Pledging securities, when a beneficial owner pledges their company shares as collateral, poses significant risks to corporate governance and share price. This risk is heightened when securities related to a special purpose acquisition company (SPAC) investment are pledged, due to additional risks and uncertainties associated with SPAC transactions.

SPACs are formed to raise capital via an IPO for the purpose of acquiring an existing privately held company. These shell entities typically offer a faster route to the public market, but SPACs carry several unique risks for investors: the SPAC’s ability to acquire a private entity and an acquired entity’s sustainability in the public market. Potential investors do not have the opportunity to review the more extensive financial information available for a more traditional IPO because SPACs lack a business operation as of the IPO date. By entering the public market and essentially acquiring business operations via a merger, acquired companies bypass some of the regulatory scrutiny upon initial market entry.

As such, confidence in major backers and entity leadership to address these risks and ensure the merged entity’s compliance greatly influence if and how much stakeholders invest in a SPAC.

As we have discussed, pledged securities present risks to corporate governance and share price. These are compounded for SPAC investors relying on the credibility SPAC sponsors and beneficial owners lend to already risky ventures. When these key investors pledge their ownership in a SPAC in exchange for financing, the risk associated with the SPAC investment is transferred to a financial institution.

While there is always a risk for securities to be sold once pledged as collateral, the risk is heightened for securities pledged from a SPAC investment. SPAC sponsors usually make money by acquiring a percentage of the newly formed public company through the beneficial ownership of company shares. Pledged SPAC shares carry an increased risk of being exposed as unmet margin calls, as SPAC investments are often subject to share price volatility and are not guaranteed to be successful in the public market.

If pledged shares for a SPAC investment are exposed as unmet margin calls, it could lead to a change in ownership and control, impacting sustainability and future prospects as a public company, regardless of operational success.

Despite associated risks, pledging securities for SPACs can be used as part of a hedging or monetization strategy to protect key investors from “worse case scenarios” – situations in which the optimistic future-looking projects or production goals fail to come to fruition and sets a floor for the losses an influential figure might accrue on a given SPAC investment.

This is particularly ironic, as the involvement of these “fair-weather” leaders was likely a significant factor in most shareholders decision to initially invest in the shell corporation.

The perils this situation can have for main street investors can be seen in the recent headlines involving insurance company Clover Health Investment Corp. The company went public in January 2021 through Social Capital Hedosophia III, one of many SPACs backed by venture capitalist Chamath Palihapitiya.

Lauded by many as the “SPAC King”, the former Facebook executive has been an outspoken advocate of the opportunity SPACs provide to main street investors. The recent focus on Palihapitiya involves a report issued by Hindenburg Research, claiming Clover Health “misled investors about critical aspects of Clover’s business in the run-up to the company’s SPAC go-public transaction”, as well as failed to disclose an active investigation by the Department of Justice regarding a variety of questionable business practices.

In a statement filed with the SEC in response to this report, Clover Health executives Vivek Garipalli and Andrew Toy confirmed Palihapitiya’s knowledge of the ongoing DOJ investigation at the time of the de-SPAC and iterated the company’s stance that, “the fact of DOJ’s request for information was not material and was not required to be specifically disclosed in [the Company’s] SEC filings.”

Following the release of the Hindenburg report, the value of the company’s stock dropped 14%. It is not surprising that reports of corporate investigation affected market confidence in the entity. However, it is particularly notable that the company confirmed Palihapitiya’s knowledge of the situation; this could signal a lack of transparency, undermining the confidence in Palihapitiya that potentially led main street investors to acquire entity shares.

