Key Findings

- Computing the cumulative average abnormal return (CAAR) to document market reaction after a financial restatement, we found no significant abnormal returns in either the first 30-day window following the date of restated financials or after a 90-day window for all populations tested

- Conversely, abnormal positive returns following a restatement were identified in the second 30-day window after the date of restated financials for all populations analyzed

- For restatements with a lengthy investigation process, there may be additional windows with abnormal positive returns

Introduction

A financial restatement is perhaps the most significant indication of an accounting failure. Inability to provide reliable financial statements may shake investor confidence and raise concerns about the overall health of the company. Moreover, a material restatement caused by an accounting irregularity may cast doubt on management integrity and expose the company to regulatory scrutiny or litigation.

In this study, we use the buy and hold method and look at price movement following the restatement. Although prior research documents notable, negative returns before and around the announcement date of the restatement, we identify long-term positive abnormal returns of up to 3.28% following the resolution of the restatement process and filing of the restated financial statements.

Negative consequences of financial restatements are well documented in the academic literature. For example, Hennes et al. (2008) found significant abnormal market reaction associated with accounting irregularities. The study also identified a positive relationship between irregularities and C-level employee turnover rate.

More recently, Myers et al. (2013) documented that restatements disclosed in periodic SEC filings or amended SEC filings generate less severe negative returns than restatements disclosed in an 8-K filing. The study also finds that returns are increasingly negative for restatements that have a negative effect on net income or a large positive effect on net income; and when there are allegations of accounting irregularities or when a restatement involves revenue recognition practices.

Finally, findings by Drake et al. (2015) suggest that short selling intensifies around a restatement announcement and that abnormal negative returns occur for the period between 20 and 30 trading days after the restatement announcement. Although the study documents abnormal returns for the 40-days holding window, the magnitude decreases and becomes insignificant using a 50-trading day holding period. The study finds that stocks of smaller companies are more likely to be mispriced and become targets of short selling activity.

Although studies around the restatement announcement date are extensive, post-event stock price movement is less documented and, in our opinion, such a study would therefore be worth exploring.

First, the short-term analysis around the restatement announcement date is primarily concerned with documenting abnormal negative returns immediately after news of the restatement becomes public. It is equally important to examine whether abnormal returns persist after the restated financial statements are filed and the restatement issue is remediated. In other words, it would be beneficial to determine whether there is a delayed market reaction and whether more negative events are expected.

Lack of reliable information during the restatement process, as well as limited financial guidance, may cause the market to initially misprice bad news for companies undergoing a long restatement process. This could create a window of opportunity for abnormal positive returns after the market corrects from the exaggerated reaction to the news.

Although some companies file restated financial statements as early as the next day following a restatement announcement, for other companies it can take years to complete the restatement process. During that time, companies may become delinquent with financial reporting, raising the risk of delisting[1]. In addition, when companies go dark, financial information available to investors is likely to be reduced. Target groups, such as large institutional investors focused on the “G” (governance) element of ESG investing, may avoid investing or increasing their position in the stock while the restatement process is ongoing.

To take full advantage of positive corporate developments, companies may choose to delay dissemination of positive news, such as new product announcements, until the remediation process is complete. For example, companies with restatements that were followed by a C-level turnover may decide to delay positive news until the new management comes on board.

To summarize, due to lack of reliable information during the restatement process and possible limitations on large institutional players to investment in companies with poor governance, there may be an opportunity to generate positive alpha.

Data and Methodology

Consistent with Myers et al. (2013), we begin our analysis with restatements disclosed in 8-K filings available in the Audit Analytics database. The population was limited to non-reliance restatements, defined as restatements that have an 8-K Item 4.02. The sample consists of 5,111 observations, for the period beginning January 2005 to December 2016.

We further exclude 2,465 restatements for which the date of restated financial statements is unavailable in the Audit Analytics database (e.g., such as companies quoted on the OTCBB). Audit Analytics collects dates of restated financials only for companies that are traded on a major exchange (e.g. NYSE, Nasdaq and AMEX). A restatement date could also be missing because a company was delisted from an exchange, was acquired before the restated financials were filed or, for newer restatements, because the restatement process is still incomplete.

We obtain stock return data from the Xignite database. After matching restatements and stock return datasets, an additional 1,111 observations were excluded for which returns were unavailable.

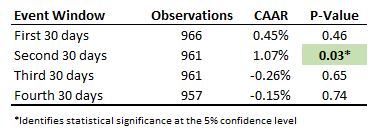

To include only restatements with long restatement processes, the sample was further reduced by 513 observations where restated financial statements were filed on the same date that the restatement announcement was made. 56 observations for which stock price on the restated financial date was below $1 were also excluded from the sample. Our final sample consists of 966 observations (see below):

In order to study the overall market reaction, we first measure the cumulative abnormal return (CAR) associated with each event by calculating daily market-adjusted returns. We then sum up these daily market-adjusted returns, for twenty-five 30-day incremental window intervals, for a period of up to 750 days following the date of restated financial statements.[2] In our calculations, we consider the Russell 3000 index as representative of the market. We, then, calculate the cumulative average abnormal return (CAAR) for the overall sample by computing the average of all CARs in our sample. We expect the stock prices to be volatile and positive rallies to be short lived, so we believe that short-term 30 days windows to be more appropriate for the analysis than 750 days buy-and-hold approach.

