Audit Analytics released our latest report, Corporate Implementation of SEC’s Compliance & Disclosure Interpretations Regarding Non-GAAP Financial Measures, at this year’s annual AICPA conference on current SEC and PCAOB developments, held in Washington, D.C.

The SEC recently provided an update to the Compliance & Disclosure Interpretations (“C&DIs”) regarding Business Combination Transactions (Section 101), which explained the conditions that must be observed to ensure that financial measures included in forecasts given to financial advisors during a business combination transaction would not constitute a non-GAAP measure.

Our report focuses on the analysis of non-GAAP usage, and was expanded from last year’s report to include the population under review to the Russell 1000. Let’s check out the progress companies have made in the past year.

464 companies (95%) of the S&P 500 disclosed a non-GAAP measurement, a decrease of 11 companies from the year before. A large portion of the remaining Russell 1000 companies also presented non-GAAP measures.

A more in-depth analysis shows that companies reacted to the SEC guidance by no longer disclosing certain types of non-GAAP metrics and/or changing the way they disclosed non-GAAP financial measures.

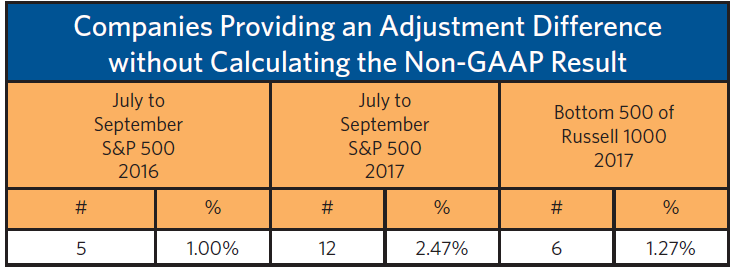

The non-Non-GAAP Presentation

As noted briefly in last year’s report, some companies provided information that does not constitute a non-GAAP financial measure, but is of interest because the practice does present information beyond that given by a typical GAAP presentation. Some companies present a reconciling table that gives the difference a non-GAAP metric would manifest without presenting a non-GAAP measure itself. Regulation G defines a non-GAAP metric as a numerical measure that excludes amounts that are included in the most comparable GAAP measure. Therefore, the method adopted by these companies would not fall under the purview of Regulation G. Nevertheless, the use of this unique practice has increased and is noteworthy.  In 2016, five S&P 500 companies chose to disclose information in a reconciling table in this manner. The use of this approach more than doubled in 2017. In addition, six companies in the Bottom 500 Russell 1000 population present differences to a GAAP metric without showing the resulting non-GAAP metric.

In 2016, five S&P 500 companies chose to disclose information in a reconciling table in this manner. The use of this approach more than doubled in 2017. In addition, six companies in the Bottom 500 Russell 1000 population present differences to a GAAP metric without showing the resulting non-GAAP metric.

In some of the cases, the new presentation came after SEC comment letters that disallowed certain non-GAAP adjustments. For example, Activision Blizzard, Inc. agreed to modify its net effect from deferral of net revenues and related cost of sales metric to comply with Regulation G and replaced the metric with the alternative presentation.

While we believe excluding the change in deferred revenues and related cost of sales with respect to certain of the company’s online-enabled games in our supplemental non-GAAP disclosure was appropriate and in compliance with Regulation G as well as useful to our investors, we acknowledge the Staff’s comment. We will review and reflect the guidance included in the updated C&DI’s when preparing our next earnings release and periodic report.

There is nothing wrong with presenting information that would be potentially useful to investors in a form that adds to the GAAP presentation, however, this type of presentation deserves discussion because the approach appears to be gaining ground.

Although it is clear that registrants have modified and/or improved their disclosures in response to the C&DIs, it remains a focus of the SEC. Division Chief Accountant, Mark Kronforst, indicated at the conference that the volume of recent comments on non-GAAP measures has dropped to pre-2016 levels, but the SEC staff will continue to closely monitor their use and issue comments

To request a copy of the full report or for more information, please contact us at info@auditanalytics.com or call (508) 476-7007.

Non-GAAP Reporting One Year After New SEC Guidance

Audit Analytics released our latest report, Corporate Implementation of SEC’s Compliance & Disclosure Interpretations Regarding Non-GAAP Financial Measures, at this year’s annual AICPA conference on current SEC and PCAOB developments, held in Washington, D.C.

The SEC recently provided an update to the Compliance & Disclosure Interpretations (“C&DIs”) regarding Business Combination Transactions (Section 101), which explained the conditions that must be observed to ensure that financial measures included in forecasts given to financial advisors during a business combination transaction would not constitute a non-GAAP measure.

Our report focuses on the analysis of non-GAAP usage, and was expanded from last year’s report to include the population under review to the Russell 1000. Let’s check out the progress companies have made in the past year.

464 companies (95%) of the S&P 500 disclosed a non-GAAP measurement, a decrease of 11 companies from the year before. A large portion of the remaining Russell 1000 companies also presented non-GAAP measures.

A more in-depth analysis shows that companies reacted to the SEC guidance by no longer disclosing certain types of non-GAAP metrics and/or changing the way they disclosed non-GAAP financial measures.

The non-Non-GAAP Presentation In 2016, five S&P 500 companies chose to disclose information in a reconciling table in this manner. The use of this approach more than doubled in 2017. In addition, six companies in the Bottom 500 Russell 1000 population present differences to a GAAP metric without showing the resulting non-GAAP metric.

In 2016, five S&P 500 companies chose to disclose information in a reconciling table in this manner. The use of this approach more than doubled in 2017. In addition, six companies in the Bottom 500 Russell 1000 population present differences to a GAAP metric without showing the resulting non-GAAP metric.

As noted briefly in last year’s report, some companies provided information that does not constitute a non-GAAP financial measure, but is of interest because the practice does present information beyond that given by a typical GAAP presentation. Some companies present a reconciling table that gives the difference a non-GAAP metric would manifest without presenting a non-GAAP measure itself. Regulation G defines a non-GAAP metric as a numerical measure that excludes amounts that are included in the most comparable GAAP measure. Therefore, the method adopted by these companies would not fall under the purview of Regulation G. Nevertheless, the use of this unique practice has increased and is noteworthy.

In some of the cases, the new presentation came after SEC comment letters that disallowed certain non-GAAP adjustments. For example, Activision Blizzard, Inc. agreed to modify its net effect from deferral of net revenues and related cost of sales metric to comply with Regulation G and replaced the metric with the alternative presentation.

There is nothing wrong with presenting information that would be potentially useful to investors in a form that adds to the GAAP presentation, however, this type of presentation deserves discussion because the approach appears to be gaining ground.

Although it is clear that registrants have modified and/or improved their disclosures in response to the C&DIs, it remains a focus of the SEC. Division Chief Accountant, Mark Kronforst, indicated at the conference that the volume of recent comments on non-GAAP measures has dropped to pre-2016 levels, but the SEC staff will continue to closely monitor their use and issue comments

To request a copy of the full report or for more information, please contact us at info@auditanalytics.com or call (508) 476-7007.