters related to climate change are almost exclusively for foreign companies.

In Europe, significantly more audit matters discussing climate change have been disclosed than in the US. However, some specific metrics of ESG reporting are already mandatory in some European jurisdictions. For example, in the UK, greenhouse gas reporting disclosures have been mandatory for listed companies since 2013 under the Companies Act 2006.

In Canada, KAMs are a new requirement. However, several climate change references in KAMs were observed for Toronto Stock Exchange-listed public companies based in the UK.

Industry

Audit matters referencing climate change have appeared in every industry, except for Public Administration.

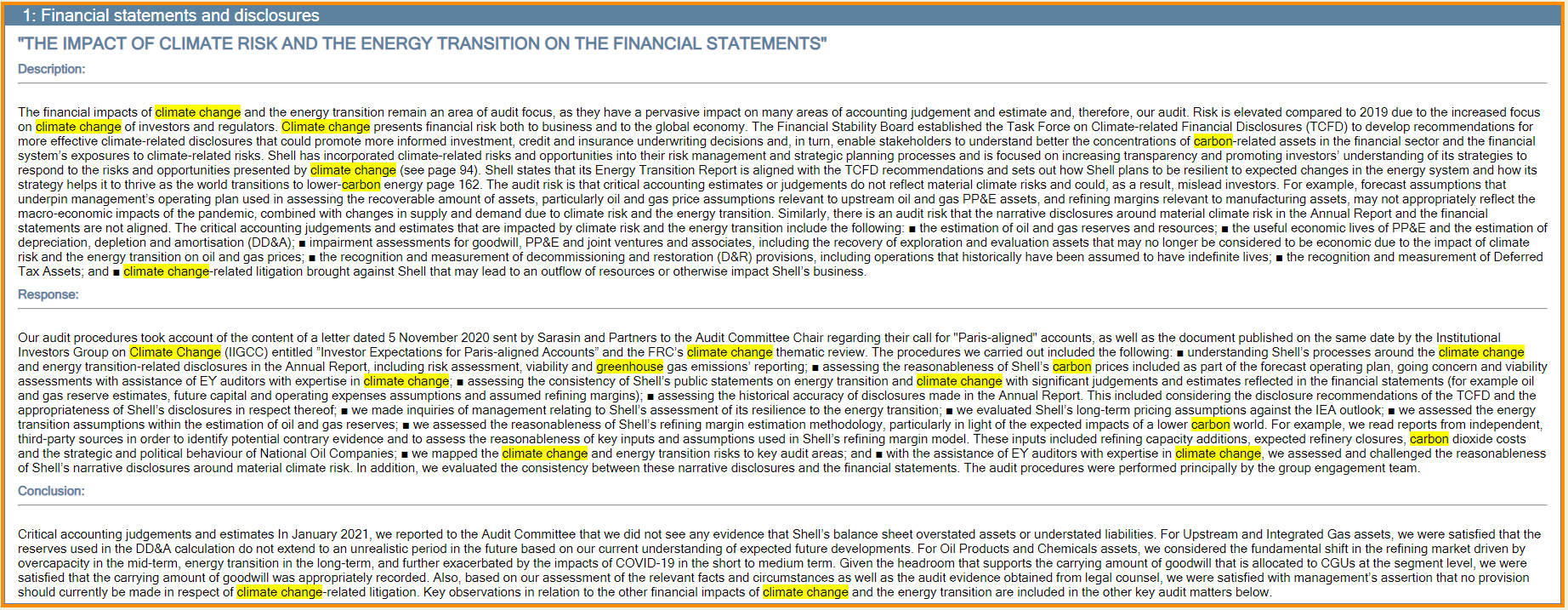

These audit matters appear most often in reports for companies in industries directly affected by current climate change-related regulations. This includes the Mining and the Manufacturing industries, with companies such as Shell, Rio Tinto, BP, and Chevron.

Other top candidates for audit matters referencing climate change are companies in the Utilities & Transportation industry. For example, the air and sea transportation companies easyJet and Gulf Marine Services, and utility company National Grid, have each received more than one audit matter related to climate change.

Size

More than half of the companies that have received climate change-related audit matters have annual revenues exceeding USD 1 billion.