Results

Overall population –Based on an assessment of the overall population (966 observations), no statistically significant abnormal returns were identified in the first 30-days window following the date of the restated financials.

However, significant positive abnormal returns of 1.07% were identified during the second 30-day window (days 31 to 60). This finding is consistent with our theory that the market may overreact and create a short-term positive returns window after the initial impact of the bad news.

We extend the analysis even further to up to 750 days following the restatement and identified abnormal positive returns of 1.55% in the event window of days 271 to 300 and abnormal returns of 1.52% in the event window of days 331 to 360. We did not identify any windows with abnormal negative returns.

Population of restatements with net income effect – Following Myers et al. (2013), we further examined whether positive abnormal returns increase when a restatement is perceived to be more significant, such as restatements with impact on aggregate net income.

Similar to the original sample, no abnormal returns were identified in the first 30-day window, but for the second 30-day trading window, abnormal returns of 1.16% were identified.

We also identified cumulative average abnormal return of 1.79% in the event window 271 to 300; and cumulative average abnormal return of 1.66% in the event window of 331 to 360. We did not identify negative abnormal returns in any of the event windows.

The sample population of restatements with net income effect contained 859 observations, in comparison to the original sample of 966 observations. In other words, about 90% of the non-reliance restatements had at least some effect on the aggregate net income. This is because, in general, restatements with no income effect are perceived to be less material and do not require an 8-K Item 4.02 filing.

Population of restatements with long restatement process – To further differentiate between restatements that are resolved quickly and restatements subject to lengthy internal investigations and remediation processes, we looked at a subset of restatements where the number of days to restate exceeded 30 days (Table 4, see also). For the purpose of this analysis, the number of days to restate is calculated as the number of days between the filing of an 8-K Item 4.02 and the day when restated financial statements are filed. Whether a firm qualifies to be in this sample can only be determined after 30 days has elapsed as it would not be possible to trade during the first 30-day period.

Our subset of long restatements includes 431 observations, in comparison to 966 in the original sample. The drop in the number of observations further emphasizes that companies are able to resolve the restatement issue within a relatively short time frame in more than 50% of the cases.

Consistent with previous samples, we found abnormal positive returns of 1.74% in the second 30-day window. Notably, we identified abnormal negative returns of 2.67% in the third 30-day window. This is different from the previous tests in Tables 1 and 2, where no abnormal returns were identified.

As with the previous tests, we identify abnormal positive returns of 2.48% in the event window 331 to 360 days. No abnormal negative returns were identified in any of the windows except the third window (61 to 90 days).

The significance of this finding, from an investor’s perspective, is that the share prices of companies with a long restatement process may continue to be volatile or underperform long after the restated financials are filed. Yet, the negative abnormal returns are short-lived.

For the population of restatements with a net income effect, there are similar results: abnormal positive returns of 1.91% in the second 30-day window and abnormal negative returns of 2.39% in the third 30-day measurement window.

The cumulative average abnormal return for the 331 to 360 days window was 2.74%.

The conclusions above are based on the statistical information using the buy and hold strategy for various windows. Yet, catching a falling knife could be dangerous and cannot be projected on individual stocks.

Summary and Conclusions

In this analysis, we aim to provide actionable information for investors exploring price movement following the completion of the restatement process.

Although academic literature provides evidence of underperformance of restating companies, investors may find value in understanding stock behavior after companies clear regulatory issues related to the restatement process.

Overall, our cursory results are consistent with the results documented by Drake et al. Although the authors discussed short selling activity following the restatement announcement, it is likely that short selling activity would gradually subside following the filing of restated financial statements.

Our broad-stroke analysis is intended to be a starting point of a more detailed study and should not be seen as a fully developed trading strategy. For example, it is possible that documented abnormal returns are concentrated within sectors or stocks priced below $5 a share. We also do not take into consideration factors such as trading costs and volatility of the restating companies.

It is also possible that companies with abnormal returns (either positive or negative) share certain factor-based characteristics not possessed by the remaining population. For example, looking at a case study of Bausch Health Companies Inc. [BHC] (formerly Valeant Pharmaceuticals International Inc. [VRX]), the company was highly leveraged, with a tangible risk of default on its loan agreements.

Moreover, our analysis looks at restatements that originated as early as 2005. We cannot rule out the possibility that if we looked at a more recent population (let’s say five most recent years) we would have produced different results. Restatement characteristics such as errors vs. irregularities and regulatory environment could have impact on the stock behavior.

Yet, we think the study is interesting and identifies a few points that warrant further analysis. For example, not a single population tested had statistically significant abnormal negative returns after the 90 days following the restated financials date while, for the population with a lengthy restatement investigation process, there could be short-term windows with abnormal positive returns.

For more information on this article, or regarding our financial restatement database, please contact us at info@auditanalytics.com or (508) 476-7007.

This article was first available to subscribers of Accounting Quality Insights by Audit Analytics on Bloomberg, Eikon, FactSet, and S&P Global.

[1] For example, on November 7, 2018 MiMedx (previously traded on Nasdaq as MDXG) was delisted following the internal investigation into revenue recognition practices and related inability to file financial statements.

[2]We sum up returns (cumulate), instead of compounding them to conduct conventional tests of statistical significance. The compounded returns to a buy and hold strategy in excess of the compounded market returns may therefore be different from the ones that we present in our tables. These differences, however, are unlikely to be significant given the short event windows that we analyze.