Last week on February 6, in its Fiscal 2016 10-K, eBay (EBAY) disclosed a material weakness in its internal controls over financial reporting (“ICFR“). The deficiency related to a failure to properly apply tax accounting and affected the Deferred Tax Asset and Income Tax Benefit accounts.

In reviewing the accounting for certain transactions completed in December 2016 as part of the realignment of our legal structure, our management identified a deficiency in the effectiveness of a control intended to properly document and review relevant facts and apply the appropriate tax accounting under accounting standards generally accepted in the United States of America, which impacted the Deferred tax asset and Income tax benefit accounts and related disclosures.

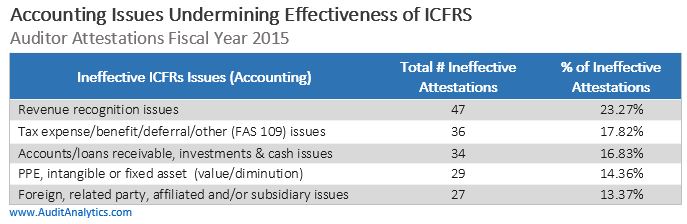

As we reported in a recent study, tax deficiencies were the second most common accounting issue to cause ineffective ICFR reports. Among companies that are required to have an auditor inspect their internal controls, 36 reports (17.82% of all ineffective attestations) cited tax accounting as one of the reasons for ineffectiveness.

Interestingly, there was very little market reaction to eBay’s disclosure. One possible explanation is that the control deficiency affected only a relatively narrow area of accounting. A clear remediation plan discussed in Item 9A might also have reduced the impact of the ineffective controls on eBay’s stock price.

We normally think about accounting-related weaknesses in the context of financial restatements. Yet, Auditing Standard No. 5 states that “the severity of a deficiency does not depend on whether a misstatement actually has occurred but rather on whether there is a reasonable possibility that the company’s controls will fail to prevent or detect a misstatement.” (par. 64) EBay did not identify any significant errors, but did note that the deficiency resulted in an adjustment during the period end close process.

Could the opposite also be true? In other words, would an accounting error always trigger non-effective attestation report? Well, not necessarily. In February 2015, eBay had to adjust previously reported Q4 2014 and full year earnings to correct an $88 million tax error.

In April 2015, the SEC issued a comment letter to eBay, requesting additional information about the materiality of the error and its impact on internal controls over financial reporting. In response, eBay confirmed that the error was identified by the auditor during the period-end closing process and that the error was caused by an immaterial control deficiency:

…eBay’s independent auditors identified a misapplication of the accounting literature relevant to the release of the valuation allowance on capital loss carryovers resulting in an audit adjustment. At that time, eBay concluded that the initial measurement of the transaction should be changed, and an adjustment was recorded by eBay and reflected on eBay’s Form 10-K for the fiscal year ended December 31, 2014, which was filed on February 6, 2015. eBay concluded that the adjustment was neither quantitatively nor qualitatively material but nevertheless filed an additional Form 8-K in connection with the filing of the Form 10-K to provide a clear explanation of the difference to investors.

As a result of this change to eBay’s reported results for the period ended December 31, 2014, eBay concluded that a control deficiency existed.

After additional analysis, eBay concluded that the deficiency did not rise to the level of a material weakness, and, therefore, its Internal Controls over Financial Reporting were effective.

The amount of adjustment together with the amount of the maximum exposure relative to eBay’s earnings initially reported on January 21, 2015 and those reported on its Form 10-K filed on February 6, 2015 was substantially less than its total quantitative materiality threshold. eBay therefore concluded that this matter did not quantitatively rise to the level of a material weakness. eBay also considered other indicators of a material weakness in accordance with Public Accounting Oversight Board Bylaws and Rules – Standards – AS5 and noted that the indicators were not present or not applicable due to the immaterial nature of the adjustment. However, eBay communicated the adjustment to its Audit Committee of the Board of Directors on February 4, 2015.

In response to a follow up letter from the SEC, eBay provided additional details about the specific controls that failed in this circumstance, further described their planned remediation efforts, and concluded that no additional disclosure would be required since expected improvements to controls are unlikely to have a material impact on internal controls.

Response: Our standard practice is to remediate all identified control deficiencies, whether or not determined to be a material weakness. As a result of the identified design gap, we have assessed and determined that the valuation allowance control as it existed in the fourth quarter of 2014 should be amended to include formalizing the tax accounting analysis related to intra period allocation technical accounting considerations for the release of valuation allowances.

For the reasons noted above, we do not believe that the proposed change to our valuation allowance control will have, or is reasonably likely to have, a material effect on our ICFR. As such, we determined that no disclosure related to a change in our ICFR was necessary to Item 9A of our Form 10-K for the period ended December 31, 2014. We subsequently updated our control activity description for this control but for the reasons stated above we did not believe a disclosure related to a change in our ICFR was necessary in Item 4 of our Form 10-Q for the period ended March 31, 2015.