Who Is Referencing Climate Change in Audit Matters?

The Big Four firms served as the auditor of record for nearly all climate-change-related audit matters observed. This is expected, due to the size of companies receiving these audit matters.

What Are the Audit Matter Topics?

There are a variety of audit matter topics referencing climate change. Overall, the majority relate to:

- Long-lived assets

- Property, plant, and equipment (PPE)

- Goodwill and other intangible assets

One emerging theme in audit matters related to climate change is the impact on asset valuation and subsequent impairment assessments.

Impairment assessments are notoriously subjective, based on forecasts and estimates of the future value of an asset. The addition of climate change considerations heightens that uncertainty and risk. Additionally, the potential for unknown factors – such as environmental regulations, shifting consumer trends, and commodity price fluctuations – further obfuscate asset valuation.

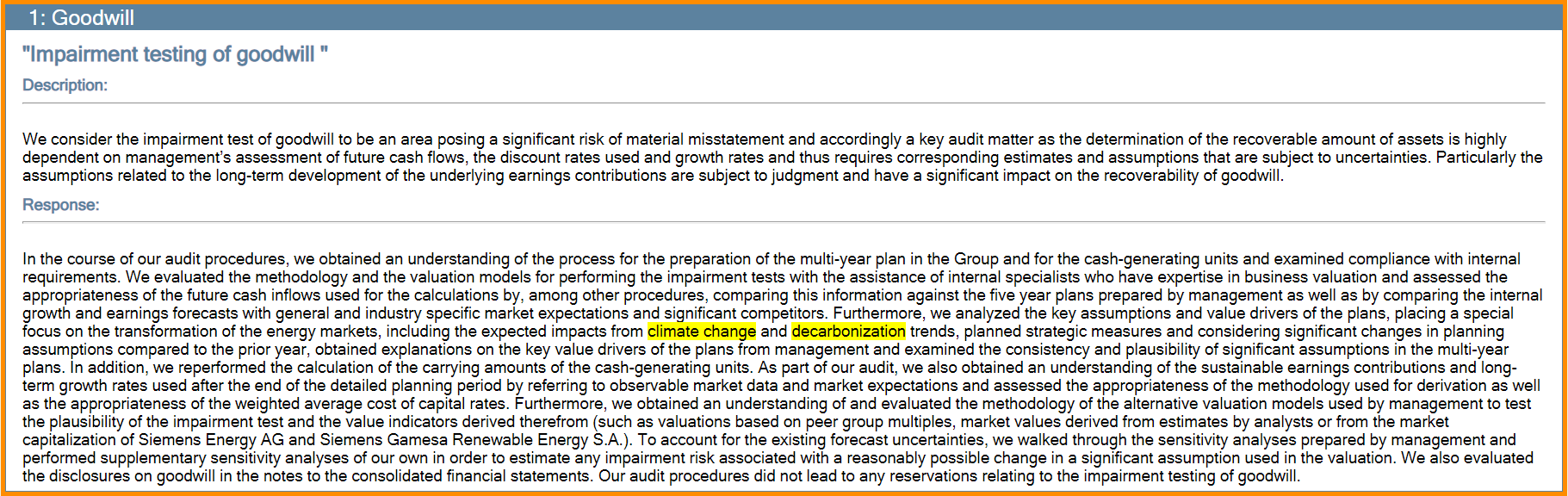

Consequently, these impacts are being broadly realized as they relate to impairment in multiple areas of financial statements. For example, Enel SpA, AES Corp, Anglo Pacific Group, and Siemens Energy all received an audit matter referencing climate change in the context of impairment assessments. Particularly, in determining the valuation of an asset over time in the presence of climate change initiatives.

Another emerging, although expected, theme in climate change-related audit matters are industry-specific matters for companies directly affected by climate change. For example, big energy companies, like BP and Shell, received audit matters broadly referencing climate change’s pervasive impacts on many areas of accounting judgments and estimates.

[1] Analysis based on data pulled in March 2022. Encompasses filings with fiscal year ends on or after January 1, 2020. Keyword search terms: ‘carbon’, ‘decarbonization’, ‘greenhouse’, ‘GHG’, and ‘climate change’.