Benjamin Franklin once noted that “in this world nothing can be said to be certain, except death and taxes.” While this maxim is perfectly applicable to mere mortals, public companies, at least in theory, can live on indefinitely. (According to this Slate article, the oldest company in the world is a construction company in Japan, which has existed continuously for 14 centuries.) Avoiding the grim reaper is one thing, but the tax man always gets his due. Nevertheless, good tax planning may help delay the reckoning.

One of the ways for a US company to defer some tax bills is to keep a portion of its income overseas, provided that the income was earned in another country and that the company plans to “reinvest” the the foreign earnings indefinitely. While most countries only tax corporate income earned in that country, the United States is unique in that it charges corporate income taxes on all income earned anywhere in the world. Taxes on that foreign income are only incurred when the income is “repatriated” back to the United States.

Over the past decade, the total amount of these indefinitely reinvested earnings has increased substantially, topping $2.4 trillion as of our most recent analysis. While the general trend over the past eight years has been to keep more cash overseas, a recent WSJ article, citing Audit Analytics research, noted that the number of Russell 1000 companies with IRFE declined about three percent from 563 in 2014 to 547 in 2015.

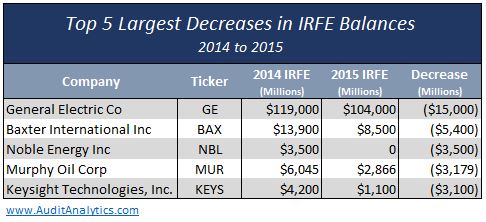

Further, a number of companies saw significant decreases to their indefinitely reinvested foreign earnings balance. In the table below, we show the five companies with the largest decreases from 2014 to 2015.

Additional companies that disclosed a significant decrease in IRFE include Marsh & McLennan ($2,900 million), Weatherford International ($2,897 million) and Accenture plc ($2,865 million).

We are not certain what may have caused the decline in the number of companies that keep the money abroad, but we thought it would be interesting to look at a couple examples of companies that recently repatriated, or may need to repatriate, part of their indefinitely reinvested foreign earnings.

During 2015, Costco (COST) repatriated a substantial portion of its indefinitely reinvested earnings and changed its position regarding additional portions of its cash held overseas. Interestingly, Costco did not record any tax liabilities on the amounts brought back to the US. Instead, the transaction created an immaterial tax benefit at the end of 2015. A recent SEC comment letter questioned whether the remaining overseas cash is still indefinitely reinvested and whether a tax liability ought to be recorded:

Although we have historically asserted that foreign undistributed earnings will be permanently reinvested, we may repatriate undistributed earnings to the extent we can do so without adverse tax consequence.

With respect to fiscal 2014 and 2015, Costco determined that a portion of Canadian earnings could be repatriated without adverse tax consequences. The determination in both cases was based in part on substantial weakening of the Canadian dollar versus the U.S. dollar, which directly impacted the foreign tax credit associated with the partial repatriation of these earnings, resulting in immaterial tax consequences for each change in our position on permanent reinvestment as disclosed in our Form 10-K for 2014 and 2015. Neither event, however, changed the fundamental premises of our analysis under ASC 740-30-25-17 and 18, as described above.

In the same conversation with the SEC, Costco indicated that the repatriated amounts were to be $904 million in fiscal 2015 and $685 million in fiscal 2016, totaling $1.6 billion.

Another interesting example of repatriation comes from Canada. A Canadian subsidiary of CST Brands (CST) distributed a note receivable worth $360 million to a subsidiary in the United States. According to the company, the remaining overseas profits are still indefinitely reinvested and no further repatriation costs are anticipated:

Within the disclosure on page 124, CST stated that the cumulative undistributed earnings of our foreign subsidiaries were approximately $1.1 billion and that on December 17, 2015, our Canadian subsidiary distributed a note receivable worth $360 million to a subsidiary in the United States. This distribution represented a one-time reduction of our tax basis in our Canadian subsidiary’s stock (with a net withholding tax impact of $14 million that was reflected in the 2015 effective tax rate) and resulted in a note payable at the Canadian subsidiary level. The statement made during the fourth quarter 2015 earnings call refers to repatriating cash out of Canada, representing repayments of this note payable. As such there will be no further tax cost associated with these repayments.

A different set of circumstances may lead EMC to bring back up to $3.5 billion in cash. The company’s merger agreement with Dell stipulates that EMC is required to provide $4.75 billion in cash to help finance the $67 billion buyout deal. As of December 31, 2015, EMC had about $1.2 billion in cash. The rest, according to a recent filing, may need to come from subsidiaries and affiliates.

This potential repatriation could be a taxable event for the company. However, EMC expects that such a transaction would not create a significant tax liability since cash equivalents and marketable securities held overseas are in an “unrealized loss position and would significantly reduce the tax associated with those which are in an unrealized gain position”. In a follow up letter, the company added that “the Company believes that neither the repatriation itself nor the net realized gains and losses would result in a material tax liability to the Company on a stand-alone basis.”

These cases are somewhat outside the norm; the decision to bring back tax profits is not always tax free. Understandably, companies would employ a variety of tax planning techniques to minimize the bill, yet the transactions may still carry substantial costs from both tax and accounting standpoints.

