In April 2016, the then-CEO of Perrigo (PRGO), Joe Papa, left the company to join the troubled pharmaceutical giant Valeant (VRX). On the heels of the accounting scandal surrounding Valeant’s subsidiary Philidor, it was thought that new leadership might be able to turn the company around. Eleven months later, Valeant is not yet out of the woods. Last week, Valeant’s major supporter and member of the Board of Directors, Bill Ackman, sold his stake in the company for a reported $2.8 billion loss.

The company Papa left behind has not exactly thrived either. Just one day after his departure, Perrigo stock lost 18% on weak guidance, and has continued a downward trend since.

Perrigo is a good example of a how weak performance and accounting quality go together. Since last April, the company has had a number of significant accounting-related issues.

In May 2016, Perigo identified and reported a material weakness related to the incorrect calculation of interim income taxes. The weakness did not result in a restatement, but it did force the company to conclude that its controls were not effective. As of today, the weakness is still unremediated:

Management has determined that we did not design and maintain effective management review controls that operated at a sufficient level of precision to ensure interim income taxes are properly recorded and disclosed in our consolidated financial statements in connection with the recording of indefinite-lived intangible asset impairment and estimated goodwill impairment. These control deficiencies resulted in a material misstatement in income taxes in the preliminary financial statements for the quarter ended April 2, 2016. The material misstatement in interim income taxes was corrected prior to the filing of this report.

In the same filing, the company identified additional errors, unrelated to the tax issue identified above. These other errors were corrected in the same quarter, and had the effect of increasing net loss by $13.7 million:

During the three months ended April 2, 2016, we identified certain errors in our consolidated financial statements for the transition period of June 28, 2015 to December 31, 2015, primarily related to the accrual estimates associated with product returns and tax related items in our BCH segment. These errors were corrected during the three months ended April 2, 2016 by increasing the consolidated operating loss by $14.5 million, which when combined with tax-related items increased the consolidated net loss by $13.7 million within the Condensed Consolidated Statements of Operations. We concluded that these errors were not material to the consolidated financial statements for the transition period of June 28, 2015 to December 31, 2015 and are not expected to be material to the consolidated financial statements for the year ended December 31, 2016.

Immaterial errors rarely trigger a significant market reaction on their own. A recent academic study, however, suggested that even immaterial errors could be associated with future control weaknesses and restatements, especially if multiple items are affected.

So far, 2017 has not brought much in the way of good news for Perrigo. On February 27, the long-standing CFO of Perrigo, Judy Brown, left to join Amgen. On the same day, the company filed a Form NT 10-K stating their inability to file their annual report by the March 1 deadline, citing among other reasons the need to review historical revenue recognition practices:

On February 27, 2017, the Company signed a definitive agreement to divest its rights to the royalty from the global nets sales of the multiple sclerosis drug, Tysabri®. Given the timing of this development, the Company has not completed its calculation of the implied fair value of the Tysabri® asset. In connection with the review for the sale, the Company’s independent auditors also are evaluating the historical revenue recognition practices associated with Tysabri®. In addition, the Company is in the process of identifying certain deferred tax assets and other related effects at Omega Pharma Invest N.V. As a result of these matters, the Company cannot, without unreasonable effort or expense, file its Form 10-K by the due date of March 1, 2017.

In the late filing notice, the company indicated two things of note: first, that a significant change in results of operations is anticipated; second, that the company would be able to file their annual report within the automatic 15 calendar day extension granted by the SEC. As of today – well past the 15-day extension – the annual report is yet to be filed, and no concrete update as to the expected filing date has been provided.

A recent WSJ article, citing Moody’s, reported that Perrigo’s inability to file its financial statement on time could potentially trigger a notice of default on part of $5.4 billion in outstanding bonds.

So what is next for Perrigo? Is Perrigo likely to restate its financial results?

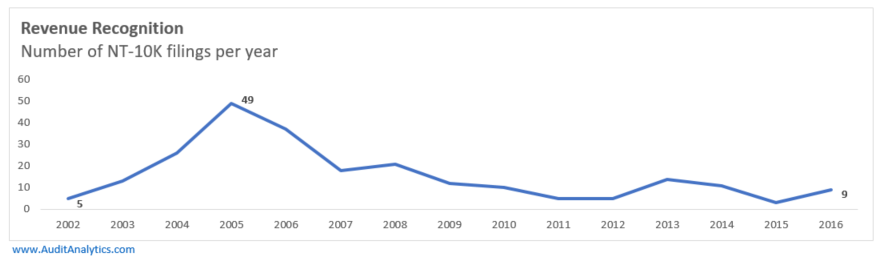

Audit Analytics analyzed every late filing ever disclosed by an SEC registrant. The chart below presents a subset of this population, namely, the number of NT 10-K filings that cited revenue recognition issues as contributing to the tardiness of their annual reports.

As we can see from the chart, revenue-related late filings are very rare. We identified only about 200 such filings since 2002. Still, while rare, a concern about revenue recognition is among the most significant warning signals that investors should be on the lookout for. It is almost always a serious issue when a company can’t file on time due to revenue recognition issues.

In the table below we summarize a number of important metrics and flags for the nine companies were unable to file their 10-Ks on time in 2016 due to revenue recognition problems.

Five of the nine have already filed financial statements, and another two have restatements pending. Only one company did not make a restatement. LifeVantage Corp, a small-cap pharmaceutical.

This leads us to believe that, based on the analysis of the year 2016 data, Perrigo is very likely to disclose substantial accounting errors that will probably result in a restatement. Revenue recognition restatements, it should be noted, are frequently associated with shareholder’s legal actions and significant legal costs.