Audit Analytics was invited to present at a recent meeting of the Financial Accounting Standards Advisory Council (FASAC), on March 17th at the FASB offices in Norwalk, CT. CEO and Founder, Mark Cheffers – along with Olga Usvyatsky, VP of Research, and John Pakaluk, Product Manager – offered some thoughts on reporting quality indicators, with the perspective of analyzing a wide swath of reporting disclosures across the SEC landscape.

Topics included the latest trends in financial restatement disclosures, themes in comment letters, non-GAAP disclosures, and more. One unique issue that was addressed was a recurring pattern noted in changes to accounting figures, whether they be restatements, adjustments, or changes in estimates: they tend predominantly to reflect an underlying bias of optimism. That is, restatements and error-correcting adjustments are much more likely to correct overstatements of income; while changes in accounting estimates – recorded prospectively – are more likely to increase income in the period the change is made.

In this post, we present a small selection of slides from the presentation. The whole presentation can be downloaded here.

I. Restatements

Our annual Restatement Report will be released soon. The presentation includes a sneak peek of the findings from the most recent report, which covers restatement disclosures made from 2001 through 2014.

- The total number of restatements has remained flat since 2009.

- There were 831 total restatements in 2014, compared to 867 in 2013 and 851 in 2012.

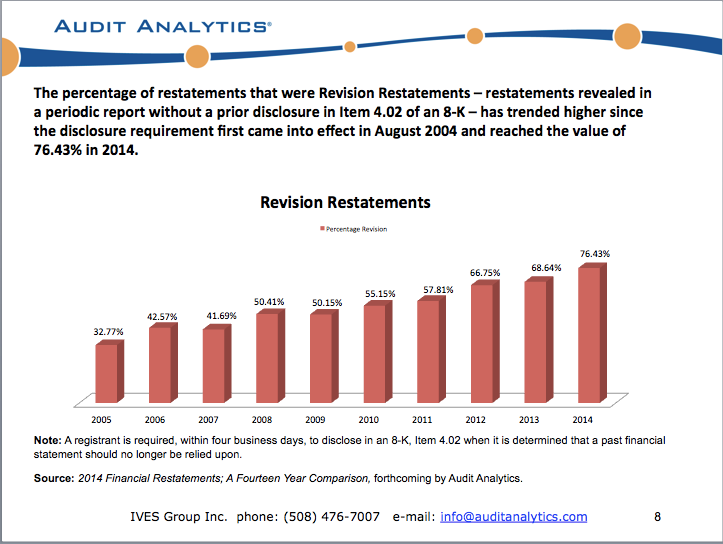

- The trend towards revision restatements continues even higher in 2014.

- Over 76% of all restatements filed during the year were so-called “revision” restatements, i.e., those that do not require an Item 4.02 8-K.

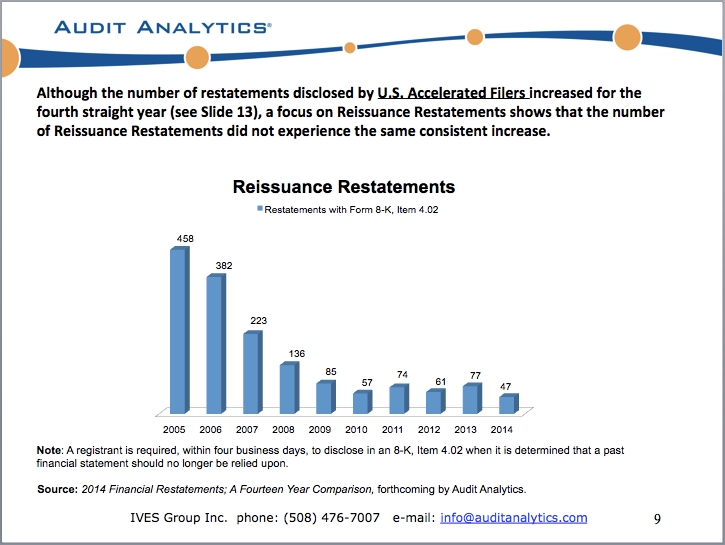

- Conversely, the number of Item 4.02 8-K Reissuance restatements continues to decrease.

- Accelerated filers disclosed only 47 reissuance restatements during the year.

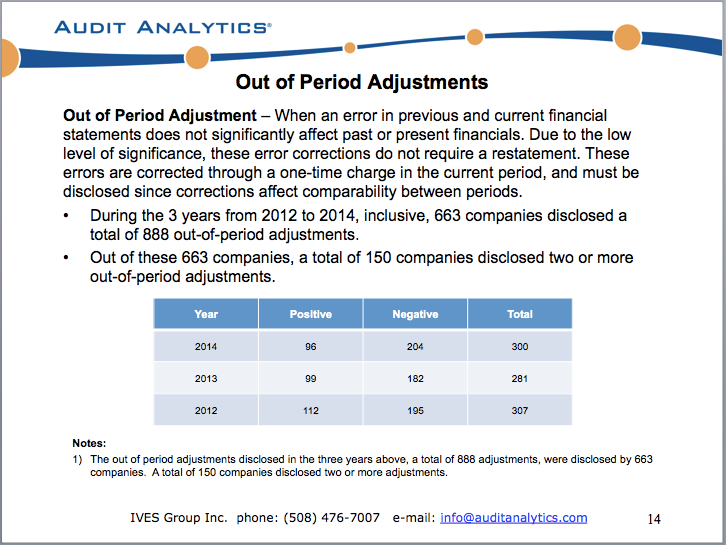

II. Out of Period Adjustments & Changes in Estimates

Two of our newest databases were the subject of some debate and conversation. In the presentation, we noted that Out of Period Adjustments – “immaterial” error corrections – and Changes in Accounting Estimates both presented an underlying pattern that suggests there might be more going on than meets the eye. Out of Period Adjustments are more likely to have a negative impact on income, and Changes in Estimates are more likely to have a positive impact on income.

- As noted above, Changes in Estimates that have a positive impact on income outnumber ones with a negative impact in every year under analysis.

- The bias towards positive adjustments goes as high as 62%.

- Out of Period Adjustments with a negative impact outnumbered those with a positive impact in the three years analyzed.

- The bias towards negative adjustments hit 68% in 2014.

Changes in Accounting Estimates and Out of Period Adjustments are two new databases available from Audit Analytics as part of a subscription to the Accounting + Oversight Module. For additional information on this module or any of the Audit Analytics data sets mentioned in this blog, please e-mail us at info@auditanalytics.com or call 508-476-7007.