2020 was the year of the special purpose acquisition company (SPAC) initial public offerings (IPOs). The somewhat controversial method of going public represented more than half of all IPOs last year. The growth in popularity of SPACs has been evident for several years, with new highs in each of the past three years. However, the growth in 2020 is truly unprecedented; with 238 SPAC IPOs, 2020 had more than four times the previous high of 59 in 2019.

The amount raised by SPAC IPOs was even more astounding, nearly matching the amount raised by traditional IPOs. The more than $70 billion raised by SPACs in 2020 was nearly five times the previous high of $12 billion in 2019. On average, 2020 SPACs raised $300 million.

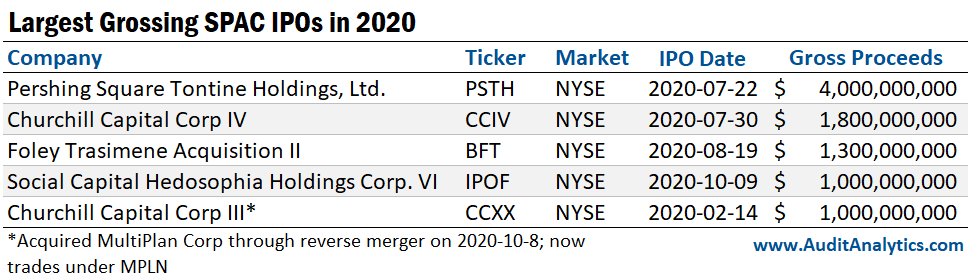

This was due, in part, to some extraordinarily large SPAC IPOs, with five raising $1 billion or more in 2020. Previously, two SPACs raised $900 million: Liberty Acquisition Holdings Virginia, Inc. in 2007 and Silver Run Acquisition Corp II in 2017. Liberty dissolved in 2010 without taking a company public. Silver Run acquired Alta Mesa Resources in 2018 before the company declared bankruptcy in 2019.

Of the five billion-dollar SPACs, only one has completed an acquisition: Churchill Capital Corp IV acquired MultiPlan as of October 8, 2020. Foley Trasimene Acquisition II has begun the process of acquiring Paysafe and expects to complete the deal in the first half of 2021. It is common for special purpose acquisition companies to take up to two years to complete an acquisition.

There are two main reasons SPACs are controversial. The first is that SPACs bypass the scrutiny of a traditional IPO. This can lead to issues being missed that may have been discovered through a traditional IPO process. One example of this is Nikola [NKLA], which went public through a deal with VectorIQ Acquisition Corp in June 2020. Hindenburg Research later issued a report that raised doubts about Nikola’s ability to deliver on the promise of the Nikola One truck.

The second reason contributing to controversy is that SPACs incentivize a deal, but not always the best deal. Sponsors typically make money by taking a private company public, but, as stated previously, SPACs can take up to two years to find an operating company to acquire. Prior to the transaction, funds from the IPO are held in escrow. Those funds are returned to investors less transaction fees if a transaction doesn’t occur.

Sponsors usually make money by acquiring a percentage of the newly formed public company. This incentivizes the sponsors of SPACs to ensure a transaction occurs, whether or not the company it is bringing public is a good candidate. According to Goldman Sachs, the average performance of SPACs have lagged both the S&P 500 and Russell 2000 as measured over three, six and twelve month ranges.

The prevalence of SPAC IPOs has steadily been on the rise since 2017, but the significant increase in 2020 was notable, for both the overall amount and the staggering proceeds raised. Given the controversy of SPAC IPOs and the uncertainty ahead in 2021, it will be interesting to see if this trend continues throughout this year and beyond. Though, it seems likely this year, as nearly a dozen SPACs have already gone public or plan to in the next week.

This analysis uses data from the IPO database, powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.