Regulation G, adopted by the SEC in 2003, established a regulatory framework that companies must follow to present metrics that are not calculated in accordance with GAAP. Regulation G defines a non-GAAP metric as a numerical measure that excludes amounts included in the most comparable measure calculated under GAAP. Proponents of non-GAAP disclosure argue that non-GAAP metrics improve transparency and allow better communication of information through the eyes of management.

Audit Analytics collects non-GAAP data from 8-K Items 2.02 (earnings releases) on a quarterly basis, which highlights notable variance between quarters. For this reason, our recently released report, Long-Term Trends in Non-GAAP Disclosures: A Three-Year Overview, looks at non-GAAP trends on an annual basis to eliminate any statistical noise from shorter, quarterly observations.

To better understand the explosive growth of non-GAAP usage, Audit Analytics looked at the use of non-GAAP metrics at three different points in time for the S&P 500: 1996, 2006, and 2016. To make the results comparable, we examined the S&P 500 companies that used non-GAAP metrics in both 1996 and 2016. The analysis was performed using data from 8-K Item 2.02 filings, when available, and 10-K filings in other cases.

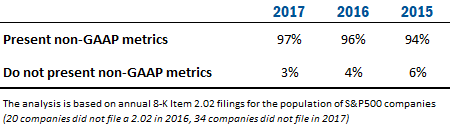

In 2017, 97% of the S&P 500 used at least one non-GAAP metric in their financial statement.

Non-GAAP metrics are often criticized because, for the most part, the non-GAAP numbers eliminate significant expenses and charges and therefore may disguise deteriorating financial performance. When metrics are presented using “adjusted” or “excluded” components, it can be difficult to discern what numbers reflect true financial position.

This report focuses on these five main categories of non-GAAP metrics:

- Income-related (including Operating Income and other Income Metrics)

- Earnings-per-share (EPS) related

- Cash-Flow related (such as free cash flow)

- EBITDA (including Adjusted EBITDA)

- Funds From Operations (including Adjusted FFO)

To request a full copy of the report, or for more information on non-GAAP disclosures, e-mail info@auditanalytics.com or call 508-476-7007.