Key Findings

- The overall number of comment letters issued by the SEC has decreased since 2010

- The percentage of comment letters referencing a non-GAAP metric increased through 2017, but has been trending downward in the first 6 months of 2018

- The number and percentage of non-GAAP comment letters declined in 2018, while remaining above the 2015 level

- The ratio of non-GAAP letters that focus on tailored accounting increased from 6.5% in the last 6 months of 2016 to 12.3% in the first 6 months of 2018, while the total number of comment letters in the same periods decreased from 2,876 to 1,475

As discussed in a previous Audit Analytics post, the Division of Corporation Finance of the Securities and Exchange Commission issued updated Compliance & Disclosure Interpretations (C&DIs) in May 2016. Based on the speeches given by the SEC, companies were strongly advised to reconsider undue prominence of non-GAAP measures in financial reporting. The SEC expected that companies would “self-adjust” in upcoming periods to adhere to the standards.

Since May 2016, the C&DIs have been updated in October 2017 and April 2018, providing several opportunities for registrants to adjust.

But have companies been adhering to the clarified GAAP guidelines?

Looking at the trends of comment letters issued referencing form types 10-K, 10-K/A 10-Q, 10-Q/A and 8-K filings from January 2010 through June 2018, our research shows an inverse relationship in the overall number of comment letters issued and the percent of letters referencing non-GAAP issues.

Since 2010, the overall number of comment letters issued by the SEC decreased, from 15,646 at the end of 2010 to 4,525 for 2017, while the percentage of comment letters referencing non-GAAP measures increased.

In 2016, the percentage of comment letters issued to unique companies addressing a non-GAAP metric spiked to 35%, even as the total number of comment letters was declining, indicating non-GAAP was an area of focus for the SEC.

There is some evidence that companies are adhering to Regulation G and Regulation S-K after the updated C&DIs in 2016. In 2017, 37% of 4,525 comment letters raised non-GAAP concerns, while 25% of 1,409 letters raised non-GAAP issues in 2018. Although these amounts are still higher than pre-2016 percentages, it indicates that companies are beginning to self-correct.

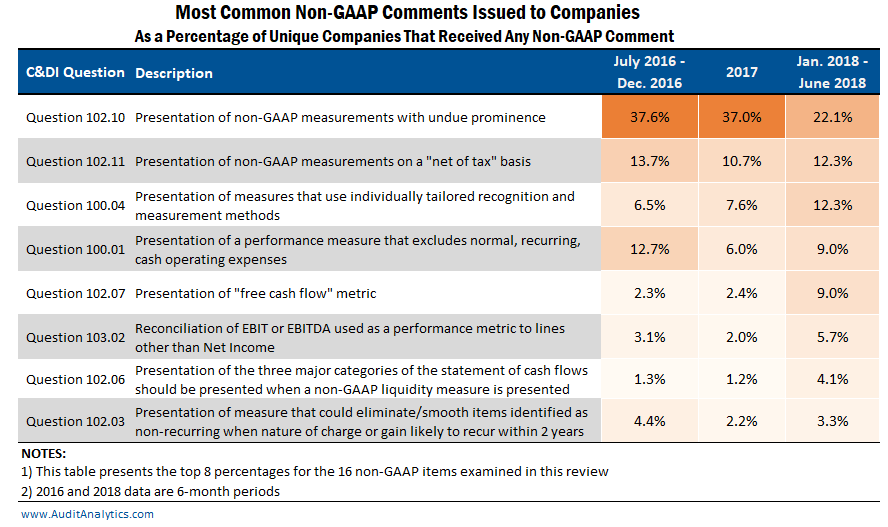

To focus on specific trends with non-GAAP comments, a subset of 16 specific non-GAAP comments related to 10-K, 10-Q, and 8-K form types were analyzed in relation to the total number of unique companies receiving any non-GAAP comment in letters disseminated between July 2016 (after the updated C&DIs) through August 2018.1

Overall, the trends that emerged based on the issuance frequency of 16 selected non-GAAP comments indicate that there is a narrowing focus on more specific issues. However, non-linear trending on certain issues is indicative of companies struggling with GAAP compliance on specific measures.

