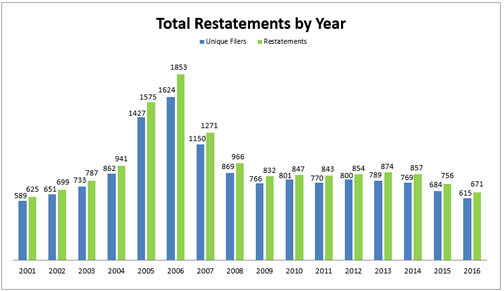

The annual Audit Analytics report on financial restatement trends is now available. This report provides a detailed analysis and comparison of trends in financial restatements over a sixteen-year period.

As summed up by the Wall Street Journal, 2016 has seen an “all time low” in restatements which could be attributed, as the article suggests, to tighter controls over financial reporting in accordance with the Sarbanes-Oxley Act of 2002.

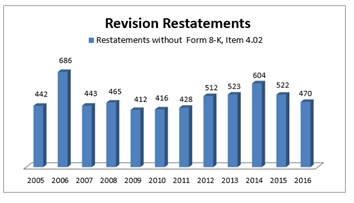

When looking at restatements we categorize them by two levels: Reissuance Restatements and Revision Restatements. Reissuance Restatements, sometimes referred to as “Big R” restatements, address a material error that calls for the reissuance of a past financial statement. Alternatively, Revision Restatements, or “little r” restatements, deal with immaterial misstatements, or adjustments made in the normal course of business. Because revision restatements are less severe, they are generally not looked at as a sign of poor reporting. However, some would argue that the disclosure of revision restatements shows a level of transparency and honesty by the filer.

Reissuan ce Restatements have declined for the tenth year in a row since 2004, when the 8-K disclosure requirements came into effect. 2016 shows a record low of 130, a sharp decline from 2006’s 941, the highest number in our sample period.

ce Restatements have declined for the tenth year in a row since 2004, when the 8-K disclosure requirements came into effect. 2016 shows a record low of 130, a sharp decline from 2006’s 941, the highest number in our sample period.

While the number of Revision Restatements has remained fairly steady, the percentage compared to all restatements has been gradually increasing. So while it’s true that we are seeing less restatements in general, the vast majority of restatements have been Revision Restatements (7 8.3% in 2016.)

8.3% in 2016.)

Additionally, the four year increase of US Accelerated filers that filed restatements spanning from 2011 to 2014, was broken in 2015 and continues to be on the decline in 2016. Interestingly, US Non-accelerated filers have also continued to decline and have hit a record low of 284 filers.

In order to gauge the severity of restatements, we turn to impact of net income. According to our report, about 59.1% of the restatements disclosed by publicly traded companies had no impact on earnings. This is the second highest percentage in 9 years.

The report also looks at both the average number of days restated and the average number of issues found in restatements, both of which continue to be low. However, the average number of days needed to restate increased to 5.37 (Note: This number is likely to increase as there are still outstanding restatements disclosed in 2016 that will most likely raise the average).

Overall, the trend for restatements continues to be on the decline. We are seeing fewer restatements, and those restatements that we do see, more often than not lack severity or material weakness. While the average amount of days to restate is slightly higher, the increase in Revision Restatements over Reissuance Restatements indicates more transparency and better quality disclosures.