On November 24, 2020, ExxonMobil Corporation [NYSE: XOM] issued a press release indicating that the company no longer plans to develop portions of its dry gas portfolio, resulting in after-tax impairments of $17-20 billion.

Like its competitors, a portion of Exxon’s property, plant, and equipment (PP&E) balance is based on “reserve”, or the estimated remaining quantity of product anticipated to be economically producible by the application of development projects to known accumulations. Changes in the corporate portfolio development strategy have led Exxon to abandon plans to recover these products, and as such, the company must adjust the portion of PPE attributable to remove the amount previously recognized as an asset.

A $20 billion impairment would be the second largest seen in the industry over the last 15 years. This would reduce the company’s PP&E balance by approximately 7-8% and their overall assets by approximately 5-6%.

Regarding ExxonMobil’s lack of impairment, former Exxon Chief Executive Rex Tillerson told trade publication Energy Intelligence that asset resiliency was a result of the high level of burden the company placed on executives to ensure that project worked at lower prices, and the accountability the company held executives; “We don’t do write downs…we are not going to bail you out by writing it down.”

The company’s lack of asset write downs has attracted a significant amount of scrutiny and attention from analysts, as well as probing from regulators.

In 2013, the SEC issued a series of comment letters regarding the company’s lack of impairment testing for North American upstream assets for impairments during fiscal year 2012 despite “statements made by [Exxon] senior management during 2012 which indicate that you [the Company] was making “no money” on U.S. natural gas due to low prices that had fallen below the cost of production”.

The SEC closed the comments and engaged in no enforcement action in relation to this matter, but the exchange underscores the abnormality of the company’s accounting practices.

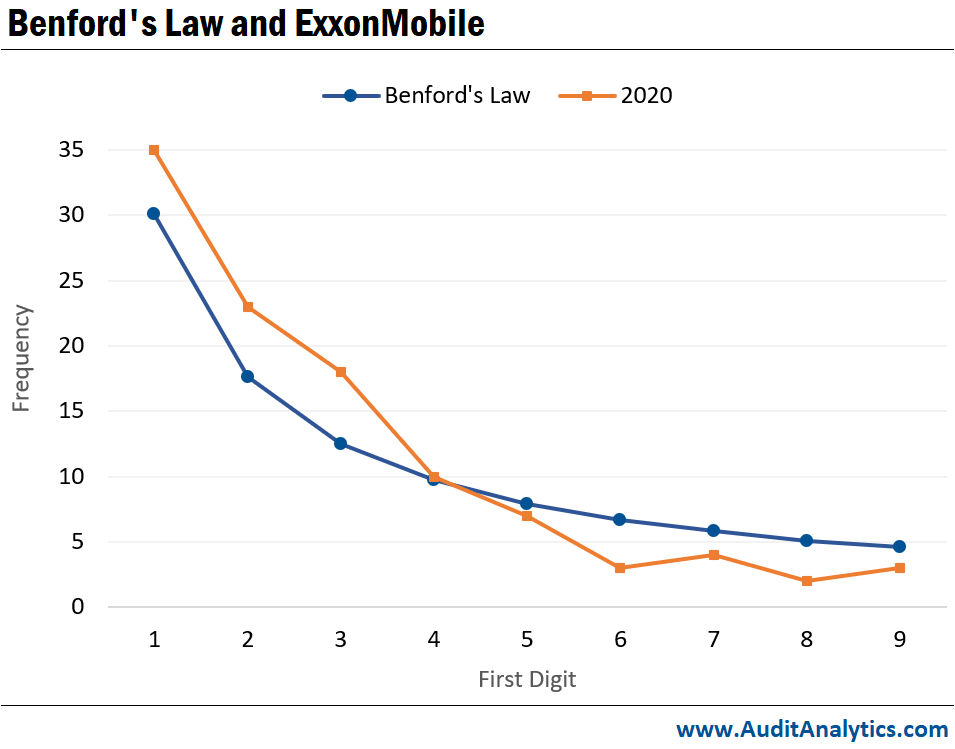

Benford’s Law has been a tool many analysts leverage when assessing the reliability of financial reporting. First hypothesized by Frank Benford, a physicist at General Electric in the 1930s, the mathematical theory holds that the distribution of the first digit in a given set of data tend to follow a predictable pattern. A growing body of research has supported that deviation from Benford’s law can indicate clerical errors, earnings management, or fraud. Amiram et al.’s 2015 paper “Financial statement errors: evidence from the distributional properties of financial statement numbers” found that when restatements occur, restated numbers tend to more closely conform to Benford’s law; “there exists a relation between the level of divergence from Benford’s Law and the informational quality of the reported financial statements”. Interestingly, Alali and Romero’s 2013 study “Benford’s Law: Analyzing a Decade of Financial Data,” found “likely manipulations across different analyses” for several accounts, including net PPE when looking at large U.S. public company restatements over a 10-year period.

Our analysis of Exxon’s financial statements indicate that the company has deviated from Benford’s Law since fiscal year 2017.

Exxon’s impairment indicates that the company’s estimated cash flows from capital expenditures no longer meet expectations. The November asset write-down primarily involves dry gas assets in the U.S. and Canada, and Argentina, many of which are part of subsidiary XTO Energy Inc.

New technologies have led to unprecedented supplies of oil and natural gas products that has radically outpaced global demand. At the time of the 2010 XTO acquisition, U.S. natural gas prices averaged $5.31 per thousand cubic feet; since then, the average has declined nearly every month reaching a low of $2.08 in June.

At a 2019 KPMG conference, former executive Rex Tillerson admitted the company “probably paid too much” for the XTO acquisition. If the impairment primarily involved assets acquired in the $31B XTO deal, equal to nearly 2/3 of the value of the acquisition, it is questionable how long-term forecasts of cash flows could have remained unchanged over the course of 10 years. The Benford abnormalities could indicate such an impairment was long overdue; the quality of previously issued financial statements should be assessed.

Further, the WSJ recently reported the SEC’s investigation into ExxonMobil after an employee filed a whistleblower complaint regarding the company’s Permian Basin asset valuation. The Permian Basin accounts for nearly 40% of all US oil production, and nearly 15% of natural gas production.

According to the WSJ, Exxon managers determined the net present value of the Delaware Basin, Exxon’s most promising Permian Basin area, at about $60B in 2018. According to the whistleblower complaint, in 2019, employees in the company’s development plan estimated the value closer to $40B after adjusting for longer than expected time to drill wells in 2018. After submitting the revised estimates, a manager allegedly asked the employees to “claw back” some of the value and use a more optimistic “learning curve” that some employees viewed as unrealistic. In response, one employee submitted the revised estimates in a file named “This is a Lie”, and the development planners’ final estimate recorded net present value at $50B.

In a rapidly evolving global environment, the future of oil and gas is unknown. Regulators should be cognizant of the pressure declining margins, environmental regulation, and changes in consumer behavior places on management and the overall risk environment. Quality financial reporting is invaluable to stakeholders, and in these trying times, it is important for those working to protect the interest of stakeholders to maintain an appropriate level of skepticism, particularly when faced with unrealistic or unbelievable reports from management.

This analysis uses data from the Impairments database, powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.