For decades Intel (INTC) has been a flagship of innovation in semiconductors. Gordon E. Moore, one of Intel’s co-founders, made an observation back in 1965 that later became known as Moore’s Law. He postulated that the number of transistors in a CPU would double every year. By 1975, it had been revised to a cadence of two years, and for forty years the law has held up.

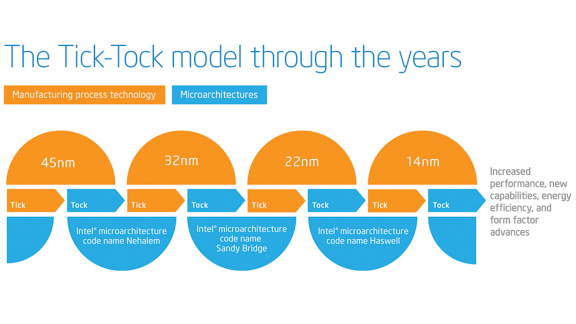

In order to be able to release a new generation of processors every year, Intel uses a so-called tick-tock innovation cycle. The tick phase takes an existing design and puts it on a new technological process with higher density, and the tock rolls out a new design on the current density. In lay terms, the tick-tock process means that two generations of Intel processors would be manufactured on the same capital equipment.

Source: http://www.Intel.com

In July 2015, Intel confirmed a delay in the new (10nm) technological process and that they would release a third generation processor on the old (14nm) one. This statement effectively puts an end to Moore’s Law as we know it…. or does it? Does this really signal a longer cadence, or is it just a one-time hiccup?

Interestingly, information about a potential long term innovation slow down came from a seemingly unrelated field – accounting. Seeking Alpha, in a recent post, analyzed Intel’s 10-K disclosures to point at a looming slowdown in the tick-tock cycle. But there was another aspect of that 10-K that we would like to bring further attention to.

In that most recent 10-K, Intel stated:

During the assessment performed in Q4 2015, we considered factors such as the lengthening of the process technology cadence resulting in longer node transitions on both 14nm and 10nm products. With those longer transitions, we added a third product to our 14nm roadmap. We have also increased re-use of machinery and tools across each generation of process technology. As a result, we determined that the useful lives of machinery and equipment in our wafer fabrication facilities should be increased from four to five years. We will account for this as a change in estimate that will be applied prospectively, effective in Q1 2016. This change in depreciable life drives approximately $1.5 billion in lower depreciation expense for 2016.

We do not see changes in estimates of this magnitude every day. In fact, this is the largest depreciation-related change that had a positive impact on earnings that we have ever seen (going back to 2006). The $1.5 billion change represents about 10% of 2015 pre-tax income.

One immediate takeaway is that comparability between 2016 and previous years is affected. But the consequences might be more significant than just that.

This is a powerful example of how a seemingly positive change in estimate – providing a relative “boost” to 2016 earnings – could actually signal trouble for the company. The extended useful life signifies a potentially epochal change in the industry, the effects of which are uncertain. Other companies have not been immune to the Moore’s Law slowdown, and many have made similar accounting changes.

In the past five years, eleven other semiconductor companies disclosed positive changes in depreciable lives estimates due to longer production cycles.

The quote below is from the 20-F filing of NXP Semiconductors (NXPI) dated 2/28/14:

Effective January 1, 2014 we extended the estimated useful life of the machinery and equipment used in our Standard Products front-end and back-end manufacturing processes. We reassessed the estimated useful life of these assets as a result of longer product life cycles, enhancements to manufacturing equipment, the versatility of manufacturing equipment to provide better flexibility to meet changes in customer demand and the ability to re-use equipment over several technology cycles.

We believe that the change in estimated useful life better reflects the future usage of this equipment. The effect of this change in estimated useful life is recognized prospectively as a change in accounting estimate. As a result of this change in accounting estimate, depreciation expense was reduced and operating income and net income increased by approximately $5 million for the three months ended March 30, 2014.

This same observation is also applicable to other industries. For example, for a car rental company, the increased useful life of its fleet, and correspondingly lower depreciation, may indicate an older fleet as a result of an attempt to cut costs – not necessarily a sign of strength.

One question that accountants always ask when seeing a large accounting change is “why now?” The correlation between positive accounting changes and negative business trends may not be as well documented as Moore’s Law, but nevertheless, by following changes in accounting estimates, we might be able to detect early signs of business changes.