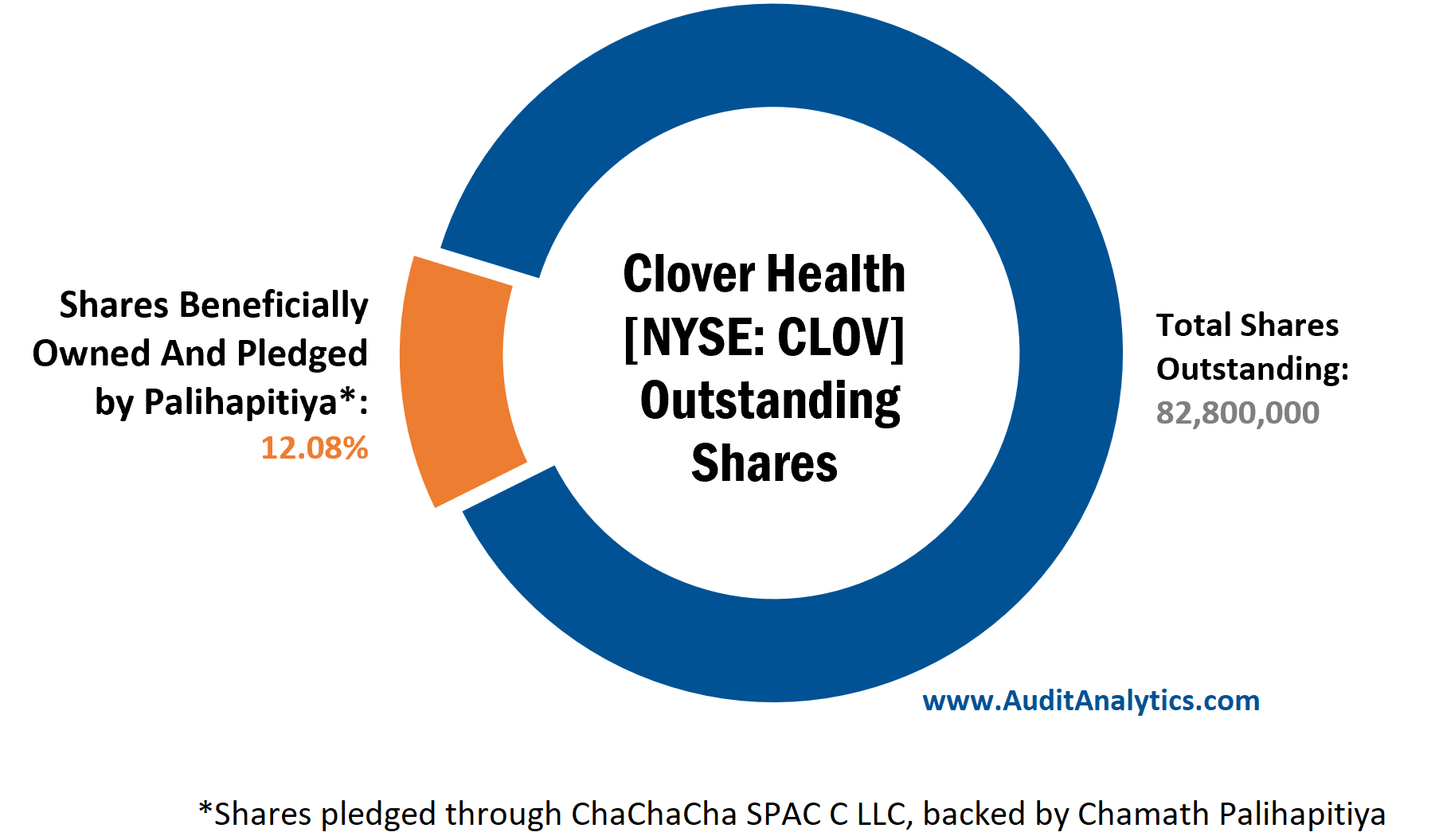

Interestingly, all 10,000,000 of Clover Health shares beneficially owned by Palihapitiya – through ChaChaCha SPAC C LLC – have been pledged to Credit Suisse AG, New York Branch as collateral with respect to a loan agreement.

For a newly public company like Clover Health, appearing to be less-than-forthcoming about sensitive, if not material, information at the time of the merger could have a profoundly detrimental effect on stock price. This is augmented by the disclosure that the SEC launched an investigation following the Hindenburg Research article. A decrease in stock price heightens the risk for pledged shares to be sold by the institution holding them as collateral, an action that risks further depressing the stock price.

Clover Health is not the only company whose shares Palihapitiya has pledged. Palihapitiya has pledged 100% of his shares that he directly beneficially owns in Virgin Galactic Holdings [NYSE: SPCE], another company taken public last year by a Palihapitiya-backed SPAC. This amounts to 2.95% of Virgin Galactic’s total shares outstanding – worth roughly $400 million. In the event of a default under the margin loan agreement for which the shares have been pledged as collateral, the holding party may foreclose upon any and all shares pledged and are entitled to seek recourse.

If a significant amount of pledged securities for a SPAC-acquired company are subject to a sudden forced sale, it carries the risk of negative impacts on the stock price, company operations, and overall financial health, even before the company becomes established and has an opportunity to be successful in the public market.

Regardless of risks associated with SPACs, it is likely there will continue to be an increase in companies going public via this non-traditional method, based on current trends in SPAC activity. With this explosion in activity and substantial proceeds raised, other aspects of these deals, such as sponsors pledging their securities, risk being overlooked by investors.

Notably, in a deal announced in early 2021, fintech company SoFi will be going public using one of Palihapitiya’s SPACs, while Social Capital Hedosophia Holdings Corp IV (IPOD) and VI (IPOF) are currently seeking target companies to take public. If he handles his ownership in these the same way as Virgin Galactic and Clover Health, investors should carefully evaluate what Palihapitiya’s future involvement, or lack thereof, means for long-term corporate stability.

Currently, the risk pledged securities in SPACs pose to investors is largely limited to a few registrants like Clover Health and Virgin Galactic. IPOs are subject to a lock-up period in which insiders are prevented from selling, disposing of, or pledging shares of common stock or securities and while the length is often between 90-180 days, the lockup phase for SPACs is often significantly longer, spanning up to 12 months.

Many SPAC sponsors are still subject to lock-up restrictions, but as these periods end, it is likely the frequency of pledging securities and heightened risks these agreements present to main street investors will increase.

This analysis uses data from the Pledged Securities database and the IPO database, both powered by Audit Analytics.

For more information about Audit Analytics or this analysis, please contact us.

Interested in our content? Be sure to subscribe to receive our email notifications.