It’s four o’clock on a Friday afternoon. The workweek is almost over. Many cubicle dwellers have already slipped out for an early weekend happy hour, followed by a couple days of R&R.

Anyway, that’s the way it is for you and me, maybe, but not for an overworked CFO, especially one with a pending press release full of bad news. When it comes to bad news, Friday afternoon might be the busiest time of all. Press releases are more art than science, and the worse the news, the more…artistic the phrasing.

How do companies bury the bad news? One way is to disseminate the information in small bits, each of which is not so bad by itself, and appears even less negative when mixed in with positive news. A tried-and-true method of dissembling is the use of non-GAAP measures, especially to play down unwelcome “one-time costs”. But one thing common to companies, politicians, and all who play the press, is the correct timing.

Footnoted.com recently blogged about the Friday dump. According to Footnoted, the phenomenon becomes apparent when one looks at the filings made between 4:00PM and 5:30PM on Fridays — when the stock market is closed for the week, but the SEC is still accepting filings. The logic behind dumping news on a Friday afternoon is that the market won’t be able to react until the following Monday, by which time (hopefully) the news might have been forgotten or obscured.

Since restatements generally fall into the category of news one does not want to deliver with a bullhorn at a busy intersection, we decided to test the Friday dump effect on our restatements database.

The table below presents restatements filed between January and August, 2013.

As indicated in the table above, there is no obvious Friday effect for the population of 2013 restatements. Restatement filings are delivered more or less uniformly across the week, with about 1/5 filed on Friday. However, 57% of the restatements were filed after the markets close at 4:00.

The effect is further amplified when we look at companies traded on major markets. This makes sense, since one would expect such companies to be more sensitive to market reactions than OTC companies would. If we narrow the population only to companies traded on NYSE, NASDAQ, or AMEX, the percentage of filings made after 4PM increases to 64%. A “4PM Effect”, though perhaps not as dramatic as the Friday dump, may still be of some interest.

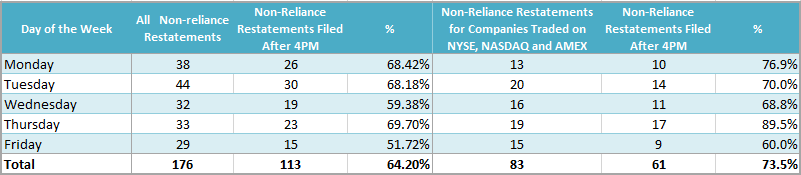

There is another subtlety to consider. What happens if we look only at the most material restatements, those that undermine reliance on previously filed financial statements? Such restatements are truly bad news — and, depending on circumstances, could even trigger significant negative stock movement. The following table shows only non-reliance restatements filed in 2013.

As evident from the table, timing does appear to be significant: 64% of all restating companies, and more than 73% of those traded on the NYSE, NASDAQ, and AMEX exchanges, disclose material restatements after 4PM.

To be clear: there is nothing wrong with filing a restatement after 4PM. SEC requires disclosure within 4 days of the discovery, and there is absolutely no requirement to file before closure of the markets. Caveats aside, though, 73% looks like something slightly more coordinated than sheer coincidence.