A wave of change appears to be forming in the arcane area of pension accounting.

About a year ago, AT&T made a change to the way it calculates the present value of future pension obligations. Typically, companies used the “weighted-average” method to determine a discount rate to use in the present value calculation. In its Fiscal 2014 10-K, AT&T disclosed that it was switching to the “spot-rate” method. Since the AT&T adoption, at least 451 more companies have made the change to the spot-rate.

As we previously predicted, AT&T does indeed appear to have been a bellwether on this issue. The SEC, back in the spring, sent a comment letter to AT&T requesting more information about the company’s change. Subsequently, the regulator issued a clarification in regard to the adoption of the spot-rate method, indicating at the AICPA-SEC/PCAOB conference that the SEC would not object to the use of this method. The Big 4 firms (e.g., Deloitte and EY) then published memoranda documenting the change, and companies appeared to take head. Mead Johnson, for example, referenced the SEC’s comments in their most recent 10-K.

The SEC staff stated that it would not object to companies’ use of an alternative approach that focuses on measuring the service cost and interest cost components of net periodic benefit cost by using individual spot rates derived from a high-quality corporate bond yield curve and matched with separate cash flows for each future year instead of a single weighted-average discount rate approach. Futher, the SEC staff stated it would not object to companies treating the change in approach as a change in estimate.

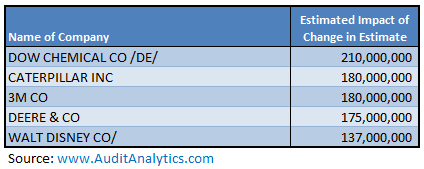

As General Dynamics disclosed in its 10-K, the spot-rate “provides a more precise measurement of service and interest costs.” But the change can also improve results, at least in the short term. AT&T reported that the adoption of the spot-rate method decreased service and interest costs related to the defined-benefit plan by $740 million for fiscal 2015. Five companies expect the change to reduce their service and interest costs by over $100 million, providing a not insignificant boost to earnings.2

Since these changes are generally being treated as changes to an accounting estimate, the adoption is recognized prospectively. That is, prior financials are not represented as if the spot rate had been used historically. Comparability between financial years will be affected for companies that make this change.

With more companies adopting the spot-rate, the method may become the norm. As of January 1st, at least 32 companies have disclosed the adoption. We expect to see many more to follow.

1. Evaluation includes 10-K and 10-Q filings through February 18, 2016. Excludes subsidiaries.↩

2. Most companies disclosed the estimated impact of the change for Fiscal 2016, so these figures are forward-looking.↩