For example, in February 2016 filing, Sothebys (BID) disclosed that, in order to finance stock repurchase programs and strategic alternatives, the company will need to tap into overseas cash reserves. The transaction added $65.7 million in tax liability and bumped 2015 effective tax rate to 77.5%:

Repatriation of Foreign Earnings—In prior periods, based on Sotheby’s projections and planned uses of U.S. and foreign earnings, management had intended that approximately $400 million of accumulated foreign earnings relating to years prior to 2014 would be indefinitely reinvested outside of the U.S. As a result, Sotheby’s did not record deferred income taxes on these earnings in its financial statements. Due to the resignation of William F. Ruprecht as Sotheby’s President and Chief Executive Officer in November 2014 and the subsequent hiring of Thomas S. Smith, Jr. as his replacement in March 2015, and the resulting reevaluation of the Company’s strategic priorities, the Board of Directors and management reassessed Sotheby’s U.S. and foreign cash needs in the fourth quarter of 2015. As a result of this reassessment and in consideration of the recent expansion of Sotheby’s Common Stock repurchase program (see Note 11), as well as the need for cash in the U.S. to fund other corporate strategic initiatives, in the fourth quarter of 2015, it became apparent that these foreign earnings will instead be repatriated to the U.S. in the foreseeable future. Consequently, in the fourth quarter of 2015, Sotheby’s recognized a non-cash income tax charge of $65.7 million (net of foreign tax credits) for the deferred income taxes on these foreign earnings. The specific timing of the repatriation of these foreign earnings and cash payment of the associated taxes is currently being evaluated.

In the past, other companies, including GE and Ebay brought back billions of dollars, paying as much as 6 billion in additional tax expenses. (Given the large amount repatriated, it is not surprising that GE also received a comment letter about its intent to keep the rest of the IRFE overseas.)

For further information or to request a copy of our latest Indefinitely Reinvested Foreign Earnings report, please contact us at info@auditanalytics.com.

Tax Implications of IRFE Repatriation

Benjamin Franklin once noted that “in this world nothing can be said to be certain, except death and taxes.” While this maxim is perfectly applicable to mere mortals, public companies, at least in theory, can live on indefinitely. (According to this Slate article, the oldest company in the world is a construction company in Japan, which has existed continuously for 14 centuries.) Avoiding the grim reaper is one thing, but the tax man always gets his due. Nevertheless, good tax planning may help delay the reckoning.

One of the ways for a US company to defer some tax bills is to keep a portion of its income overseas, provided that the income was earned in another country and that the company plans to “reinvest” the the foreign earnings indefinitely. While most countries only tax corporate income earned in that country, the United States is unique in that it charges corporate income taxes on all income earned anywhere in the world. Taxes on that foreign income are only incurred when the income is “repatriated” back to the United States.

Over the past decade, the total amount of these indefinitely reinvested earnings has increased substantially, topping $2.4 trillion as of our most recent analysis. While the general trend over the past eight years has been to keep more cash overseas, a recent WSJ article, citing Audit Analytics research, noted that the number of Russell 1000 companies with IRFE declined about three percent from 563 in 2014 to 547 in 2015.

Further, a number of companies saw significant decreases to their indefinitely reinvested foreign earnings balance. In the table below, we show the five companies with the largest decreases from 2014 to 2015.

Additional companies that disclosed a significant decrease in IRFE include Marsh & McLennan ($2,900 million), Weatherford International ($2,897 million) and Accenture plc ($2,865 million).

We are not certain what may have caused the decline in the number of companies that keep the money abroad, but we thought it would be interesting to look at a couple examples of companies that recently repatriated, or may need to repatriate, part of their indefinitely reinvested foreign earnings.

During 2015, Costco (COST) repatriated a substantial portion of its indefinitely reinvested earnings and changed its position regarding additional portions of its cash held overseas. Interestingly, Costco did not record any tax liabilities on the amounts brought back to the US. Instead, the transaction created an immaterial tax benefit at the end of 2015. A recent SEC comment letter questioned whether the remaining overseas cash is still indefinitely reinvested and whether a tax liability ought to be recorded:

In the same conversation with the SEC, Costco indicated that the repatriated amounts were to be $904 million in fiscal 2015 and $685 million in fiscal 2016, totaling $1.6 billion.

Another interesting example of repatriation comes from Canada. A Canadian subsidiary of CST Brands (CST) distributed a note receivable worth $360 million to a subsidiary in the United States. According to the company, the remaining overseas profits are still indefinitely reinvested and no further repatriation costs are anticipated:

A different set of circumstances may lead EMC to bring back up to $3.5 billion in cash. The company’s merger agreement with Dell stipulates that EMC is required to provide $4.75 billion in cash to help finance the $67 billion buyout deal. As of December 31, 2015, EMC had about $1.2 billion in cash. The rest, according to a recent filing, may need to come from subsidiaries and affiliates.

This potential repatriation could be a taxable event for the company. However, EMC expects that such a transaction would not create a significant tax liability since cash equivalents and marketable securities held overseas are in an “unrealized loss position and would significantly reduce the tax associated with those which are in an unrealized gain position”. In a follow up letter, the company added that “the Company believes that neither the repatriation itself nor the net realized gains and losses would result in a material tax liability to the Company on a stand-alone basis.”

These cases are somewhat outside the norm; the decision to bring back tax profits is not always tax free. Understandably, companies would employ a variety of tax planning techniques to minimize the bill, yet the transactions may still carry substantial costs from both tax and accounting standpoints.

For example, in February 2016 filing, Sothebys (BID) disclosed that, in order to finance stock repurchase programs and strategic alternatives, the company will need to tap into overseas cash reserves. The transaction added $65.7 million in tax liability and bumped 2015 effective tax rate to 77.5%:

In the past, other companies, including GE and Ebay brought back billions of dollars, paying as much as 6 billion in additional tax expenses. (Given the large amount repatriated, it is not surprising that GE also received a comment letter about its intent to keep the rest of the IRFE overseas.)

For further information or to request a copy of our latest Indefinitely Reinvested Foreign Earnings report, please contact us at info@auditanalytics.com.