In the first six months of 2018, there are five metrics that make up over three-quarters (about 78%) of non-GAAP comments issued to registrants:

Undue Prominence (Question 102.10)

The percentage of unique companies receiving an “undue prominence” comment decreased marginally from 2016 (37.6%, 145 companies) to 2017 (37%, 184 companies), but then decreased significantly through June 2018 (22.1%, 27 companies). A previous deep-dive report by Audit Analytics found that companies were decreasing the practice of presenting non-GAAP metrics in press release text and headings prominently before the comparable GAAP metric.2

It is worth noting that undue prominence of a non-GAAP metric is a prima facie issue; it is, therefore, understandable that this is one of the most common non-GAAP comments issued by the SEC. Additionally, this is the easiest standard to comply with, as companies rarely push back and are likely to modify the disclosure in future filings.

Net of Tax Presentation (Question 102.11)

Comments related to presentation of net of tax have a less linear trend from 2016 to 2018. To comply with GAAP standards, adjustments that are used to arrive at a non-GAAP measure must show taxes as a separate adjustment and must be explained.

These are less severe comments based on presentation in financial reporting. Similar to undue prominence, issues related to net of tax presentations are typically resolved in future comments.

Individually Tailored Recognition & Measurement Methods (Question 100.04)

The most interesting trend from the top 5 non-GAAP comments analyzed occurs with individually tailored recognition and measurement methods. 12.3% of the companies receiving any non-GAAP comment received a letter referencing this issue in 2018. This metric has raised questions for registrants and regulators alike due to complexities involved with corporate accounting, as discussed in a Wall Street Journal article in 2017.

For example, Nordstrom Inc. [JWN] received the following comment in an April 2018 letter (emphasis is ours):

“1. You include adjustments to arrive at net operating profit that appear to remove your operating lease rent expense under GAAP and replace it with estimated depreciation, as if these leases had met the criteria for capital leases or you had purchased the properties … It appears that these adjustments may substitute individually-tailored recognition and measurement methods for those of GAAP. Please remove these adjustments from your non-GAAP measure or tell us how you considered the guidance in Question 100.04 of the Non-GAAP Financial Measures Compliance and Disclosure Interpretations updated on April 4, 2018 and concluded that these adjustments were appropriate.”

The SEC concluded the review after Nordstrom pushed back on the comment, asserting the adjustments are necessary and reporting that future filings will include a clarifying disclosure.

Measures Excluding Normal, Recurring, or Cash Operating Expenses (Question 100.01)

The trend for measures excluding normal, recurring, or cash operating expenses has not been linear since 2016. This measure, as with individually tailored recognition methods, is subject to the complexities of corporate accounting.

Complexities include certain expenses and costs that require considerable judgments and estimates. For example, expenses and costs related to acquisitions and restructuring may occur over multiple periods, but are not necessarily recurring expenses.

In December 2016, the SEC issued a comment to Hanesbrands Inc. [HBI], noting an exclusion of acquisition and integration costs in the presented non-GAAP measures, despite the Company incurring the charges in three consecutive annual reporting periods. Hanesbrands justified the exclusion, explaining the costs did not relate to ongoing business operations in the three periods and the costs associated with several singular transactions are not expected to continue on a recurring basis.

It took another back-and-forth comment letter conversation before the SEC was satisfied with the clarification provided by Hanesbrands.

Considerations for classifying normal, recurring, or cash-operating expenses revolve around unique circumstances for each registrant that must be explained in detail, possibly underlying the non-linear trend.

Free Cash Flow (Question 102.07)

The percentage of companies receiving comments referencing presentation of free cash flow has increased significantly since 2016.

A possible explanation for this increase may be that it is a gray area, as demonstrated by its corresponding Compliance & Disclosure Interpretation (Question 102.07):

“…However, companies should be aware that this measure does not have a uniform definition and its title does not describe how it is calculated. Accordingly, a clear description of how this measure is calculated, as well as the necessary reconciliation, should accompany the measure where it is used…” [May 17, 2016]

It is interesting to note then, the increased percentage of companies receiving a comment on the required presentation of the three major categories of the statement of cash flows when a non-GAAP liquidity measure is used (Question 102.06). Since the presentation of free cash flow is a non-GAAP liquidity measure, an increase in comments related to the three major categories of the statement of cash flows may indicate that companies are receiving both comments related to one item of financial reporting.