Based on the analysis provided by eBay, the proposed disclosure (or rather the lack of thereof) is aligned with regulatory requirements. The AS 5 requirement to disclose control issues extends only to deficiencies that rise to the level of a material weakness; and only changes in internal controls that are likely to have a material impact on ICFR need to be disclosed in Item 9A.

The remediation efforts needed to rectify material weakness identified in February 2017, appear to be more significant:

Remediation Plan. Management has begun implementing a remediation plan to address the control deficiency that led to the material weakness. The remediation plan includes the following:

• Implementing specific review procedures, including the added involvement of our chief tax officer in the review of tax accounting, designed to enhance our income tax control; and

• Strengthening our income tax control with improved documentation standards, technical oversight and training

Interestingly, we saw a very similar scenario last September, when Walmart disclosed a material weakness in lease accounting. Similar to eBay, in 2014, Walmart discovered a control deficiency and recorded an immaterial error correction. Walmart also received a subsequent SEC comment letter with requesting the retailer to provide a SAB 99 materiality analysis and clarify the impact of the errors on ICFR. Subsequently, in September 2016, Walmart identified a material weakness in ICFR related to lease accounting.

To summarize, eBay’s tax control deficiencies appear to be unrelated to each other. In 2014, the deficiency was related to controls over valuation allowance, while the 2017 weakness is related to intercompany accounting. None of the errors affected previously filed financial statements. Still, adjustments were required in both cases. Just another example of why investors should pay close attention to even immaterial adjustments and control deficiencies.

EBay Reports Material Weakness: Second Control Deficiency in Three Years

Last week on February 6, in its Fiscal 2016 10-K, eBay (EBAY) disclosed a material weakness in its internal controls over financial reporting (“ICFR“). The deficiency related to a failure to properly apply tax accounting and affected the Deferred Tax Asset and Income Tax Benefit accounts.

As we reported in a recent study, tax deficiencies were the second most common accounting issue to cause ineffective ICFR reports. Among companies that are required to have an auditor inspect their internal controls, 36 reports (17.82% of all ineffective attestations) cited tax accounting as one of the reasons for ineffectiveness.

Interestingly, there was very little market reaction to eBay’s disclosure. One possible explanation is that the control deficiency affected only a relatively narrow area of accounting. A clear remediation plan discussed in Item 9A might also have reduced the impact of the ineffective controls on eBay’s stock price.

We normally think about accounting-related weaknesses in the context of financial restatements. Yet, Auditing Standard No. 5 states that “the severity of a deficiency does not depend on whether a misstatement actually has occurred but rather on whether there is a reasonable possibility that the company’s controls will fail to prevent or detect a misstatement.” (par. 64) EBay did not identify any significant errors, but did note that the deficiency resulted in an adjustment during the period end close process.

Could the opposite also be true? In other words, would an accounting error always trigger non-effective attestation report? Well, not necessarily. In February 2015, eBay had to adjust previously reported Q4 2014 and full year earnings to correct an $88 million tax error.

In April 2015, the SEC issued a comment letter to eBay, requesting additional information about the materiality of the error and its impact on internal controls over financial reporting. In response, eBay confirmed that the error was identified by the auditor during the period-end closing process and that the error was caused by an immaterial control deficiency:

After additional analysis, eBay concluded that the deficiency did not rise to the level of a material weakness, and, therefore, its Internal Controls over Financial Reporting were effective.

In response to a follow up letter from the SEC, eBay provided additional details about the specific controls that failed in this circumstance, further described their planned remediation efforts, and concluded that no additional disclosure would be required since expected improvements to controls are unlikely to have a material impact on internal controls.

Based on the analysis provided by eBay, the proposed disclosure (or rather the lack of thereof) is aligned with regulatory requirements. The AS 5 requirement to disclose control issues extends only to deficiencies that rise to the level of a material weakness; and only changes in internal controls that are likely to have a material impact on ICFR need to be disclosed in Item 9A.

The remediation efforts needed to rectify material weakness identified in February 2017, appear to be more significant:

Interestingly, we saw a very similar scenario last September, when Walmart disclosed a material weakness in lease accounting. Similar to eBay, in 2014, Walmart discovered a control deficiency and recorded an immaterial error correction. Walmart also received a subsequent SEC comment letter with requesting the retailer to provide a SAB 99 materiality analysis and clarify the impact of the errors on ICFR. Subsequently, in September 2016, Walmart identified a material weakness in ICFR related to lease accounting.

To summarize, eBay’s tax control deficiencies appear to be unrelated to each other. In 2014, the deficiency was related to controls over valuation allowance, while the 2017 weakness is related to intercompany accounting. None of the errors affected previously filed financial statements. Still, adjustments were required in both cases. Just another example of why investors should pay close attention to even immaterial adjustments and control deficiencies.