Note: This post has been updated to include the full, unabridged FactSet article made available on November 12, 2018.

General Electric Co [GE] released an update on April 13, which among other things, clarified issues related to the adoption of the new revenue recognition standard.

This is the second time that GE stock dropped following the release of the updated adoption numbers. And although there was volatility following the releases, part of that instability could be explained by the way GE discussed its revenue recognition practices.

In our recent FactSet article, Audit Analytics took a deeper look into GE’s ASC 606 and SEC investigation disclosures.

GE provided two relevant pieces of information (both were previously disclosed during the January conference call). The first piece was related to the impact of the new revenue recognition rule and the second was related to the SEC investigation.

Key Findings include:

When General Electric Co [GE] filed its annual report after hours on February 23, share prices fell to a low of $13.95. The share price later rebound to $14.65 – up from the previous closing of $14.49.

The volatility following the report’s release is a bit of a surprise. The sharp swings in stock price following the release of the annual report indicate that the market had difficulty digesting the news. Part of that volatility could be explained by how GE discussed its revenue recognition practices.

GE provided two relevant pieces of information (both were previously disclosed during the January conference call). The first piece was related to the impact of the new revenue recognition rule and the second was related to the SEC investigation. As we discuss below, the ASC 606 impact is not a result of incorrect financials. And, while a SEC investigation is typically unwelcome news for a company, investigations do not always result in material error corrections.

Because of the new ASC 606 rule, which standardizes and simplifies how companies record revenue in customer contracts, all companies are required to disclose what changes they’ll need to make to past earnings statements and how they will implement those changes.

GE said they’ll use the full retrospective method. The full retrospective method is in many cases preferable from an investors’ standpoint because it provides a historical perspective and shows by how much past financials are affected. But in a quest for transparency, GE may have inadvertently spooked investors with the language they used. In the 10-K filing and during the conference call, GE used the word “restated,” which may have been what raised eyebrows (bolded emphasis is ours):

Although GE used the word “restated,” what they’re doing is a technical implementation of the new revenue recognition rule. This is not a restatement in the classic accounting sense, which normally raises red flags because of its negative connotations. The word restatement is often used to describe errors identified in the prior financial statements.

We think the media and investors should have noted another disclosure related to revenue recognition, one that we believe is more of a red flag than the well-publicized accounting changes because of ASC 606. Tucked away in the 10-K filing is this statement (bolded emphasis is ours):

The SEC notified GE in November about their investigation- and GE publicly disclosed it a few months later during the January conference call.

The SEC investigation focuses on accounting for long-term contracts. Contract accounting is a complex issue that presents challenges to all parties involved, including companies, analysts, and auditors.

One of the problems with contract accounting is that it relies heavily on estimates and analysts have very little visibility into the estimation process. Another problem is that contract estimates are subject to frequent re-evaluation which can cause significant swings in both revenue recorded and net income.

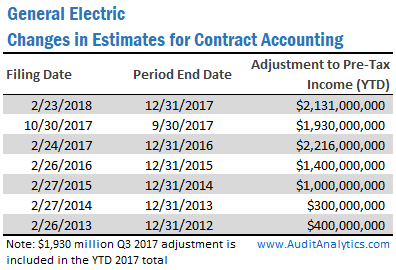

Since 2012, 105 companies disclosed 999 changes in estimates related to contract accounting. Below, we show the companies that recorded aggregate changes in estimates which exceeded $1 billion.

Although GE is no exception in recording substantial changes in contract estimates, there is one interesting distinction between GE and other companies that use contract accounting- the frequency.

While most companies disclose contract estimates on a quarterly basis, GE, for the most part, discloses estimates on an annual basis (which is why we see eight [seven annual and one quarterly] changes in estimates for GE in comparison to 20+ for some other companies).

As we discussed in our previous article, only material changes in estimates are required to be disclosed. GE is an extremely large company, so it is possible that changes in estimates that would be material to other contractors would still be below the materiality threshold for GE.

The impact on pre-tax income of GE’s contract accounting estimate changes seemed to accelerate in the past few years.

Since 2012, only thirteen stand-alone annual changes in contract estimates of at least $1 billion (twelve positive and one negative) were disclosed, and four of them were recorded by GE. It is not uncommon for changes in contract estimates to have a positive effect on the bottom line.

As with our previous articles, we are not suggesting that GE or any other company is manipulating the earnings with large positive adjustments. Instead, we are merely noting that contract accounting is a risk area because of the complexity. Schilit and Perler, in their classic book on accounting gimmicks, note that this method of revenue recognition is notoriously difficult to get right, and the nature of the method allows for ample “wiggle room”, even under GAAP.

The new ASC 606 accounting method will change some of GE’s contract accounting from over-a-period-of-time to a point-in-time, reducing estimates.

The SEC investigation into GEs contract accounting appears to be the latest in the chain of similar investigations. In our previous blog post, Is Contract Accounting under the Microscope?, we flagged changes in estimates related to contract accounting and discussed some of the investigations.

The SEC investigation has three possible outcomes:

- Worst-case scenario: a full restatement of previously filed financial statements. One example is what happened to KBR, Inc. [KBR]. In May 2014, KBR said it had to restate previously filed financial statements for 2013 because of contract accounting mistakes. When the errors were corrected, its cumulative net income fell by more than $150 million. Because of the restatement, KBR also invoked a very rare clawback provision.

- Less severe, but still negative: immaterial corrections, perhaps with some control deficiencies. For example, in July 2014, L3 Technologies, Inc. [LLL] announced that the company is investigating certain accounting matters in its Aerospace segment and that the Company expects to take $84 million charge mostly related to “contract cost overruns that were inappropriately deferred and overstatements of net sales”. Although the investigation appeared to be prompted by an internal review, an SEC investigation followed and in January 2017, the company agreed to pay $1.6 million to settle the SEC charges.

- Best-case scenario for GE: The SEC closes the investigation without any findings. Not every SEC investigation ends badly for a company. In 2016, the SEC investigated Boeing Co [BA] for its revenue recognition practices regarding costs and expected sales of a 787 Dreamliner and the 747-jumbo aircraft, as we discussed in the past. In a different case (not related to contract accounting), in 2014, the SEC closed an investigation into International Business Machines Corp [IBM] without releasing any findings surrounding IBM’s cloud revenue recognition practices.

Based on the limited disclosure we’ve seen so far, we cannot estimate the probability to any of these outcomes; however, it’s possible because of the way GE reported its ASC 606 revenue recognition implementation and blended in the SEC investigation, the market has already incorporated the worst possible outcome in share prices. Only time will tell.

A version of this article was previously available on FactSet to subscribers of our Accounting Quality Insights. For more information, email us at info@auditanalytics.com or call (508) 476-7007.