Audit Analytics recently released its most recent report, Nineteen Year Review of Audit Fee and Non-Audit Fee Trends. Using data from our Audit Fees database, this report provides a detailed analysis and comparison of trends in audit and non-audit fees disclosed by public companies between 2002-2020.

Analyzing the total fees paid to external auditors is of interest because it provides insights into both audit risk and auditor independence.

Audit fees are an indicator of audit complexity and risk. Higher risk audits require more auditor resources to reduce audit risk to an acceptable level. Analyzing fees by industry, company size, and location illustrates the level of risk and auditor effort across various sectors of publicly listed companies.

Furthermore, non-audit fees are of interest, both domestically and internationally. Regulators consider high non-audit fees to be an auditor independence concern, an area receiving increased attention in recent years.

Report Highlights

The most interesting findings from the analyses in this report edition include:

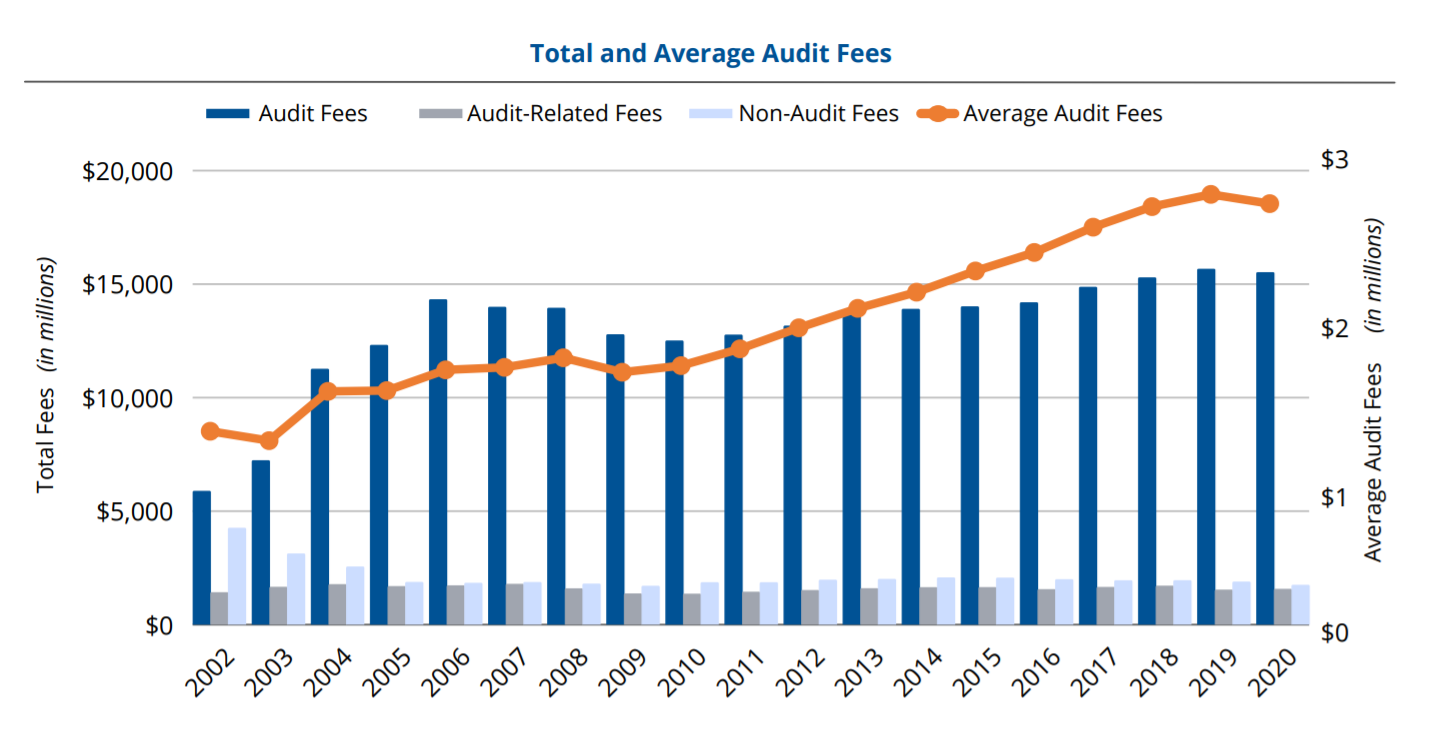

- Aggregate audit fees paid by public companies fell for the first time since 2010.

- Similarly, average audit fees fell for the first time in a decade.

- The amount of non-audit fees fell to a record low of total proportionate fees.

Audit fee trends were impacted by several external events during fiscal year 2020. The COVID-19 pandemic necessitated modified audit procedures, subsequently lowering audit costs. Additionally, regulatory changes altered the composition of companies filing as accelerated filers. This resulted in the audit fee to ratio revenue falling for accelerated filers during the year.

To access the full report, click here. Audit Analytics subscribers can download the report from their dashboard.

Interested in our content? Be sure to subscribe to receive our email notifications.