Note: This article was first available to subscribers of Accounting Quality Insights by Audit Analytics on Bloomberg, Eikon, FactSet, and S&P Global. For recent updates, please contact us.

Introduction

For nearly two years, we have monitored U.S. public companies’ progress toward implementing the new revenue recognition standard known as ASC 606 – Revenue from Contracts with Customers, which (for public companies) went into effect for fiscal years beginning after December 15th, 2017.

The complexity of the standard and lack of comparability to previous financial statements caused investors to be confused about which standard (old or new) was used and the impact on financials. To help investors understand the complex disclosure, we used simple metrics (described below) to benchmark the implementation practices and corresponding disclosures:

- Adoption rates and method

- Impact of the standard on financial statements, including revenue, net income and retained earnings

- Disclosure of remaining performance obligation and disaggregation of revenue by the revenue stream

- Number of reconciling lines in comparison of the old ASC 605 and new ASC 606 standards

As a reminder, ASC 606 standardizes and simplifies how companies record revenue in customer contracts across industries. Despite its intention to simplify revenue from contracts, many companies have been underprepared to adopt the new provisions. The standard itself is very complex and can involve major process changes – especially affecting accounting processes but may also affect other areas, including human resources and information technology. In some extreme cases, companies were even forced to restate previously filed financial statements to correct the application of ASC 606.1

We’re seeing the impact ASC 606 is having on companies in the latest batch of earnings releases. These are the last updates before the annual reports are filed this spring. The annual reports should contain expanded disclosure, so we thought it would be worthwhile to review Q4 2018 data of the S&P 500 companies to see how the companies are faring prior to filing annual reports.

Adoption Rates

As expected, most companies with fiscal years ending in December already adopted the new standard, and those with a fiscal year ending in October and November will adopt soon. Eleven companies said the standard was not expected to be material and did not provide any disclosure or footnotes. If adopting the standard is material, and a footnote or disclosure is missing, the Securities and Exchange Commission (SEC) will likely comment and request the company adds the disclosure. There also could be implications on controls and procedures.

In the example below, the SEC expressed concerns over missing ASC 606 disclosure and requested further clarification about the effectiveness of disclosure controls:

Please revise your disclosure to provide your accounting policy on revenue recognition as a result of your implementation of FASB ASC 606. Please refer to the guidance in FASB ASC 606-10-50 and Article 10 of Regulation S-X.

Response: Disclosures attributable to ASC 606 are presented in the Amendment No.1 to the 10-Q.

Item 4. Controls and Procedures, page 25

Please revise your disclosure to provide your conclusion on the effectiveness or ineffectiveness of your Disclosure Controls and Procedures. In addition, please provide a detailed discussion on how the non-disclosure of your revenue recognition policy in this Form 10-Q affected your conclusion.Response: Management has determined that its disclosure controls and procedures were effective and has included its conclusion in the Amendment No.1 to the 10-Q. During the quarter ended December 31, 2017 and during the audit review process, the Company assessed the impact of FASB ASC 606 and discussed with its independent registered accountant. Management’s determination was that FASB ASC 606 would have no impact on the Company’s financial performance or results. Although the Company did not disclose its consideration of ASC 606 in its Form 10-Q, the Company does not believe that this impacts its conclusion that its disclosure controls and procedures were effective in light of the fact that the impact of ASC is immaterial to the Company’s financial results.

Adoption Method

When implementing ASC 606, companies could use one of two methods – a full retrospective or a modified retrospective. About 80% of S&P 500 companies used the modified retrospective, so they did not restate previously filed financial statements. That makes comparing current results to previous years’ earnings much like comparing apples and oranges.

A full retrospective makes disclosure more transparent and easier to compare; however, it is more work for the companies and harder to implement. Most companies have opted for the modified retrospective method that does not require restating previous financial statements, as this method is easier to implement.

Impact on Financial Statements

When analysts review earnings that reflect the old and new accounting methods, especially if the modified method is used, they need to consider how much the standard altered revenue numbers. With the modified method, financial statements for prior periods are presented under the old standard, while the current period is presented under the new standard, making the comparison difficult.

We reviewed the impact of ASC 606 across three categories: net income, revenue and retained earnings.

For the companies that used modified method, the standard had a positive median effect of $7.3 million on revenue and $3.4 million on income for the first nine months of 2018. Overall, 150 companies disclosed an aggregate revenue impact of about $7.4 billion, and 97 companies disclosed a positive income effect of $2.5 billion. (Note that the data above is for companies that used modified method only).

