In a post from May, we provided an analysis of audit fees for Canadian companies whose filings are available through the SEDAR system. In 2007, we noted, non-audit fees were 29% of the total fees paid by all Canadian issuers. Over the next six years, non-audit fees dropped to about 23% of total fees in 2013.1

It is not always clear, however, where the line is drawn between audit fees and some non-audit fees. Are distinctions consistently applied across the board? It’s hard to say. In our experience we have seen some US companies include things like the quarterly reviews in audit fees, while others include them in audit-related.

For Canadian companies, the compensation of the external auditor is disclosed pursuant to the Multilateral Instrument 52-110 on Audit Committees, which describes in Item 9 the following categories of fees that are to be disclosed: (1) Audit Fees, (2) Audit-Related Fees, (3) Tax Fees, and (4) All Other Fees.

According to the Multilateral Instrument, “Audit Fees” should include the aggregate fees billed by the issuer’s external auditor in each of the last two fiscal years for audit services. “Audit-related” fees category should include the aggregate fees billed for assurance and related services that are reasonably related to the performance of the audit or review of the issuer’s financial statements and are not included in “Audit Fees”. All Other Fees are defined as all the fees that are not included in “Audit”, “Audit-Related” or “tax” fees.

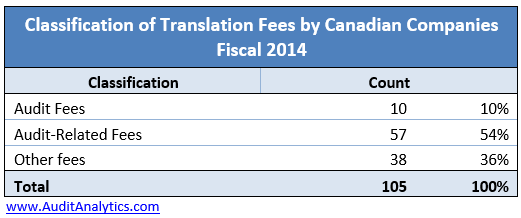

The table below shows a breakdown of where Canadian companies classified translation costs according to the one of the four categories listed in the Multinational Instrument.

In 2014, about 4% of the nearly 3,000 Canadian filers tracked by Audit Analytics disclosed information about costs related to the translation of their financials. As evident from the table above, there is a clear diversity in practice: more than half of these companies (57 issuers) treated translation costs as audit-related, 36% included the costs in the “Other” category, and 10% included translation costs in with audit fees.

In practice, however, the diversity may not be as significant as it appears here. This is a small sample of only 105 companies out of 2,773. Further, there was some uncertainty even among these few companies that did disclose information about translation fees. In most cases, these disclosures were not sufficient to determine whether the translation was related to required regulatory filings – Quebec typically requires translation to French – or translation services of some other documents to languages other than French

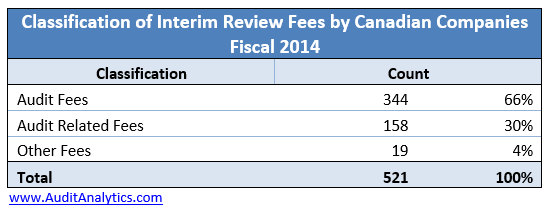

In the table below, we looked at another category of costs routinely incurred by Canadian public companies, namely, costs to review interim financial statements.

As expected, costs associated with reviews of quarterly financial statements were mostly classified as audit fees: 66% of companies that discussed interim reviews in the fees section classified those expenses as Audit Fees, while a further 30% considered these costs Audit-related. This corresponds to what we have seen from US public companies. (Our 2015 Audit Fees report is now available.)

Audit Analytics, the leader in US auditor intelligence, also tracks Canadian auditors and audit fees. We are pleased to announce the release of a database of European Union auditors and audit fees. For more information, please contact us.

1. For the purposes of this analysis, non-audit fees include audit-related, tax, and other fees.↩