This seems to be the case with multiple registrants so far in 2018, including National Fuel Gas Company [NFG] and H.B. Fuller Company [FUL]. Both registrants received comments related to further explanation of free cash flows, accompanied by a comment related to the absence of the three major categories of the statement of cash flows in their respective financial statements.

• • • • •

Overall, these trends suggest that more complex and significant issues with non-GAAP financial reporting measures, such as tailored accounting and free cash flows, are being addressed more often in SEC comment letters to registrants. The more easily identifiable issues, such as undue prominence and net of tax presentation, are still addressed but the percentage of companies receiving these comments is gradually decreasing, as registrants self-correct following the updated C&DIs in May 2016.

Trends to keep an eye on include the non-GAAP measures that are complicated by complex accounting practices and require detailed explanation of unique circumstances be provided. It will be interesting to see if the trend of the SEC nudging companies for better explanations will endure, or if registrants will make an effort to provide more clarification on financial statements.

A version of this article was first available on FactSet to subscribers of our Accounting Quality and Insights. For subscription information please contact us at info@auditanalytics.com or (508) 476-7007.

1.For a comprehensive list of non-GAAP comments included in the analysis and the corresponding numbers and percentages of letters and unique companies, please contact Audit Analytics ↩

2. Subscribers to Audit Analytics can download “Corporate Implementation of SEC’s Compliance & Disclosure Interpretations Regarding Non-GAAP Financial Measures” here. All others may purchase the report here. ↩

Trends in SEC Non-GAAP Comment Letters 2016-2018

Key Findings

As discussed in a previous Audit Analytics post, the Division of Corporation Finance of the Securities and Exchange Commission issued updated Compliance & Disclosure Interpretations (C&DIs) in May 2016. Based on the speeches given by the SEC, companies were strongly advised to reconsider undue prominence of non-GAAP measures in financial reporting. The SEC expected that companies would “self-adjust” in upcoming periods to adhere to the standards.

Since May 2016, the C&DIs have been updated in October 2017 and April 2018, providing several opportunities for registrants to adjust.

But have companies been adhering to the clarified GAAP guidelines?

Looking at the trends of comment letters issued referencing form types 10-K, 10-K/A 10-Q, 10-Q/A and 8-K filings from January 2010 through June 2018, our research shows an inverse relationship in the overall number of comment letters issued and the percent of letters referencing non-GAAP issues.

Since 2010, the overall number of comment letters issued by the SEC decreased, from 15,646 at the end of 2010 to 4,525 for 2017, while the percentage of comment letters referencing non-GAAP measures increased.

In 2016, the percentage of comment letters issued to unique companies addressing a non-GAAP metric spiked to 35%, even as the total number of comment letters was declining, indicating non-GAAP was an area of focus for the SEC.

There is some evidence that companies are adhering to Regulation G and Regulation S-K after the updated C&DIs in 2016. In 2017, 37% of 4,525 comment letters raised non-GAAP concerns, while 25% of 1,409 letters raised non-GAAP issues in 2018. Although these amounts are still higher than pre-2016 percentages, it indicates that companies are beginning to self-correct.

To focus on specific trends with non-GAAP comments, a subset of 16 specific non-GAAP comments related to 10-K, 10-Q, and 8-K form types were analyzed in relation to the total number of unique companies receiving any non-GAAP comment in letters disseminated between July 2016 (after the updated C&DIs) through August 2018.1

Overall, the trends that emerged based on the issuance frequency of 16 selected non-GAAP comments indicate that there is a narrowing focus on more specific issues. However, non-linear trending on certain issues is indicative of companies struggling with GAAP compliance on specific measures.

In the first six months of 2018, there are five metrics that make up over three-quarters (about 78%) of non-GAAP comments issued to registrants:

Undue Prominence (Question 102.10)

The percentage of unique companies receiving an “undue prominence” comment decreased marginally from 2016 (37.6%, 145 companies) to 2017 (37%, 184 companies), but then decreased significantly through June 2018 (22.1%, 27 companies). A previous deep-dive report by Audit Analytics found that companies were decreasing the practice of presenting non-GAAP metrics in press release text and headings prominently before the comparable GAAP metric.2

It is worth noting that undue prominence of a non-GAAP metric is a prima facie issue; it is, therefore, understandable that this is one of the most common non-GAAP comments issued by the SEC. Additionally, this is the easiest standard to comply with, as companies rarely push back and are likely to modify the disclosure in future filings.

