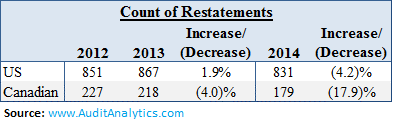

For the years 2012 through 2014, the number of Canadian restatements has been trending downward. Canadian filers issued 227 restatements in 2012, compared to 179 in 2014, a decrease of over 20%.

As we documented in our 2014 Financial Restatements report, there was a similar decline in the number of restatements among US filers. Unlike Canadian filers, however, the decline in US restatements was minor, and the number of US restatements has remained relatively flat since 2012.

The most commonly cited issues in Canadian restatements between 2012 and 2014 can be seen below. Tax-related issues were the most common both in 2012 and in 2013, while Debt and/or Equity classification issues were the most cited in 2014.  US filers have cited Debt, quasi-debt, warrants & equity (BCF) security issues more than any other issue since 2012. Cash flow statement classification and tax issues were also commonly cited issues in by US filers. For a comprehensive look at US restatements, see our 2014 restatements report.

US filers have cited Debt, quasi-debt, warrants & equity (BCF) security issues more than any other issue since 2012. Cash flow statement classification and tax issues were also commonly cited issues in by US filers. For a comprehensive look at US restatements, see our 2014 restatements report.

As part of our Canada (SEDAR) Module, Audit Analytics has been compiling a comprehensive database of Canadian public company restatements. SEDAR, which stands for System for Electronic Document Analysis and Retrieval, is the Canadian system for compiling public company financial statements, similar to EDGAR in the United States.1 The Audit Analytics’ Canadian restatement database contains over 1,700 restatements from more than 1,000 filers between 2009 and 2014.2

Keep an eye out for an upcoming article presenting highlights from our first annual SEDAR Audit Fees and Non-Audit Fees report.

1. There is a significant difference between SEDAR and EDGAR, however. EDGAR is administered by the SEC, which is the primary regulator of all publicly-listed companies in the United States. In Canada, each province has its own separate securities regulator, and there is no federal-level regulator comparable to the SEC. SEDAR is administered by the Canadian Securities Administrators, an informal body consisting of the provincial and territorial regulators.↩

2. It is important to note that there is some overlap among Canadian and SEC restatements. There are a number of companies that are listed in both the US and Canada, and a restatement issued by a dual-listed company would be included in both the Canadian and SEC restatement counts. ↩