For the ninth year in a row, the Center for Audit Quality (CAQ) has released the Audit Committee Transparency Barometer. This report has provided investors with insights into the disclosures made by audit committees in proxy statements each year since 2014.

Compiled and published in partnership with Audit Analytics, the Barometer measures a year-over-year comparison of disclosures for S&P 500, S&P MidCap, and S&P SmallCap companies in certain key areas. These key areas include audit committee duties and composition, auditor evaluation/oversight, audit firm and lead partner selection, auditor compensation, cybersecurity, and new this year, ESG.

It begins by highlighting four new areas of focus in 2022. Specifically, the report highlights how audit committees execute areas of oversight responsibility, with the belief that there is room for improvement in transparency by the audit committee. These new focus points build on existing questions to better understand oversight responsibility.

In addition, two of the new questions tracked in fiscal 2022 related to ESG. They provided insight into ESG oversight and the audit committees having an ESG sustainability expert.

Auditor Tenure

Since 2018, auditor reports have been required to include auditor tenure, auditor independence, and audit quality. While many companies disclose audit firm tenure, very few mention how the audit committee considers the length of tenure during re-appointment.

71% of S&P companies discuss the length of time the auditor has been engaged. In comparison, only 9% disclose how the audit committee considers the length of tenure during re-appointment.

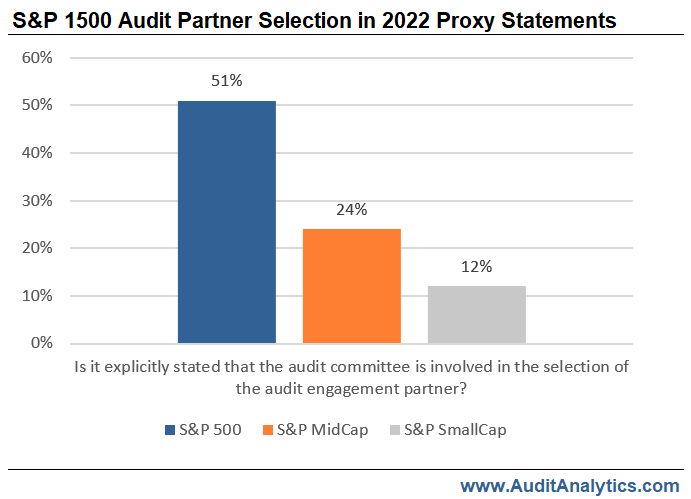

Audit Partner Selection

This year, the new question revolved around the involvement of the audit committee in the selection of the audit engagement partner. Results show 51% in S&P 500. The audit partner selection process is positively associated with audit quality, according to the 2021 Transparency Barometer.

“The oversight by the audit committee of the selection of the engagement partner is therefore critical to audit quality“.

Cybersecurity

The Audit Analytics 2021 Transparency Barometer blog predicted a continuous upward trend in cybersecurity disclosures as stakeholders’ interest in cybersecurity risk increases. This prediction held true. The 2022 barometer found 39% of proxy statements for S&P 500 companies disclose a cybersecurity expert on the board of directors. In comparison to 2021, with 34%.

The report found the audit committee is responsible for cybersecurity risk oversight for 54% of S&P 500 companies in 2022. In comparison, they were responsible for 46% in 2021. This shows a continuous upward trend in all areas of cybersecurity disclosures.

ESG

The CAQ began tracking ESG-related disclosures this current year. Equal to the percentage of audit committees having a cybersecurity expert, 39% of companies in the S&P 500 disclose having an ESG expert. Although significantly lower, the responsibility of ESG oversight is addressed by 18% of audit committees in the S&P 500. In contrast, 54% of audit committees addressing cybersecurity oversight.

It is highly likely that audit committees will continue to see a rise in ESG oversight, with data displaying that 453 companies in the S&P 500 disclosing climate-related information in their 10-Ks.

Audit Committee Disclosure and Practices

One key benefit of audit committee disclosures is quite simple. As referenced in the recent Barometer, “when audit committees report exerting strong oversight, they have higher audit quality“.

Investor protection relies heavily on audit committees through oversight of external auditors. In addition, audit committee disclosures on emerging risks such as cybersecurity and ESG are imperative to investors. Therefore, disclosures about the audit committee’s oversight responsibilities and how they execute these responsibilities promote trust among investors and supply them with valuable information.

The Kitchen Sink of the Board

The importance of clarity and transparency is crucial when it comes to creating proxy disclosures related to audit committee oversight. So much in fact, that researchers from the University of Tennessee-Knoxville and the Pamplin College of Business, Virginia Tech, have constructed a four-step method to assist those preparing proxies. This method will help them revamp and revise their disclosures. The report titled Audit Committee: The Kitchen Sink of the Board, How Audit Committees Can Manage Their Evolving Responsibilities and Polish Their Proxy Disclosures, shows us how proxies can have a fresh enhanced look.

In conclusion, over the course of nine years, we have witnessed long-term upward disclosure trends across most questions. We will continue to monitor these trends, and report on new findings. This year, more so than in previous years, the CAQ encouraged audit committees to be fully transparent, improve disclosures, and enhance the clarity and consistency of the oversight work they perform.

Interested in our content? Be sure to subscribe to receive our email notifications.