The magnitude of the impact varied significantly between the companies and, in some cases, the direction of the change is not easy to determine. For example, to illustrate the presentation challenges, let’s take an example of Philip Morris [PM]. The company made the policy election to “exclude excise taxes collected from customers from the measurement of the transaction price, thereby presenting revenues, net of excise taxes”. In other words, the net revenue declined by a staggering $36 billion. Yet, the company still presents the top line of the income statement as “Revenue before excise taxes” – which pre-adoption was called “Net Revenue”. The impact on net income was not material since offsetting amounts on the income statement were affected

Of note is that Philip Morris used the full retrospective method and restated previously disclosed financial statements for the adoption. In general, for companies that elected the full retrospective method the impact appeared to be more material with average impact on revenue of $280.4 million and median impact of $8.4 million, in comparison to average impact of $49.0 million and median of $7.3 million for modified retrospective adopters. (The numbers exclude Philip Morris because technically the top revenue line did not change).

One of the challenges in estimating the pre-adoption impact was lack of quantitative disclosure. Only 55 companies quantified expected impact of the standard in the pre-adoption SAB 74 disclosure on revenue; 118 on retained earnings; and 21 on income. Most of the companies that did provide such an estimate were accurate with their preliminary numbers. For example, General Electric [GE] disclosed in its annual report filed on February 23, 2018 estimated impact retained earnings to be $4.2 billion and the final impact of $4.24 billion. In another example, General Motors [GM] estimated $1 billion reduction of retained earnings and disclosed final impact of $1.3 billion.

Also, the companies that gave pre-adoption estimated impact on revenue were more likely to have larger positive impact – the median impact on revenue for the companies that did provide the SAB 74 estimates was $61.9 million, in comparison to $5 million for companies that disclosed only the final actual numbers.

The impact of the standard varied greatly between industries.

Additional Disclosure

We also wanted to see the impact of important new metrics that are now required to be disclosed under ASC 606. One new metric is the remaining performance obligation (RPO), which shows how much revenue the company expects to record from existing contracts. Accounting rules say the revenue can only be booked after contractual obligations are fulfilled.

Our analysis shows that, of the 451 companies that have provided post-adoption disclosure, 142 companies provided remaining performance obligation disclosure., These 142 RPO disclosures had an average of $13.9 billion, median of $1.6 billion and maximum of $491.2 billion.

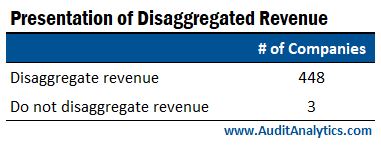

Yet, another provision of ASC 606 requires more detailed revenue streams disclosure, which provides better visibility into how a company generates revenue. Almost all of the companies that already adopted the standard and provided ASC 606 disclosure, namely 448 out of the 451, disaggregated revenue streams to provide more granular disclosure of the revenue by product type, geography and revenue recognition method. In addition to the disaggregation of the revenue streams, many companies that have adopted the standard also modified segments disclosure to provide more granular information.

For example, prior to adoption, Tesla [TSLA] disaggregated revenue into four categories on the income statement. After adoption, in addition to the income statement disaggregation, Tesla disaggregated revenue by major source, segment and geography. Tesla disclosed seven major sources of revenue, two segments and four major geographic regions plus an ‘Other’ category for smaller markets.

Lastly, we were curious to see how companies disclosed information that compared old and new revenue standards. Although there is no explicit requirement which lines on the income statement and the balance sheet need to be reconciled, on average companies reconciled eleven lines, while the median was standing on seven. One company in particular, Marriott International [MAR] was standing reconciling full income statement, balance sheet and the statement of the cash flow.

Areas of Accounting Affected

To better understand the changes, we looked at the areas most affected by the new standard. Overall, about 60% of the companies disclosed the specific accounting areas impacted by the new rule.

The most common change, timing of revenue recognition, affected about 37% of the companies. Previously, many companies recorded revenue over a contract’s duration; now, with the new standard, many of the companies are able to recognize revenue sooner at a specific point in time (often at the beginning of the contract). This change is closely aligned with the overall positive impact on net income that we previously identified.

Other significant areas were capitalization of expenditures, including sales and commissions costs, and incremental costs required to fulfill the contract.

While it is interesting that many companies modified their business processes and controls to accommodate ASC 606, it is unsurprising, due to the complexity of the rule.

About 15% of the companies, 76 in total, implemented internal controls changes after adopting the rule.

Conclusion

In conclusion, as we expected, the standard turned out to be complex and, in some cases, confusing for both companies and investors. Analysts who want to understand how a company generates revenue need to continually monitor disclosures to learn about the changes. The SEC is also monitoring company disclosures. The agency will likely continue issuing comment letters, as about 10% of the companies have already received comment letters related to the implementation of the standard.

1. See “Kingsway Financial Services, Inc. [KFS]: Extensive SEC Comment Letter Conversation Identifies Accounting Errors” available at https://blog.auditanalytics.com/kingsway-financial-services-inc-kfs-extensive-sec-comment-letter-conversation-identifies-accounting-errors/↩