The Tax Cuts and Jobs Act, passed into law in December 2017, is going to significantly affect the amount of taxes on income paid by U.S. companies. The major provisions of the Act include a drop in corporate tax rate from 35% to 21%, a one-time 8% tax on illiquid assets and 15.5% on cash held overseas, and the establishment of a territorial tax system.

In the long run, the Act is expected to reduce tax bills for multinational companies and therefore, have a favorable effect on the bottom line. In the short term, however, the Act may have negative accounting consequences – primarily related to the impact of one-time transitional tax on foreign earnings and to the impact that change in the corporate tax rate will have on the value of deferred tax assets.

For some companies, this means billions of dollars in immediate write-downs. The key question, of course, is: who is going to be affected and by how much?

Under generally accepted accounting principles (GAAP), tax assets and liabilities are required to be re-measured during the period in which the new tax legislation is enacted. In some cases, if the impact is expected to be material, companies are also required to disclose estimated impact through 8-K filings.1

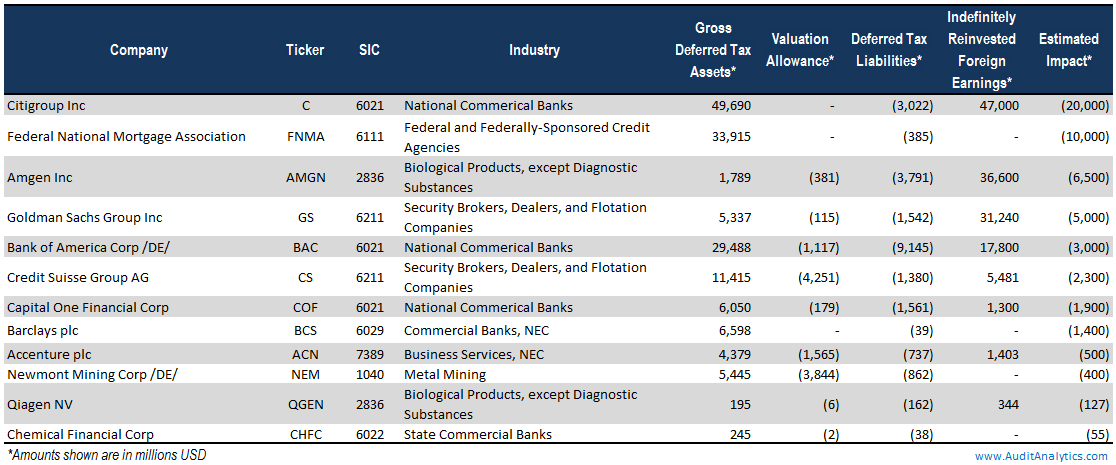

The analysis below is based on the disclosures provided in SEC filings and press-releases. So far, at least 36 companies made such a disclosure, reducing the net income by a total of at least $50 billion. Eight of these 36 companies disclosed write-downs that exceeded $1 billion. Interestingly, two out of 36 companies have large deferred tax liability positions, so the effect is expected to be positive.

Seven out of the eight companies having >$1 billion impact were financial companies, with Citigroup (C) topping the list with a staggering $20 billion tax impairment. This is not all that surprising, considering the large carry-over losses accumulated by the banking industry during the financial crisis.

Sure enough, the implications of the reduction in tax assets value can go beyond a simple accounting change. For example, Capital One Financial Corp (COF) indicated in its 8-K filing that the company will have to resubmit its capital plan. In connection with the resubmission, the company also had to cut its authorized repurchases to $1 billion.

Non-banking companies are also likely to see a near-term hit from the tax reform. One company that really stands out is Amgen (AMGN), which, according to the regulatory filing, is likely to incur a $6.5 billion tax charge:

The Company expects to incur Generally Accepted Accounting Principles (“GAAP”) net tax expense of between $6 billion and $6.5 billion, recorded as the nominal amount or the present value of such amount with the balance accreting over time. The net tax expense relates to the repatriation tax and the revaluation of net deferred tax liabilities. The Company will provide an update to its GAAP tax expense associated with the tax reform legislation in its fourth quarter/full-year 2017 earnings call on or about February 1, 2018. This charge will impact the Company’s previously provided 2017 GAAP earnings per share (“EPS”) and tax rate guidance. However, this charge has no impact on the Company’s previously provided non-GAAP guidance. Going forward, the Company does not expect an increase in its non-GAAP tax rates as a result of the legislation.

According to the same filing, the change will not affect the non-GAAP guidance previously provided by the company. In comparison to Citigroup and other financial companies, Amgen has a relatively low tax assets balance of about $1.8 billion. The company, however, ranked very high among companies with large indefinitely reinvested foreign earnings (IRFE), holding the 19th spot of the Russell 1000.2

But what about the companies that did not yet disclose the impact? A recent Market Watch article, using data provided by Audit Analytics, estimated that 15 companies with the largest tax assets balances will have to write over $74 billion, in aggregate.

It will be interesting to see how companies with large IRFE balances will be impacted. The top 50 companies (ranked by amount of IRFE), as listed in our “Indefinitely Reinvested Foreign Earnings: Balances Held by the Russell 1000: A 9-Year Snapshot” report, will certainly keep our focus this year.

For more information about the potential impacts of this Act or to receive a comprehensive list of companies that have already self-reported the Tax Cuts Act impact, please contact us at info@AuditAnalytics.com or call (508) 476- 7007.

1. In connection with the Tax Cuts Act, SEC recently issued SAB 118 update that outlines Tax Cuts Act 8-K filing requirements ↩

2. For more information, see “Indefinitely Reinvested Foreign Earnings: Balances Held by the Russell 1000: A 9-year Snapshot” report released by Audit Analytics in July 2017 ↩