The initiative to include key audit matters (KAMs) in auditor reports is a part of the global push for corporate and auditor transparency. In Canada, CAS 701 requires auditors to communicate KAMs in the auditor’s report. For companies listed on the Toronto Stock Exchange, the standard became effective for periods ending on or after December 15, 2020.

Following the implementation of the standard, Audit Analytics added the Canadian Key Audit Matters database to our product offerings in 2020. The database provides critical insights into this relatively new addition to the audit report.

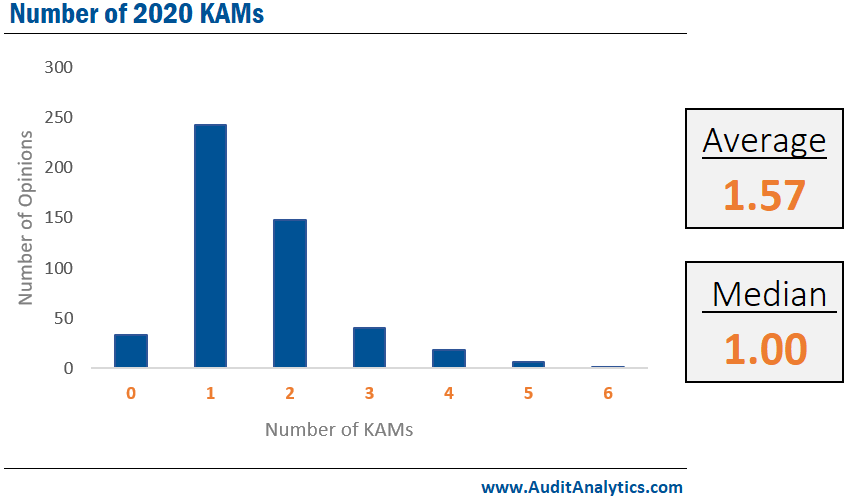

2020 KAM Trends

As with US critical audit matters (CAMs), KAMs are matters that the auditor determines are most significant during a financial statements audit. In the audit report, auditors are required to disclose why the matter was determined to be a KAM, how auditors addressed the matter in the audit, and reference related financial statement disclosures.

On average, Canadian auditors tended to identify between one and two KAMs in their auditor report in 2020. Similarly, in the US, audit reports averaged 1.67 CAMs.

Some Canadian audit reports contained up to six KAMs. In contrast, some audit reports identified no KAMs.

In 2020, the Big 4 audit firms hovered around this average. For example, EY averaged the highest with 1.7, and PwC averaged the lowest with 1.3.

Fixed assets was the most common topic cited as a KAM, appearing in 40% of all Canadian audit opinions. After that, the most common KAM topic was related to intangible assets, appearing in 22% of opinions.

In conclusion, KAMs provide valuable information about areas of the audit that carry more risk. Analyzing this information provides insight into the amount of risk and complexity of an audit. Additionally, KAMs communicate the auditor’s response to these significant issues. Using this insight, financial statement users and regulators can make more informed decisions, ultimately benefiting investors at large.

Interested in our content? Be sure to subscribe to receive our email notifications.