Net of Tax Presentation (Question 102.11)

Comments related to presentation of net of tax have a less linear trend from 2016 to 2018. To comply with GAAP standards, adjustments that are used to arrive at a non-GAAP measure must show taxes as a separate adjustment and must be explained.

These are less severe comments based on presentation in financial reporting. Similar to undue prominence, issues related to net of tax presentations are typically resolved in future comments.

Individually Tailored Recognition & Measurement Methods (Question 100.04)

The most interesting trend from the top 5 non-GAAP comments analyzed occurs with individually tailored recognition and measurement methods. 12.3% of the companies receiving any non-GAAP comment received a letter referencing this issue in 2018. This metric has raised questions for registrants and regulators alike due to complexities involved with corporate accounting, as discussed in a Wall Street Journal article in 2017.

For example, Nordstrom Inc. [JWN] received the following comment in an April 2018 letter (emphasis is ours):

The SEC concluded the review after Nordstrom pushed back on the comment, asserting the adjustments are necessary and reporting that future filings will include a clarifying disclosure.

Measures Excluding Normal, Recurring, or Cash Operating Expenses (Question 100.01)

The trend for measures excluding normal, recurring, or cash operating expenses has not been linear since 2016. This measure, as with individually tailored recognition methods, is subject to the complexities of corporate accounting.

Complexities include certain expenses and costs that require considerable judgments and estimates. For example, expenses and costs related to acquisitions and restructuring may occur over multiple periods, but are not necessarily recurring expenses.

In December 2016, the SEC issued a comment to Hanesbrands Inc. [HBI], noting an exclusion of acquisition and integration costs in the presented non-GAAP measures, despite the Company incurring the charges in three consecutive annual reporting periods. Hanesbrands justified the exclusion, explaining the costs did not relate to ongoing business operations in the three periods and the costs associated with several singular transactions are not expected to continue on a recurring basis.

It took another back-and-forth comment letter conversation before the SEC was satisfied with the clarification provided by Hanesbrands.

Considerations for classifying normal, recurring, or cash-operating expenses revolve around unique circumstances for each registrant that must be explained in detail, possibly underlying the non-linear trend.

Free Cash Flow (Question 102.07)

The percentage of companies receiving comments referencing presentation of free cash flow has increased significantly since 2016.

A possible explanation for this increase may be that it is a gray area, as demonstrated by its corresponding Compliance & Disclosure Interpretation (Question 102.07):

It is interesting to note then, the increased percentage of companies receiving a comment on the required presentation of the three major categories of the statement of cash flows when a non-GAAP liquidity measure is used (Question 102.06). Since the presentation of free cash flow is a non-GAAP liquidity measure, an increase in comments related to the three major categories of the statement of cash flows may indicate that companies are receiving both comments related to one item of financial reporting.

This seems to be the case with multiple registrants so far in 2018, including National Fuel Gas Company [NFG] and H.B. Fuller Company [FUL]. Both registrants received comments related to further explanation of free cash flows, accompanied by a comment related to the absence of the three major categories of the statement of cash flows in their respective financial statements.

• • • • •

Overall, these trends suggest that more complex and significant issues with non-GAAP financial reporting measures, such as tailored accounting and free cash flows, are being addressed more often in SEC comment letters to registrants. The more easily identifiable issues, such as undue prominence and net of tax presentation, are still addressed but the percentage of companies receiving these comments is gradually decreasing, as registrants self-correct following the updated C&DIs in May 2016.

Trends to keep an eye on include the non-GAAP measures that are complicated by complex accounting practices and require detailed explanation of unique circumstances be provided. It will be interesting to see if the trend of the SEC nudging companies for better explanations will endure, or if registrants will make an effort to provide more clarification on financial statements.

A version of this article was first available on FactSet to subscribers of our Accounting Quality and Insights. For subscription information please contact us at info@auditanalytics.com or (508) 476-7007.

1.For a comprehensive list of non-GAAP comments included in the analysis and the corresponding numbers and percentages of letters and unique companies, please contact Audit Analytics ↩

2. Subscribers to Audit Analytics can download “Corporate Implementation of SEC’s Compliance & Disclosure Interpretations Regarding Non-GAAP Financial Measures” here. All others may purchase the report here. ↩